-

The Fuzzy Math of Apple's TV Subscription Service Doesn't Add Up

Yesterday's Wall Street Journal story, suggesting that CBS and Disney may participate in Apple's planned TV subscription service, caused was yet another tremor in the already chaotic video industry. Though Apple's plans are still preliminary, when I consider the numbers the Journal reported, the company's fuzzy math suggests incumbent distributors have little to worry about just yet.

The Journal said that in "In at least some versions of the proposal, Apple would pay media companies about $2 to $4 a month per subscriber for a broadcast network like CBS or ABC, and about $1 to $2 a month per subscriber for a basic-cable network..." Let's assume the mid-points for both: $3/mo for broadcast networks and $1.50/mo for cable networks. With 4 broadcast networks (assuming NBC participates, which under Comcast ownership is itself unlikely), that would be $12 in fees/mo. Say Apple signed up 12 cable networks, that would be another $18 in fees/mo. Together the $30 in fees/mo equals what Apple is reportedly looking to charge consumers. And this package would only deliver 16 channels, which would induce few consumers to cut the cord. And by the way, there's zero chance that one of those 16 cable channels would be Disney's ESPN, which already gets north of $3/mo/sub in all of its existing affiliate deals.

Given the broadcast networks' woes, it's within the realm of possibility that they would be enticed by the $2-$4/mo, considering it's above the $1/mo/sub that is often bandied about in retransmission consent discussions. Yet, Apple is supposedly talking about delivering the programs commercial-free, which means broadcasters' total revenue per month has to equal or exceed what they're already making per month for the plan to be interesting to them. With $60 billion/year in TV advertising revenue at stake, that's a big gamble for broadcast networks to make. Even the notion that consumers would pay for broadcast programs simply because they're commercial-free is speculative. Most research I've seen suggests the opposite consumer preference (they'd rather stomach ads in exchange for free content).

An even bigger challenge for Apple is to get cable networks to play ball. Starting with my post over a year ago, "The Cable Industry Closes Ranks," I've continued to assert that, despite ongoing skirmishes, cable networks and cable operators are joined at the hip in their desire to defend the traditional multichannel subscription model. In the model, big owners of cable networks bundle smaller channels with bigger, more popular ones, and require that cable operators, telcos and satellite operators take these as a package. This is the backdrop for why consumers often grouse that there are lots of channels, but little on that interests them personally. Meanwhile, TV Everywhere is intended to preserve this model as online viewing expectations build.

It stretches my imagination to believe that big cable network owners (Disney included) are going to allow Apple to cherry-pick which cable networks they want and disrupt the traditional model, especially at a time when cable networks want more, not less control. That cable networks would be willing to put Steve Jobs in the driver's seat of their digital futures is very unlikely. Analogies to the music business only go so far: remember, music companies were already under assault from rampant piracy and reeling under financial pressure when Apple came riding to their rescue. Cable networks feel no such urgency; they've been the brightest star in the media landscape as the recession has worn on.

I've learned never to underestimate Steve Jobs or Apple. But based on what's been reported so far, Apple's subscription TV math seems very fuzzy and any service that emerges from it is likely, for the most part, to be non-threatening to incumbent distributors. And that's before getting to the issues of Apple being a closed system and requiring consumers to buy a proprietary Apple TV box to get their programs onto their TVs. In the budding 'over-the-top" sweepstakes, Apple is one to watch for sure. But there are a lot of variables in play here. It will be fun to see if Jobs has yet another rabbit up his sleeve.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, Cable TV Operators

Topics: ABC, Apple, CBS, Disney

-

4 Items Worth Noting for the Nov 30th Week (Alicia Keys on YouTube, Jeff Zucker's record, Comcast's Xfinity, SI's tablet demo)

Following are 4 items worth noting for the Nov 30th week:

1. Alicia Keys concert on YouTube is an underwhelming experience - Did you catch any of the Alicia Keys concert on YouTube this past Tuesday night celebrating World AIDS Day? I watched parts of it, and while the music was great, I have to say it was disappointing from a video quality standpoint -lots of buffering and pixilation, plus watching full screen was impossible.

I think YouTube is on to something special webcasting live concerts. Recall its webcast of the U2 concert from the Rose Bowl on Oct 25th drew a record 10 million viewers. That concert's quality was far superior, and separately, the dramatic staging and 97,000 in-person fans also helped boost the excitement of the online experience. It's still early days, but to really succeed with the concert series, YouTube is going to have to guarantee a minimum quality level. Notwithstanding, American Express, the lead sponsor of the Keys concert had strong visibility and surely YouTube has real interest from other sponsors for future concerts. It could be a very valuable franchise YouTube is building and is further evidence of YouTube's evolution from its UGC roots.

2. Being a Jeff Zucker fan is lonely business - In yesterday's post, "Comcast-NBCU: The Winners, Losers and Unknowns" I said I've been a fan of Jeff Zucker's since seeing him deliver a brutally candid and very sober assessment of the broadcast TV industry at the NATPE conference in Jan '08. My praise elicited a number of incredulous email responses from readers who vehemently disagreed, thinking Zucker's performance merits him being sent to the woodshed rather than to the CEO's office for the new Comcast-NBCU JV.

To be sure, NBC's abysmal performance under Zucker (falling from first place to fourth in prime-time), will be one of his legacies, but I take a broader view of his tenure. A good chunk of NBCU's cable network portfolio came to the company via the Vivendi deal around the time Zucker took over responsibility for cable. Since that time the networks have grown strongly in audience and cash flow has doubled from about $1 billion to a projected $2.2 billion in '09. NBCU added Oxygen (which combined with its iVillage property makes a strong proposition for women-focused advertisers) and The Weather Channel, in a joint buyout with two PE firms.

While Zucker's hiring of Ben Silverman to run NBC was a misstep, NBCU has enjoyed stability on the cable side, with two of the highest-regarded women in TV, Bonnie Hammer and Lauren Zalaznick cranking out hit after hit for their respective networks. A CEO's tenure is always a mixed one, with plenty of wins and losses. It can be hard to know how much of the wins to ascribe to the CEO personally, rather than the executives below, but at the end of the day, NBCU was transformed from a single network company to a cable powerhouse; even Zucker skeptics have to give him some credit for this.

3. Comcast rebrands On Demand Online to Fancast Xfinity TV - yuck! - Largely lost in the NBCU commotion this week was news that B&C broke that Comcast is changing the name of its soon-to-be-launched TV Everywhere service from On Demand Online to Fancast Xfinity TV. Yikes, the branding gurus need to head back to the drawing board, and quick. The name violates the first rule of branding: pronunciation must be obvious and easy. Not only is it unclear how you pronounce Xfinity, it's a an unnecessary mouthful that doesn't fit with any of Comcast's other workmanlike brands (e.g. "Digital Cable," "On Demand," "Comcast.net"). If we're talking about a new videogame targeted to teenage boys, Xfinity is great. If we're talking about a service that provides online access to TV shows, there's no need for something super-edgy. I'd suggest just sticking with "On Demand Online." But even more importantly, priority #1 is getting the product launched successfully.

4. Sports Illustrated demo builds tablet computing buzz - If you haven't seen SI's demo of its tablet version being shown off this week, it's well worth a look at the video here. Never mind that there isn't such a tablet device on the market yet, the rumors swirling around Apple's planned launch of one has created an air of inevitability for the whole category. As the SI demo shows, a tablet can be thought of a larger version of an iPhone (likely minus the phone), providing larger screen real estate to make the user experience even more interesting. It's fascinating to think about what a tablet could do for magazines in particular, along the lines of what the Kindle has done for books. The mobile video and gaming possibilities are endless. Judge for yourselves.

Enjoy the weekend!

Categories: Aggregators, Broadcasters, Cable TV Operators, Magazines, People

Topics: Comcast, NBCU, Sports Illustrated, YouTube

-

VideoNuze Report Podcast #42 - December 4, 2009

Daisy Whitney and I are pleased to present the 42nd edition of the VideoNuze Report podcast, for December 4, 2009.

Today's sole topic is of course the big news of the week, Comcast's acquisition of NBCU. Daisy and I chat about the winners/losers/unknowns that I detailed in my post yesterday. There are a lot of aspects to the Comcast-NBCU deal and the new entity will have wide-ranging implications for the media industry. Listen in to learn more.

Click here to listen to the podcast (15 minutes, 24 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Broadcasters, Cable Networks, Cable TV Operators, Deals & Financings, Podcasts

Topics: Comcast, GE, Hulu, NBCU, Podcast

-

Comcast-NBCU: The Winners, Losers and Unknowns

With Comcast's acquisition of NBCU finally official this morning (technically, it's not an acquisition, but rather the creation of a JV in which Comcast holds 51% and GE 49%, until GE inevitably begins unwinding its position), it's time to assess the winners, losers and unknowns from the deal, the biggest the media industry has seen in a long while. I listened to the Comcast investor call this morning with Brian Roberts, Steve Burke and Michael Angelakis and reviewed their presentation.

Here's how my list shakes out, based on current information:

Winners:

1. Comcast - the biggest winner in the deal is Comcast itself, which has pulled off the second most significant media deal of the decade (the first was its acquisition in 2002 of AT&T Broadband, which made Comcast by far the largest cable operator in the U.S.), for a relatively small amount of upfront cash. Comcast has long sought to become a major player in cable networks, but to date has been able to assemble an interesting, but mostly second tier group of networks (only one, E! has distribution to more than 90 million U.S. homes).

The deal moves Comcast into the elite group of top 5 cable channel owners, alongside Disney, Viacom, Time Warner and News Corp, with pro-forma 2010 annual revenues of $18.2 billion and operating cash flow of $3 billion. It also provides Comcast with a huge hedge on its traditional cable/broadband/voice businesses, as the JV, on a pro-forma basis would be 35% of Comcast's overall 2010 revenue of $52.1 billion, though importantly only 18% of its cash flow of $16.5 billion. On the investor call, Roberts emphasized that the deal should not be seen as the company diminishing its enthusiasm for the traditional cable business, but given the downward recent trends in fundamentals (vividly shown in slides from my "Comcast's Digital Transformation Continues" post 3 weeks ago), the conclusion that Comcast will be relying on its content business for future growth is inescapable.

2. Cable networks' paid business model/TV Everywhere - With Comcast's executives' platitudes about cable networks being "the best part of the media business," the fact that cable networks will contribute 80%+ of the JV's cash flow and the ongoing travails of the ad-supported broadcast TV business, the deal puts an exclamation mark on the primacy of the dual-revenue stream cable network model and Comcast's commitment to defending it (see "The Cable Industry Closes Ranks" for more on this.)

The deal can also be seen as cementing the paid business model for online access to cable networks' programs. Comcast is committed to having online distribution of TV programs emulate the cable model, where access is only given to those consumers who pay for a multichannel subscription service. Much as they may resist acknowledging it, Hollywood and the larger creative community must see Comcast as doing them a huge service by preserving the consumer-paid model, helping the video industry avoid the financial fate of newspapers, broadcasters and music. To be sure, some consumers will cut the cord and be satisfied with what they can get for free online, however it is unlikely to be a large number any time soon. As for aspiring over-the-top providers, they'll need to look outside the cable network ecosystem to generate competitive advantage.

3. Jeff Zucker - The current head of NBCU will migrate into the role of CEO of the JV, greatly expanding his portfolio and influence. Zucker has fought the good fight to preserve the NBC network's status, rotating in new creative heads, shifting Leno to primetime, backing Hulu, etc, but the reality, as he pointed out earlier this year, is that NBCU in his mind has long since become a cable programming company. I've been a Zucker fan since seeing him speak at NATPE in '08 when he laid out a sober assessment of the broadcast business. Through solid acquisitions and execution, Zucker has proved himself to be far more than the wonderboy of "Today" - he's going to fit in well at Comcast and be a great addition to its executive team.

Losers:

1. NBC broadcast network and the JV's 10 owned and operated stations - While Comcast executives said they "don't anticipate any need or desire to divest any businesses" and "take seriously their responsibility" to the iconic NBC brand, the reality is that with the broadcast business contributing just 10% of the JV's pro-forma annual cash flow, the network, and especially the stations, are not just in the back seat of the JV, they're in the third row. Though broadcast contributes 38% of the JV's pro-forma revenue and the deal is being struck near the bottom of the advertising recession, it's hard to see things improving much. Exceptions are the sports division (more on that below), the TV production arm and possibly the news division. The only thing saving the stations is retrans and Comcast's need to appease regulators to get the deal done and keep the regulators at bay thereafter.

2. Other cable operators, telcos and satellite operators - It's never good news when one of your main competitors owns the rights to a good chunk of the key ingredients in your product, yet that's the reality for all other cable operators, telcos and satellite operators. Sure Comcast must be disciplined about throwing its weight around too much, but if these distributors cried when NBCU (and other big network owners) forced bundling and drove fee increases, they haven't seen anything until Comcast runs the renewal processes. With 6 channels having 90+ million homes under agreement plus many others in the JV's portfolio, Comcast is in a very strong negotiating position. As the world moves online, the threat that Comcast eventually says to hell with other distributors and goes over the top itself (a scenario I described here), other distributors have even bigger problems ahead.

3. GE - Yes GE gets about $15 billion in cash and a graceful exit from NBCU, but 20 years since incongruously acquiring NBC, the question burns even brighter, what was GE doing in the entertainment business in the first place? Hasta la vista GE, time to focus on manufacturing turbines and unraveling the woes at GE Capital.

Unknowns:

1. Do content and distribution go together any better this time around - With the disastrous results of AOL-Time Warner still fresh in the mind, it's fair to ask whether vertical integration will work any better this time around. Sensitive to the issue and no doubt anticipating questions on it, Roberts said on the call that this is "a different time and a different deal" and, pointing to News Corp-DirecTV, noted that sometimes vertical integration does work. In addition, he highlighted that the deal's financials are not predicated on achieving any elusive synergies. Still, aside from the obvious benefits of getting bigger in cable networks, the primary reasons cited for Comcast pursuing the deal still have synergy at their core: a slide that clearly says that "Distribution Benefits Content" and "Content Benefits Distribution." As always there are plenty of opportunities to pursue in theory; the challenge is executing on them given the rampant conflicts and turf battles that inevitably ensue.

2. Hulu's future - the online aggregator was literally not mentioned once in the Comcast presentation and its logo only appears on just one of the 36 slides in the deck, yet its presence is hard to underestimate. Hulu is the embodiment of the free, ad-supported premium video model that Comcast is so fiercely committed to combating. So how does it fare when one of its controlling partners soon will be Comcast? In response to a question, Steve Burke said he sees "broadcast content going to Hulu" and that "Hulu and TV Everywhere are complementary products." He also tersely dismissed the much-rumored idea of a Hulu subscription offering. It's impossible to know what becomes of Hulu, but with such divergent interests among the owners, it wouldn't surprise me if Hulu is unwound at some point post closing.

3. ESPN's role - With the JV's NBC Sports assets, plus Comcast's Versus, regional sports networks and Golf Channel, the new JV is primed to play a bigger role in national sports. While Fox Sports and TNT have skirmished for high-profile rights deals with ESPN, the new JV has a much stronger hand to play. It's fair to wonder whether Comcast, which likely sends Disney a check for $70-80 million each month to carry ESPN to its 24 million subscribers, won't at some point say, "hey we can do some of this ourselves" and move to become a bona fide ESPN competitor. In fact, ESPN figures into a far larger Comcast vs. Disney story line in the media industry going forward. The two companies are incredibly dependent on each other, and yet are poised to become even tougher rivals. Expect to hear much more about this one.

4. Consumers - last but not least, what does the deal mean for consumers? Likely very little initially, but over time almost certainly an acceleration of digitally-delivered on-demand premium content - but at a price. Comcast has the best delivery infrastructure, with the JV, soon premier content assets and a persistent, if sometimes incomplete (as with VOD, for example) commitment to shape the digital future. I expect that will mean lots of experimentation with windows, multiplatform distribution and co-promotion across brands. Washington will scrutinize the deal thoroughly, but with continued public service assurances from Comcast, will eventually bless it. Then it will be vigilant for anything that smacks of anti-competitiveness. Consumers should buckle up, the next stage of their media experience is about to begin.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, Cable TV Operators, Deals & Financings

Topics: Comcast, GE, Hulu, NBCU

-

The Opportunity for Paid Streaming of TV Shows Seems Narrow

A report this morning by Peter Kafka saying that YouTube is in discussions with TV networks to allow it to stream programs, commercial-free, for $1.99 apiece suggests to me that TV networks are in a tight place when it comes to trying to charge for streaming TV episodes.

The $1.99 figure happens to be the same amount currently charged by iTunes and Amazon (for example) to download and own an episode. If there's no material difference in value, then it's pretty straightforward to conclude that such a YouTube initiative would likely fail. Consumers will quickly ask - why would I rent

something one time for $1.99 when I can own it for the same price? The folks at YouTube must surely understand this too, and therefore be angling for something that would provide their rentals differentiated value vs. the current download-to-own models.

something one time for $1.99 when I can own it for the same price? The folks at YouTube must surely understand this too, and therefore be angling for something that would provide their rentals differentiated value vs. the current download-to-own models.The $1.99 figure was set several years ago, likely pitched somewhat arbitrarily by Apple to TV networks to govern the original iTunes download deals. Apple no doubt wanted the price point to be low enough to spur download volume, which would in turn drive sales of video-enabled iPods, yet different enough from the $.99 it was charging for song downloads. At least some of the TV networks likely thought this price point was too low from the start (a position underscored when NBC temporarily pulled its programs off iTunes 2 years ago in order to obtain more pricing flexibility), but acquiesced because of their desire to experiment with digital delivery and their lust to get into business with Steve Jobs.

Now however, the $1.99 price point is pretty well cemented in consumers' minds. Because streaming inherently provides less value than a download (lower video quality, requirement to be connected, etc.), in order for paid streaming to succeed, an episode surely needs to be priced lower than $1.99. But because Hulu and the networks themselves provide programs for free, streaming access to many TV episodes is already a reality. Further, I suspect most TV executives would be loathe to charge $.99 or less for a streaming TV program, as it sets up the consumer perception (albeit an incorrect apples to oranges one) that a TV episode is worth less than a music download.

Given these circumstances, this suggests that pricing for streaming TV episodes likely needs to fall somewhere in the $1-$2 range to have any shot of success at all. Even in this range, I'm skeptical that standalone paid-for streaming episodes will catch on. Few consumers download programs in sufficiently high volume to have the potentially lower differential streaming pricing save them much money. In short, they'll be inclined to keep on buying and downloading, even if they perceive they won't watch the show more than once or twice. The real problem is that the download price was originally set too low. If it were higher - even $2.99 or $3.99 per episode - that would have created more headroom to stake out a value proposition for streaming.

Yet another issue is that TV Everywhere is going to provide streaming of many TV shows anyway. Granted you'll have to be a paying video subscriber, but if TV Everywhere marketers are clever, they'll be able to create the perception that the streaming episodes are "free" causing even more pressure on standalone paid-for streaming. Networks would likely be better off trying to figure out how to get a piece of the TV Everywhere action.

In general I'm a fan of experimentation, but in this case I'm hard-pressed to see how TV program streaming for a fee will succeed.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters

-

4 Items Worth Noting for the Nov 16th Week (FCC's Open Access, Broadcast woes, Droid sales, AOL cuts)

Following are 4 items worth noting for the Nov 16th week:

1. FCC raises "Open Access" possibility, would further government's control of the Internet - As reported by the WSJ this week, the FCC is now considering an "Open Access" policy that would require broadband Internet providers to open up their networks for use by competitors. The move comes on top of FCC chairman Julius Genachowski's recent proposal for formalizing net neutrality, a plan that I vigorously oppose. Open Access gained steam recently due to a report released by Harvard's Berkman Center that characterized the U.S. as a "middle-of-the-pack" country along various broadband metrics. The report has been roundly dismissed by service providers as drawing incorrect conclusions due to reliance on incomplete data.

The FCC is in the midst of crafting a National Broadband Plan, as required by Congress, aimed at providing universal broadband service throughout the U.S. as well as faster broadband speeds. Improving broadband Internet access in rural areas of the U.S. is a worthy goal, but the FCC should be pursuing surgical approaches for accomplishing this, rather than turning the whole broadband industry upside down. As for increasing speeds, major ISPs are already pushing 50 and 100 mbps services, more than most consumers need right now anyway. Broadband connectivity is the lifeblood for online video providers and any government initiative that risks unintended consequences of slowing network infrastructure investments is unwise.

2. Broadcast TV executives waking up to online video's challenges - Reading the coverage of B&C/Multichannel News's panel earlier this week, "Free Streaming: Killing or Saving the Television Business" featuring Marc Graboff (NBCU), Bruce Rosenblum (Warner Bros.), Nancy Tellem (CBS) and John Wells (WGA), I kept wondering where were these sentiments when the Hulu business plan was being crafted?

Hulu is of course the poster child for providing free access to the networks' programs, with just a fraction of the ad load as on-air. While the panelists agreed that the industry should be dissuading consumers from cord-cutting, Hulu is (purposefully or not) the chief reason some people consider dropping cable/satellite/telco service. For VideoNuze readers, it's old news already that broadcast networks have been hurting themselves with their current online model. What was amazing to me in reading about the panel is that what now seems obvious should have been very apparent to industry executives from the start.

3. Motorola Droid sales off to a strong start - The mobile analytics firm Flurry released data suggesting that first week Verizon sales of the Motorola Droid smartphone were an estimated 250,000. Flurry tracks applications on smartphones to estimate sales volume of devices. While the Droid results are lower than the 1.6 million iPhone 3GS units sold in that device's first week, Flurry notes that the iPhone 3GS was available in 8 countries and also had an installed base of 25 million 1st generation iPhones to draft on.

The Droid's success is important for lots of reasons, but from my perspective the key is how it expands the universe of mobile video users. As I noted in "Mobile Video Continues to Gain Traction," a robust mobile ecosystem is developing, and getting more smartphones into users' hands is crucial. I was in my local Verizon store this week and saw the Droid for the first time - though it lacks some of the iPhone's sleekness, the video quality is even better.

4. AOL's downsizing suggests further pain ahead - AOL was back in the news this week, planning to cut one-third of its employees ahead of its spin-off from Time Warner on Dec. 9th. The cuts will bring the company's headcount to 4,500-5,000, down from its peak of 18,000 in 2001. As I explained recently, no company has been hurt more by the rise of broadband than AOL, whose dial-up subscribers have fled en masse to broadband ISPs. Now AOL is going all-in on the ad model, even as the ad business itself is getting hurt by the ongoing recession. New AOL CEO Tim Armstrong is clearly a guy who loves a challenge; righting the AOL ship is a real long shot bet. I once thought of AOL as being a real leader in online video. Now I'm hard-pressed to see how the AOL story is going to have a happy ending.

Enjoy your weekends!

Categories: Advertising, Aggregators, Broadband ISPs, Broadcasters, Mobile Video, Portals, Regulation

Topics: AOL, Droid, FCC, Hulu, iPhone, Motorola, Verizon

-

4 Items Worth Noting for the Nov 2nd Week (Q3 earnings review, Blu-ray streaming, Apple lurks, "Anywhere" coming)

Following are 4 items worth noting for the Nov 2nd week:

1. Media company and service provider earnings underscore improvements in economy - This was earnings week for the bulk of the publicly-traded media companies and video service providers, and the general theme was modest increases in financial performance, due largely to the rebounding economy. The media companies reporting - CBS, News Corp, Time Warner. Discovery, Viacom and the Rainbow division of Cablevision - showed ongoing strength in their cable networks, with broadcast networks improving somewhat from earlier this year. For ad-supported online video sites, plus anyone else that's ad-supported, indications of a healthier ad climate are obviously very important.

Meanwhile the video service providers reporting - Comcast, Cablevision, Time Warner Cable and DirecTV all showed revenue gains, a clear reminder that even in recessionary times, the subscription TV business is quite resilient. Cable operators continued their trend of losing basic subscribers to emerging telco competitors (with evidence that DirecTV might now be as well), though they were able to offset these losses largely through rate increases. Though some people believe "cord-cutting" due to new over-the-top video services is real, this phenomenon hasn't shown up yet in any of the financial results. Nor do I expect it will for some time either, as numerous building blocks still need to fall into place (e.g. better OTT content, mass deployment of convergence devices, ease-of-use, etc.)

2. Blu-ray players could help drive broadband to the TV - Speaking of convergence devices, two articles this week highlighted the role that Blu-ray players are having in bringing broadband video to the living room. The WSJ and Video Business both noted that Blu-ray manufacturers see broadband connectivity as complementary to the disc value proposition, and are moving forward aggressively on integrating this feature. Blu-ray can use all the help it can get. According to statistics I recently pulled from the Digital Entertainment Group, in Q3 '09, DVD players continue to outsell Blu-ray players by an almost 5 to 1 ratio (15 million vs. 3.3 million). Cumulatively there are only 11.2 Blu-ray compatible U.S. homes, vs. 92 million DVD homes.

Still, aggressive price-cutting could change the equation. I recently noticed Best Buy promoting one of its private-label Insignia Blu-ray players, with Netflix Watch Instantly integrated, for just $99. That's a big price drop from even a year ago. Not surprisingly, Netflix's Chief Content Officer Ted Sarandros said "streaming apps are the killer apps for Blu-ray players." Of course, Netflix execs would likely say that streaming apps are also the killer apps for game devices, Internet-connected TVs and every other device it is integrating its Watch Instantly software into. I've been generally pessimistic about Blu-ray's prospects, but price cuts and streaming could finally move the sales needle in a bigger way.

3. Apple lurks, but how long will it stay quiet in video? - The week got off to a bang with a report that Apple is floating a $30/mo subscription idea by TV networks. While I think the price point is far too low for Apple to be able to offer anything close to the comprehensive content lineup current video service providers have, it was another reminder that Apple lurks as a major potential video disruptor. How long will it stay quiet is the key question.

While in my local Apple store yesterday (yes I'm preparing to finally ditch my PC and go Mac), I saw the new 27 inch iMac for the first time. It was a pretty stark reminder that Apple is just a hair's breadth away from making TVs itself. Have you seen this beast yet? It's Hummer-esque as a workstation for all but the creative set, but, stripped of some of its computing power to cost-reduce it, it would be a gorgeous smaller-size TV. Throw in iTunes, a remote, decent content, Apple's vaunted ease-of-use and of course its coolness cachet and the company could fast re-order the subscription TV industry, not to mention the TV OEM industry. The word on the street is that Apple's next big product launch is a "Kindle-killer" tablet/e-reader, so it's unlikely Steve Jobs would steal any of that product's thunder by near-simultaneously introducing a TV. If a TV's coming (and I'm betting it is), it's likely to be 2H '10 at the earliest.

4. Get ready for the "Anywhere" revolution - Yesterday I had the pleasure of listening to Emily Green, president and CEO of tech research firm Yankee Group, deliver a keynote in which she previewed themes and data from her forthcoming book, "Anywhere: How Global Connectivity is Revolutionizing the Way We Do Business." Emily is an old friend, and 15 years ago when she was a Forrester analyst and I was VP of Biz Dev at Continental Cablevision (then the 3rd largest cable operator), she was one of the few people I spoke to who got how important high-speed Internet access was, and how strategic it would become for the cable industry. 40 million U.S. cable broadband homes later (and 70 million overall) amply validates both points.

Emily's new book explores how the world will change when both wired and wireless connectivity are as pervasive as electricity is today. No question the Internet and cell phones have already dramatically changed the world, but Emily makes a very strong case that we ain't seen nothing yet. I couldn't help but think that TV Everywhere is arriving just in time for video service providers whose customers increasingly expect their video anywhere, anytime and on any device. "Anywhere" will be a must-read for anyone trying to make sense of how revolutionary pervasive connectivity is.

Enjoy your weekends!

Categories: Aggregators, Books, Broadcasters, Cable Networks, Cable TV Operators, Devices

Topics: Best Buy, Bl, Cablevision, CBS, Comcast, DirecTV, Netflix, News Corp, Rainbow, Time Warner Cable, Time Warner. Discovery, Viacom

-

VideoNuze Report Podcast #36 - October 16, 2009

Daisy Whitney and I are pleased to present the 36th edition of the VideoNuze Report podcast, for October 16, 2009.

This week Daisy and I first discuss my post from yesterday, "Can Advertising Alone Support Premium Long-Form Online Video?" which picks up on the in-depth discussion panelists had at this week's VideoSchmooze event in NYC. As I said in the post, this is a crucial issue, particularly for broadcast TV networks who have aggressively pursued online distribution of their primetime programs, but have yet to demonstrate they can generate the same revenue per program per viewer online as they do on-air. In the podcast, Daisy explains why she thinks that something has to break, and that a "survival of the fittest," dynamic looms for broadcast networks.

Moving on, Daisy then discusses her New Media Minute episode this week, in which she describes the success that Univision, the Spanish-language network, is having with online-only shows. Univision is so bullish on the format that Kevin Conroy, a company executive, recently told Daisy that he is actively soliciting pitches. Details on the growth in Internet usage among the Hispanic audience underscore why Univision is hitting its stride online.

Click here to listen to the podcast (12 minutes, 44 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Advertising, Broadcasters, Podcasts

-

Can Advertising Alone Support Premium Long-Form Online Video?

This was the question I started our VideoSchmooze panel discussion off with this past Tuesday night. Yet 20 minutes of debate among our group of panelists yielded no real answers. This lack of consensus suggests an upcoming period of high anxiety in the industry: for even as viewers shift to online consumption, it is far from clear whether advertising alone will be sufficient to support the creative infrastructure needed to produce premium long-form video.

I continue to believe that broadcast TV networks are the companies most at risk from the unknowns around online video advertising. Lacking the additional revenue stream from distributors that their cable TV network brethren enjoy, broadcast networks must figure out how to make online video advertising work.

However, as I originally wrote over a year ago, and then again here, the fundamental problem the broadcast networks face with their current online implementations is that ad revenue per viewer per program is a fraction of what it is on-air (likely less than 25% by my calculations). In my mind, getting the two into balance is the minimum requirement for the networks to keep their top lines even with where they are today, assuming online viewership substitutes for on-air, as I expect it will over time.

As our panel explained though, the constraints to achieving this parity are significant. First is the issue of just how many ads can be inserted into an online episode. Today sites like Hulu, with their very light ad loads bias significantly in favor of the consumer experience rather than revenue optimization (for more on this see Chuck Salter's fine new article, "Can Hulu Save Traditional TV?" in this month's Fast Company). Just how many ads can be forced into an online episode given the DVR ad-skipping generation's expectations is an unknown. For sure it is fewer than the 16-18 minutes in a traditional one hour on-air program.

So if the quantity of ads must be lower, then each one needs to bring a higher price than their on-air counterparts. The traditional "CPM" metric (the cost per thousand viewers reached) is well-entrenched among ad agency media buyers. On the VideoSchmooze panel, George Kliavkoff, now a Hearst executive, but formerly the chief digital officer at NBCU and the first CEO of Hulu, lamented the CPM framework for online video advertising. He threw down the gauntlet, saying essentially that the whole broadband video industry is in for big trouble if it doesn't break out of selling ads on a CPM basis.

George's point was that it's foolish for a new medium like broadband, which offers content providers new technology-based ways to create value for advertisers, to allow itself to get locked in to the monetization techniques from the prior TV medium. That rationale is compelling enough, but for me another strong reason to get beyond CPM pricing is that not doing so means that media buyers will always be presented with a fundamental question: is it worth paying a 25%/50%/100% (take your pick) premium to reach online vs. on-air eyeballs watching the exact same show? This raises the bar for online ads; the research must show demonstrably higher engagement, recall, purchase intent, etc. to justify the premium. All of this may happen due to online's improved targeting, but even if it does, it won't happen overnight and the upside is likely not that large anyway.

If CPM-based pricing is challenged, then what's better? On the panel we discussed examples of interactive ads that can be quantifiably valued, such as by generating a specific lead or purchase for the advertiser, along with other formats. Of course these ideas have been floating around the TV world for years, but have gained little traction (although it is worth noting that in online, paid search marketing is a pure performance ad format that has worked spectacularly well). As several attendees remarked to me afterward though, these new ad formats face the additional challenge of needing to conform to ad agencies' buying processes, which are research-driven, dominated by younger staffers and not well-suited to understanding innovative ad formats.

Add it all up and significant questions remain about whether advertising alone is going to be able to support premium long-form online video and the creative infrastructure that produces it. Just as newspapers are struggling today to support traditional newsroom expenses on skimpier online ad revenues, broadcast networks accustomed to spending $2 million or more for a single episode of a scripted program could face a similar day of reckoning. This is the core issue, made all the more urgent by viewers' relentless shift to online consumption. Only time will tell whether there are any satisfactory answers to be had here.

What do you think? Post a comment now.

Categories: Advertising, Broadcasters

Topics: Hulu, VideoSchmooze

-

4 Items Worth Noting (Hulu, TiVo-Emmys, GAP-VMIX, Long Tail) for Sept 21st Week

Following are 4 news items worth noting from the week of Sept. 21st:

1. Bashing Hulu gains steam - what's going on here? - These days everyone seems to want bash Hulu and its pure ad-supported business model for premium content. Last week it was Soleil Securities releasing a report that Hulu costs its owners $920 per viewer in advertising when they shift their viewership. This week, it was a panel of industry executives turn. Then a leaked email from CBS's Quincy Smith showed his dissatisfaction with Hulu, and interest in trying to prove it is the cause of its parent networks' ratings declines.

What's happening here is that the world is waking up to the fact that although Hulu's user experience is world-class, its ad model implementation is simply too light to be sustainable. I wrote about this a year ago in "Broadcast Networks' Use of Broadband Video is Accelerating Demise of their Business Model," following up in May with "OK, Hulu Now Has ABC. But When Will it Prove Its Business Model?" Content executives are finally realizing that it is still too early to put long form premium quality video online for free. Doing so spoils viewers and reinforces their expectation that the Internet is a free-only medium. When TV Everywhere soon reasserts the superiority of hybrid pay/ad models, ad-only long-form sites are going to get squeezed. At VideoSchmooze on Oct 13th, we have Hulu's first CEO George Kliavkoff on our panel; it's going to be a great opportunity to understand Hulu's model and dig further into this whole issue.

2. TiVo data on ad-skipping for Emmy-winning programs should have TV industry alarmed - As if ad-skipping in general wasn't already a "hair-on-fire" problem for TV executives, research TiVo released this week on ad-skipping behavior specifically for Emmy-winning programs should have the industry on DEFCON 1 alert. Using data from its "Stop | Watch" ratings service, TiVo found that audiences for the winning programs in the 5 top Emmy categories - Outstanding Comedy Series, Drama Series, Animated Program, Reality-Competition and Variety/Music/Comedy Series - all show heavier than average (for their genre) time-shifting. The same pattern is true for ad-skipping; the only exception is "30 Rock" (winner of Outstanding Comedy Series) which performs slightly better than its genre average.

The numbers for AMC's "Mad Men" (winner of Outstanding Drama Series), are particularly eye-opening: 85% of the TiVo research panel's viewers time-shifted, and of those, 83% ad-skipped. (Note as an avid Mad Men viewer, I've been doing both since the show's premiere episode. It's unimaginable to me to watch the show at its appointed time, and with the ads.) The data means that even when TV execs produce a critical winner, their ability to effectively monetize it is under siege. How long will BMW sign up to be Mad Men's premier sponsor with research like this? TiVo's time-shifting data shows why network executives have to get the online ad model right. When TV Everywhere launches it will cater to massive latent interest in on-demand access by viewers; it is essential these views be better monetized than Hulu, for example, is doing today.

3. Radio stations push into online video as GAP Broadcasting launches with VMIX - Lacking its own video, the radio industry has been a little bit of the odd man out in the online video revolution. Some of the industry's bigger players like Clear Channel have jumped in, but there hasn't been a lot of momentum, especially with the ad downturn. But this week GAP Broadcasting, owner of 116 stations in mostly smaller markets announced a partnership with video platform and content provider VMIX. I talked to VMIX CEO Mike Glickenhaus who reported that radio stations are starting to get on board. For GAP, VMIX is providing an online video platform, premium content from hundreds of licensed partners, user-generated video tools and sales training, among other things. GAP's goal is to be a "total audience engagement platform" not just a radio station. Sounds right, but there's lots of hard work ahead.

4. So is there a "Long Tail" or isn't there? Ever since Chris Anderson's book "The Long Tail" appeared in 2006 there have been researchers challenging his theory which asserts that infinite shelf space drives customer demand into the niches. The latest attempt is by 2 Wharton professors, who, using Netflix data, observe that the Long Tail effect is not ironclad. Sometimes it's present, sometimes it's not. Anderson disputes their findings. The argument boils down to the definitions of the "head" and "tail" of the markets being studied. Anderson defines them in absolute terms (say the top 100 products), whereas the Wharton team defines them in terms of percentages (the top 1 %).

I've been fascinated with the Long Tail concept since the beginning, as it potentially represents a continued evolution of video choice; over-the-air broadcasting allowed for 3 channels originally, cable then allowed for 30, 50, 500, now broadband creates infinite shelf space. Independent online video producers and their investors have bet on the Long Tail effect working for them to drive viewership beyond broadcast and cable. With Nielsen reporting hours of TV viewership holding steady, we haven't yet seen cannibalization. However, with Nielsen, comScore and others reporting online video consumption surging, audiences may be carving out time from other activities to go online and watch.

Enjoy your weekends! There will be no VideoNuze on Monday as I'll be observing Yom Kippur.

Categories: Advertising, Aggregators, Broadcasters, Indie Video, Radio

Topics: AMC, GAP Broadcasting, Hulu, Long Tail, Netflix, VMIX

-

Titans-Steelers on NBCSports.com Last Night Was Impressive

I was only able to catch a little bit of the Titans-Steelers came last night on NBCSports.com, but what I did see was pretty impressive. This was the first of the "Sunday Night Football Extra" games that NBC Sports

and the NFL plan to stream live this season. NBC Sports is using Silverlight for the first time, and the live HD broadcast included 5 different camera angles to choose from. Akamai is providing CDN services and Microsoft's Smooth Streaming for delivery.

and the NFL plan to stream live this season. NBC Sports is using Silverlight for the first time, and the live HD broadcast included 5 different camera angles to choose from. Akamai is providing CDN services and Microsoft's Smooth Streaming for delivery. NBC has been a pioneer in the delivery of online sports content, and with the 2008 Beijing Olympics setting a new standard. The NFL is not alone in pushing into online delivery though. As I noted recently in "2009 is a Big Year for Sports and Broadband/Mobile Video," there have been a ton of new initiatives this year across baseball, basketball, football, golf, tennis, auto racing, etc.

I'm looking forward to having Perkins Miller, SVP, Digital Media and GM, Universal Sports, NBCU Sports and Olympics on my discussion panel at VideoSchmooze on Mon evening, Oct 13th in NYC. No doubt he'll have lots of great insights and data to share about how the season is progressing.

The next game on NBCSports.com is this Sun night, Bears vs. Packers, 8pm ET.

Categories: Broadcasters, Sports, Technology

Topics: Akamai, Microsoft, NBC Sports, NFL, Silverlight

-

VideoNuze Report Podcast #30 - September 4, 2009

Daisy Whitney and I are pleased to present the 30th edition of the VideoNuze Report podcast, for September 4, 2009.

This week Daisy shares more detail from her most recent New Media Minute, concerning what broadcast networks are doing this Fall with online video extensions of their shows. For example, CW is launching an original series in conjunction with "Melrose Place." ABC is doing a 3rd season of an "Ugly Betty" web series and a tie-in for "Lost." CBS is launching its first web series, via TV.com, with Julie Alexandria, focused on recapping highlights from various shows. Daisy notes that these efforts are focused mainly on marquee shows and when advertisers are already on board.

In the 2nd part of the podcast we discuss my post from yesterday, "2009 is a Big Year for Sports and Broadband/Mobile Video." In that post I observed that many big-time sports, and the TV networks that have the rights to televise them have realized this year that broadband and mobile distribution are friend, not foe. As a result they've rolled out many different initiatives. We also touch on the various lessons other content providers can take away from what's happening with sports and broadband/mobile distribution.

Click here to listen to the podcast (13 minutes, 54 seconds)Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Broadcasters, Podcasts, Sports

Topics: ABC, CBS, CW, Podcast, TV.com

-

2009 is a Big Year for Sports and Broadband/Mobile Video

Pick your favorite sport - baseball, basketball, football, golf, tennis, auto racing, etc. and it's likely that in 2009 some part of the action has been available via broadband or mobile video. 2009 is looking like the year that sports executives - and the TV network honchos that pay dearly for sports' broadcast rights- concretely realized that broadband and mobile complement traditional sports broadcasting and that they should be embraced, not spurned.

In VideoNuze's News Roundup, I've been keeping track of all the broadband and mobile sports headlines this year. Here's just a partial list of what I've captured, along with links:

- PGATour.com to Offer Live Video Streams of Key Holes for Tour Playoffs (B&C)

- U.S. Open to Stream Almost All Matches Online (PaidContent)

- DirecTV Offers NFL Sunday Ticket via Internet in NY Trial (USA Today)

- "Live at Wimbledon" Streaming Coverage Announced by NBC (Sports Media News)

- Cablevision Subs Will Gain Access to In-Market Streaming of YES's Yankee Telecasts (Multichannel News)

- MLB.com Streams Live Baseball Games to the iPhone (NYTimes Bits)

- NBA Playoffs to Stream on Android App (Online Media Daily)

- Speedtv.com to Stream Part of Le Mans 24 Hours (Multichannel News)

- NHL to Launch Daily Stanley Cup Pre-game Web Series (Mediaweek - reg required)

- Follow the Masters on Your iPhone (Electronic House)

- March Madness! YouTube Gets Live Video via Silverlight (NewTeeVee)

In some cases the initiatives provide specially-produced video, while in other cases they offer streams that are already available on TV. The former type isn't that surprising as supplementary video can add a lot of value to the main event (the analog in entertainment are the popular "behind-the-scenes" extras that come with DVDs).

It's the latter type - where broadcast streams are delivered via broadband or mobile, either live or on-demand - that is much more intriguing as it represents a big step forward in sports and TV network executives' thinking about multi-platform distribution. Traditionally the approach has been to tell fans when the sporting event was on and on which network to find it. But with these broadband and mobile efforts, increasingly we're seeing executives scrap that model and replace it with a more fan-friendly approach that seeks to bring the action to fans, on-demand and wherever they might be.

In my view, this is a welcome change. Regrettably, big-time sports are now all about big-time money. To understand the stakes, I'm fond of reminding people to do the math on what just ESPN rakes in on just its U.S. monthly affiliate fee of approximately $3.75 from cable operators, satellite operators and telcos carrying the channel into 90 million + homes (your calculator may run out of zeros if you try). With that kind of money on the line, it's imperative that networks and sports themselves figure out how to harness new technologies to deliver more value. From the looks of 2009's initiatives, they appear to be well on their way.

What do you think? Post a comment now.

Categories: Broadcasters, Cable Networks, Sports

Topics: ESPN

-

4 Items Worth Noting from the Week of August 17th

Following are 4 news items worth noting from the week of August 17th:

CBS's Smith says authentication is a 5 year rollout - I had a number of people forward me the link to PaidContent's in-depth coverage of CBS Interactive CEO Quincy Smith's comments at the B&C/Multichannel News panel in which he asserted that TV Everywhere/authentication won't gain critical mass until 2014.

I was asked what I thought of that timeline, and my response is that I think Smith is probably in the right ballpark. However, these rollouts will happen on a company by company basis so timing will vary widely. Assuming Comcast's authentication trial works as planned, I think it's likely to expect that Comcast will have its "On Demand Online" version of TV Everywhere rolled out to its full sub base within 12 months or so. Time Warner Cable is likely to be the 2nd most aggressive in pursuing TV Everywhere. For other cable operators, telcos and satellite operators, it will almost certainly be a multi-year exercise.

NFL makes its own broadband moves - While MLB has been getting a lot of press for its recent broadband and mobile initiatives, I was intrigued by 2 NFL-related announcements this week that show the league deepening its interest in broadband distribution. First, as USA Today reported, DirecTV will offer broadband users standalone access to its popular "Sunday Ticket" NFL package. The caveat is that you have to live in an area where satellite coverage is unattainable. The offer, which is being positioned as a trial, runs $349 for the season. With convergence devices like Roku hooking up with MLB.TV, it has to be just a matter of time before the a la carte version of Sunday Ticket comes to TVs via broadband as well.

Following that, yesterday the NFL and NBC announced that for the 2nd season in a row, the full 17 game Sunday night schedule will be streamed live on NBCSports.com and NFL.com. Both will use an HD-quality video player and Microsoft's Silverlight. They will also use Microsoft's Smooth Streaming adaptive bit rate (ABR) technology. All of this should combine to deliver a very high-quality streaming experience. But with all these games available for free online, I have to wonder, are NBC and the NFL leaving money on the table here? It sure seems like there must have been some kind of premium they could have charged, but maybe I'm missing something.

Metacafe grows to 12 million unique viewers in July - More evidence that independent video aggregators are hanging in there, as Metacafe announced uniques were up 67% year-over-year and 10% over June (according to comScore). I've been a Metacafe fan for a while, and their recent redesign around premium "entertainment hubs" has made the site cleaner and far easier to use. Metacafe's news follows last week's announcement by Babelgum that it grew to almost 1.7 million uniques in July since its April launch. Combined, these results show that while the big whales like YouTube and Hulu continue to capture a lot of the headlines, the minnows are still making swimming ahead.

Kodak introduces contest to (re)name its new Zi8 video camera - It's not every day (or any day for that matter) that I get to write how a story in a struggling metro newspaper had the mojo to influence a sexy new consumer electronic product being brought to market by an industrial-era goliath, so I couldn't resist seizing this opportunity.

It turns out that a review Boston Globe columnist Hiawatha Bray wrote, praising Kodak's new Zi8 pocket video camera, but panning its dreadful name, prompted Kodak Chief Marketing Officer Jeffrey Hayzlett to launch an online contest for consumers to submit ideas for a new name for the device, which it intends to be a Flip killer. Good for Hayzlett for his willingness to change course at the last minute, and also try to build some grass roots pre-launch enthusiasm for the product. And good for the Globe for showing it's still relevant. Of course, a new name will not guarantee Kodak success, but it's certainly a good start.

Enjoy your weekend!

Categories: Aggregators, Broadcasters, Cable TV Operators, Devices, Indie Video, Sports

Topics: Babelgum, Boston Globe, CBS, Comcast, Kodak, MetaCafe, MLB, NFL, Roku, Time Warner Cable

-

Hulu is Broadcast TV Networks' Best Bet for Generating Online Video Payments

Last Monday, in "Netflix's ABC Deal Shows Streaming Progress and Importance of Broadcast TV Networks," I tried making the case that from Netflix's perspective, in order for its Watch Instantly streaming service to succeed, it would most likely need to strike more deals with the broadcast TV networks (as it announced with ABC).

Now how about the flip side of the question: how can broadcast TV networks make online video payments a significant revenue stream?

There is certainly no lack of interest by broadcasters in getting paid for online access to their content. For example, CBS has joined Comcast's TV Everywhere trial, and its CEO Leslie Moonves has been outlining his arguments for why cable's authentication plans should generated new revenue for the network. News Corp head (and Fox owner) lately Rupert Murdoch hasn't been shy about his interest in charging for content, though his first focus appears to be on newspapers. And Disney CEO Bob Iger (and ABC owner), recently told the WSJ, "People are going to pay for content. We are not worried about that." Meanwhile NBC's Jeff Zucker is trying to reposition NBCU as a cable network company (i.e. one that sells ads AND gets paid for its programs).

For broadcast TV networks though, figuring out how to get paid for online distribution is not trivial. Years of giving viewers free access to their shows has set expectations. Consider for example recent CBS research in which respondents were asked if they could watch a program online for free with commercials or pay $1.99 for it; 92% chose the former. This echoes mountains of research that has reached similar conclusions (a conundrum likewise bedeviling newspapers who are also seeking to charge for their content).

As I think through how broadcasters can succeed with getting paid, I keep returning to 3 core beliefs: first, broadcasters' efforts should not be undertaken individually, but rather through its joint initiative Hulu, second, the model needs to be subscription-based, not per program-based and third, the subscription service should be made in partnership with incumbent video service providers (cable, satellite, Netflix, etc.) and convergence device makers (Roku, Xbox, etc.).

Hulu has established a strong online brand, built a large audience and demonstrated online savvy. I have the most confidence in Hulu to be able to identify the differentiators needed to drive new value vs. free,

including things like more timely access to hit programs, deeper libraries, higher quality streaming, options for downloading and mobile, etc. And assuming the federal government didn't step in and cry "collusion!" Hulu would provide the greatest negotiating leverage.

including things like more timely access to hit programs, deeper libraries, higher quality streaming, options for downloading and mobile, etc. And assuming the federal government didn't step in and cry "collusion!" Hulu would provide the greatest negotiating leverage. The key challenge for Hulu would be gaining the rights from the networks, producers, talent and others to launch such a comprehensive service. These stakeholders would be understandably wary, not knowing exactly how to value what they'd be providing.

Several months ago, I suggested a Hulu subscription service was in the offing, but so far Hulu has stayed on message, only emphasizing its free, ad-supported model. I hope it and its parents recognize that time is of the essence. With each passing day, as more people use Hulu ever more intensively, their expectations for free are being set, thereby raising the bar on their eventual willingness to pay. I do believe broadcast networks have any opportunity to evolve their business model and charge, but they must not dither. The online medium is still immature enough that they can influence its rules by acting now.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters

Topics: ABC, CBS, FOX, Hulu, NBC

-

Netflix's ABC Deal Shows Streaming Progress and Importance of Broadcast TV Networks

Yesterday's announcement by Netflix that it will be adding to its Watch Instantly library past seasons ABC's "Lost," "Desperate Housewives," "Grey's Anatomy" and "Legend of the Seeker" is another step forward for Netflix in strengthening its online competitiveness.

At a broader level though, I think it's also further evidence that the near-term success of Watch Instantly and other "over-the-top" broadband video services is going to be tied largely to deals with broadcast TV networks, rather than film studios, cable TV networks or independently-produced video sources.

Key fault lines are beginning to develop in how premium programming will be distributed in the broadband era. Content providers who have traditionally been paid by consumers or distributors in one way or another are redoubling their determination to preserve these models. Examples abound: the TV Everywhere initiative Comcast/Time Warner are espousing that now has 20+ other networks involved; Epix, the new premium movie service backed by Viacom, Lionsgate and MGM; new distribution deals by the premium online service ESPN360.com, bringing its reach to 41 million homes; MLB's MLB.TV and At Bat subscription offerings; and Disney's planned subscription services. As I wrote last week in "Subscription Overload is On the Horizon," I expect these trends will only accelerate (though whether they'll succeed is another question).

On the other hand, broadcast TV networks, who have traditionally relied on advertising, continue mainly to do so in the broadband world, whether through aggregators like Hulu, or through their own web sites. However, ABC's deal with Netflix, coming on top of its prior deals with CBS and NBC, shows that broadcast networks are both motivated and flexible to mine new opportunites with those willing to pay.

That's a good thing, because as Netflix tries to build out its Watch Instantly library beyond the current 12,000 titles, it is bumping up against two powerful forces. First, in the film business, well-defined "windows"

significantly curtail distribution of new films to outlets trying to elbow their way in. And second, in the cable business, well-entrenched business relationships exist that disincent cable networks from offering programs outside the traditional linear channel affiliate model to new players like Netflix. These disincentives are poised to strengthen with the advent of TV Everywhere.

significantly curtail distribution of new films to outlets trying to elbow their way in. And second, in the cable business, well-entrenched business relationships exist that disincent cable networks from offering programs outside the traditional linear channel affiliate model to new players like Netflix. These disincentives are poised to strengthen with the advent of TV Everywhere.In this context, broadcast networks represent Netflix's best opportunity to grow and differentiate Watch Instantly. Last November in "Netflix Should be Aggressively Pursuing Broadcast Networks for Watch Instantly Service," I outlined all the reasons why. The ABC deal announced yesterday gives Netflix a library of past seasons' episodes, which is great. But it doesn't address where Netflix could create the most value for itself: as commercial-free subscription option for next-day (or even "next-hour") viewing of all prime-time broadcast programs. That is the end-state Netflix should be striving for.

I'm not suggesting for a moment that this will be easy to accomplish. But if it could, Netflix would really enhance the competitiveness of Watch Instantly and its underlying subscription services. It would obviate the need for Netflix subscribers to record broadcast programs, making their lives simpler and freeing up room on their DVRs. It would be jab at both traditional VOD services and new "network DVR" service from Cablevision. It would also be a strong competitor to sites like Hulu, where comparable broadcast programs are available, but only with commercial interruptions. And Hulu still has limited options for viewing on TVs, whereas Netflix's Watch Instantly options for viewing on TVs includes Roku, Xbox, Blu-ray players, etc. Last but not least, it would also be a powerful marketing hook for Netflix to use to bulk up its underlying subscription base that it intends to transition to online-only in the future.

Beyond next-day or next-hour availability, Netflix could also offer things like higher-quality full HD delivery or download options for offline consumption. Broadcasters, who continue to be pinched on the ad side, should be plenty open to all of the above, assuming Netflix is willing to pay.

I continue to believe Netflix is one of the strongest positions to create a compelling over-the-top service offering. But with numerous barriers in its way to gain online distribution rights to films and cable programs, broadcast networks remain its key source of premium content. So keep an eye for more deals like the one announced with ABC yesterday, hopefully including fast availability of current, in-season episodes.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, Cable TV Operators, FIlms

Topics: ABC, Cablevision, CBS, Comcast, EPIX, ESPN360, MLB, NBC, Netflix, Time Warner

-

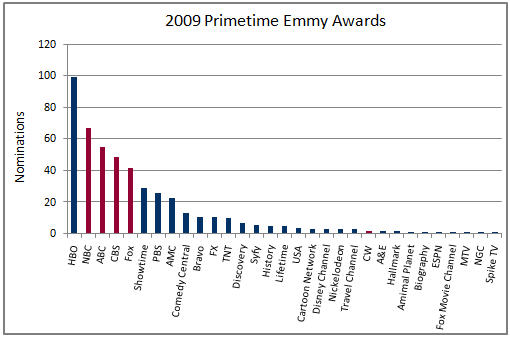

Cable's Emmy Nominations Illustrate Cord-Cutting's Challenge

Last week when the primetime Emmy award nominees were announced, cable programs turned in another strong performance, garnering 272 of the 487 nominations. The Emmys and other awards illustrate one of the key challenges for would-be cord-cutters: outside of per-program download options (e.g. iTunes) that will persist, in the coming TV Everywhere world, virtually none of cable's award-winning programming will be accessible online unless you subscribe to a cable/satellite/telco service provider. This is a critical fact in understanding how the broadband video world is going to unfold.

One of the reasons TV Everywhere is so compelling is that it offers cable networks an on-ramp to online distribution while preserving their existing - and increasingly valuable - dual revenue (monthly affiliate fees and advertising) business model. As more content executives are concluding that advertising alone will not be sufficient for profitable long-form program distribution online, the payments cable networks receive from cable/satellite/telco providers is more valuable than ever. TV Everywhere's online access will inevitably lead to heavier viewership and enhanced loyalty.

The Emmy nominations show the expanding breadth of cable's quality. As the below chart depicts, this year 26 different cable networks' programs were nominated, with HBO, the perennial leader picking up 99 nominations (it should be noted that last week HBO signed on to Comcast's On Demand Online technical trial, further entrenching HBO in the cable world, therefore dimming the notion that HBO will ever be available outside the traditional premium subscription model).

Cable's strength is even better understood by looking at the major Emmy award categories. For example, in the outstanding drama series category, cable got 5 of 7 nominations (AMC-2, FX, HBO, Showtime). In the outstanding children's program category, cable got all 3 nominations (Disney Channel-2 and Nickelodeon). In the outstanding reality program series category, cable got 5 of 6 nominations (A&E, Bravo, Discovery-2, NGC). Even in outstanding comedy series, cable got 3 of 7 nominations (HBO-2, Showtime).

When TV Everywhere gets fully rolled out, cable networks will have little-to-no incentive to make much of their programming available to non-paying video subscribers. That means that the Hulus of the world will have to content themselves with a catalog of broadcast programs, older movies and made-for-broadband series. As broadcast's Emmy nominations show, that still means there's plenty of popular content to drive online audience. But until Hulu figures out a subscription model, it (and its content suppliers) will be economically disadvantaged to cable both on-air and online. This is no small issue given each TV program episode now costs $2-3 million to produce.

Meanwhile, consumers will make their own video choices. If they choose to cut the cord they won't have subscription-based online access to programs like Entourage, Weeds, MythBusters, Hannah Montana, Mad Men or Dexter, not to mention top-shelf sports from ESPN, TNT and others. For some people eager to cut the cord, that will be just fine. But I'm betting that for the majority of viewers that would be unacceptable and they'll continue to choose to subscribe. TV Everywhere can use cable programs' popularity to blunt cord-cutting before it ever takes off and cement cable's appeal in the broadband era.

What do you think? Post a comment now.

Categories: Broadcasters, Cable Networks, Cable TV Operators

Topics: Comcast, HBO, TV Everywhere

-

Comcast Adds CBS and 17 More Cable Nets to On Demand Online Trial

Another day, another flurry of announcements from Comcast with news of more networks participating in its On Demand Online technical trial. Newly on board are CBS (also the first broadcast network to participate) and 17 more cable networks such as A&E, AMC, BBC America, Food Network, History Channel, Sundance and others. Together with those already announced, there are now over 20 networks in the trial.

The cable networks' interest isn't surprising. I've been saying for a while that On Demand Online will be a real boon to them, providing a secure, scalable on-ramp to online distribution, new ad impressions and most important, significant enhanced value to their viewers. Still, despite all of Comcast's progress, most of the big cable network groups (e.g. NBCU, Fox, Disney, Viacom, Discovery) have not yet publicly signed on. I think that's just a matter of time.

There's no question Comcast is building real industry momentum for On Demand Online. But given the trial hasn't even begun yet, all of these announcements are really raising the visibility of the trial - and of course

the pressure to make sure its "authentication" processes work as intended. No doubt each of these announcements is creating a lot of sweaty palms among Comcast's technical staff - the people who are responsible for proving authentication works. With all the PR buildup, if for some reason all does not go according to plan, Comcast will have lots of people looking for answers.

the pressure to make sure its "authentication" processes work as intended. No doubt each of these announcements is creating a lot of sweaty palms among Comcast's technical staff - the people who are responsible for proving authentication works. With all the PR buildup, if for some reason all does not go according to plan, Comcast will have lots of people looking for answers.From my perspective though, I'd like to see Comcast tamp down the PR machine for now and focus on executing the trial itself. The point has now been amply made that the cable network community wants to play ball with On Demand Online. Comcast needs to make the trial a resounding success and then fill in details about how the rollout will proceed.

What do you think? Post a comment now.

Categories: Broadcasters, Cable Networks, Cable TV Operators

-

Catching Up on Last Week's Industry News

I'm back in the saddle after an amazing 10 day trip to Israel with my family. On the assumption that I wasn't the only one who's been out of the office around the recent July 4th holiday, I've collected a batch of industry news links below so you can quickly get caught up (caveat, I'm sure I've missed some). Daily publication of VideoNuze begins again today.

Hulu plans September bow in U.K.

Rise of Web Video, Beyond 2-Minute Clips

Nielsen Online: Kids Flocking to the Web

Amid Upfronts, Brands Experiment Online

Clippz Launches Mobile Channel for White House Videos

Prepare Yourself for iPod Video

Study: Web Video "Protail" As Entertaining As TV

In-Stat: 15% of Video Downloads are Legal

Kazaa still kicking, bringing HD video to the Pre?

Office Depot's Circuitous Route: Takes "Circular" Online, Launches "Specials" on Hulu

Upload Videos From Your iPhone to Facebook Right Now with VideoUp

Some Claims in YouTube lawsuit dismissed

Concurrent, Clearleap Team on VOD, Advanced Ads

Generating CG Video Submissions

MJ Funeral Drives Live Video Views Online

Why Hulu Succeeded as Other Video Sites Failed

Invodo Secures Series B Funding

Comcast, USOC Eye Dedicated Olympic Service in 2010

Consumer Groups Push FTC For Broader Broadband Oversight

Crackle to Roll Out "Peacock" Promotion

Earlier Tests Hot Trend with "Kideos" Launch

Mobile entertainment seeking players, payment

Netflix Streams Into Sony Bravia HDTVs

Akamai Announces First Quarter 2009 State of the Internet Report

Starz to Join Comcast's On-Demand Online Test

For ManiaTV, a Second Attempt to be the Next Viacom

Feeling Tweety in "Web Side Story"

Most Online Videos Found Via Blogs, Industry Report

Categories: Advertising, Aggregators, Broadcasters, Cable Networks, Cable TV Operators, CDNs, Deals & Financings, Devices, Indie Video, International, Mobile Video, Technology, UGC

Topics: ABC, C, Clearleap, Clippz, Comcast, Concurrent, Hulu, In-Stat, Invodo, iPod, Kazaa, Nielsen, Office Depot, Qik, VideoUp, YouTube

-

4 Industry Items from this Week Worth Noting

YouTube mobile video uploads exploding; iPhones are a key contributor - The folks at YouTube revealed that in the last 6 months, uploads from mobile phones to YouTube have jumped 1,700%, while in the last week, since the new iPhone GS was released, uploads increased by 400% per day. I didn't have access to these stats when I wrote on Monday "iPhone 3GS Poised to Drive User-Generated Mobile Video," but I was glad to see some validation. The iPhone 3GS - and other smartphone devices - will further solidify YouTube as the world's central video hub. I stirred some controversy last week with my "Does It Actually Matter How Much Money YouTube is Losing?" post, yet I think the mobile video upload explosion reinforces the power of the YouTube franchise. Google will figure out how to monetize this over time; meanwhile YouTube's pervasiveness in society continues to grow.

Nielsen study debunks mythology around teens' media usage - Nielsen released a new report this week "How Teens Use Media" which tries to correct misperceptions about teens' use of online and offline media. The report is available here. On the one hand, the report underscores prior research from Nielsen, but on the other it reveals some surprising data. For example, more than a quarter of teens read a daily newspaper? Also, 77% of teens use just one form of media at one time (note, data from 2007)? I'm not questioning the Nielsen numbers, but they do seem out of synch with everything I hear from parents of teens.

Paid business models resurfacing - There's been a lot of talk from media executives about the revival of paid business models in the wake of the recession's ad spending slowdown and also the newspaper industry's financial calamity. For those who have been offering their content for free for so long, putting the genie back in the bottle is going to be tough. Conversely for others, like those in the cable TV industry, who have resisted releasing much content for free, their durable paid models now look even more attractive.

Broadcast TV networks diverge on strategy - Ad Age had a good piece this week on the divergence of strategy between NBC and CBS. The former is breaking industry norms by putting Leno on at 10pm, emphasizing cable and avidly pursuing new technologies. Meanwhile CBS is focused on traditional broadcast network objectives like launching hit shows and amassing audience (though to be fair it is pursuing online distribution as well with TV.com). Both strategies make sense in the context of their respective ratings' situations. Regardless, broadcasters need to eventually figure out how to successfully transition to online distribution, something that is still unproven (as I wrote here).

Categories: Aggregators, Broadcasters, Mobile Video, UGC

Topics: Apple, CBS, iPhone, NBC, Nielsen, YouTube

Posts for 'Broadcasters'

Connect with VideoNuze

Exclusive News Roundup

- ‘Jeopardy!’ Plans YouTube Spinoff Show as It Ramps Up Production on Platform The Hollywood Reporter

- Netflix Raising U.S. Prices for Second Time in Less Than Two Years Variety

- Walmart, Vizio Link Content To Commerce At NewFronts Mediapost

- Deloitte: 68% of Streamers Choose Less-Expensive Ad-Supported Plan Media Daily News

- Samsung, Amazon Ads Form Shoppable CTV Partnership Mediapost

- OpenAI drops AI video tool Sora, startling Disney Reuters