-

Now We Know: Netflix Modeling Churn At Record 6.5 Million Subscribers in Q3 '11 Due to Effect of Pricing Change

A central question following Netflix's recent decision to separate DVD and streaming plans - driving some subscribers' rates up by 60% - was what effect it would have on churn. The hue and cry from outraged subscribers in the days after the decision was announced certainly indicated it would be meaningful. But it was anyone's best guess what it would actually be.

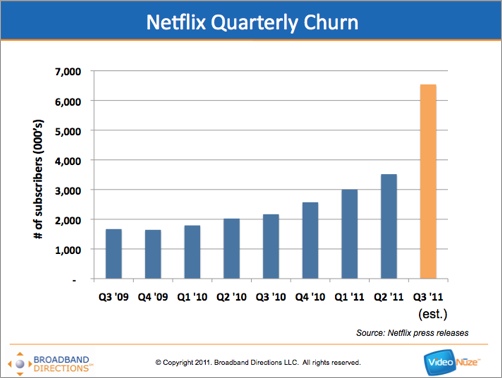

Now, with Netflix's Q3 '11 subscriber forecast included in its Q2 earnings release, plus a few assumptions I've made, it appears as though Netflix itself is modeling churn of approximately 6.5 million U.S. subscribers this quarter, a record for the company that could wipe out almost all of its quarterly gross subscriber additions in the U.S. (see below for a 2-year churn chart). The 6.5 million includes around 2.5-3 million incremental subscribers lost - presumably due to the price increase - over and above an expected churn of 3.5-4 million subscribers for the quarter.

The 6.5 million subscriber churn figure is calculated by starting with the mid-point of Netflix's Q3 U.S. ending subscriber forecast of 25 million, which implies growth of just 410K subscribers during the quarter. Assuming that gross subscriber additions are unaffected by the pricing increase, how many gross adds might Netflix have in Q3? Well, Q1 '11 gross adds were 80% higher than Q1 '10, and Q2 '11 gross adds were 73% higher than Q2 '10. So say Q3 '11 gross ads are 75% higher than the 3.97 million U.S. gross ads from Q3 '10 and that means Netflix could have U.S. gross adds of over 6.9 million. But since it's forecasting a mid-point net subscriber growth in the U.S. of about 410K, that means during the quarter 6.5 million would churn out (note Netflix is forecasting a range of ending subscribers of 24.6 million to 25.4 million, so estimated churn could be plus or minus 400K).

Two big questions here are that subscriber additions in Q3 continue growing at the same year-over-year pace as in the first 2 quarters of the year, and that underlying normal churn rates remain steady. On the former point, even though Netflix disclosed that 75% of its Q2 new subscribers took the streaming only plan (whose price didn't change), the question is how the remaining 25% who took the combined DVD-streaming might translate in Q3 results given lower DVD-only pricing, but higher combined DVD-streaming pricing. And on underlying normal churn, given the higher churn rate of streaming-only subscribers, this amount could increase in Q3 thereby reducing churn attributable to price the increase.

Meanwhile, one other big unknown lurks for Netflix later this year. The company positioned the price increase related churn as being confined to Q3 only, indicating that in Q4 "we expect domestic net additions to return to a pattern of year-over-year growth." That may be a bit optimistic - with price increases not kicking in and visible on subscribers' credit card statements until late in Q3, there could well be a spillover churn effect felt in Q4.

Net, net, the recent price increase has opened up significant uncertainty in Netflix's U.S. subscriber growth expectations, which was immediately reflected in a 10% after-hours drop in its stock price. All of this could be ancient history a year from now if Netflix resumes steady U.S. growth and higher revenue per subscriber kicks in, along with well-executed international expansions. But those are ifs. For now, the price increase looks like a gutsy move by Netflix that has disrupted the impressive results it has delivered for the last 2 years.

Categories: Aggregators

Topics: Netflix

Connect with VideoNuze

Exclusive News Roundup

- Amazon MGM Studios Head Jen Salke Exiting to Focus on Producing IndieWire

- YouTube is changing how YouTube Shorts views are counted TechCrunch

- Americans Now Spend $69 per Month on Video Streaming - and Nearly Half Think It’s Too Much Variety

- NBCUniversal To Launch 40 FAST Channels On LG Smart-TVs Under Expanded Partnership Deadline

- In Warning Sign for Hollywood, Younger Consumers Are Choosing Creator Content Over Premium TV and Movies The Hollywood Reporter

- Netflix’s $275 Million ‘The Electric State’ Has Fallen Flat. No Matter? NY Times