-

Here's A Great Example of Why TV Everywhere Matters So Much To the Pay-TV Industry

Want a really tangible example of why TV Everywhere is so critical to the pay-TV industry? Then have a look at this post from industry banker Ken Sonenclar, who recounts his personal experience of trying to find an online version of the season finale of Showtime's "Dexter" on an evening when bad weather knocked out his satellite dish. Frustrated that he couldn't find the episode available anywhere, he ultimately stumbled upon a pirate site and happily watched the episode, albeit at somewhat lower quality.

Experiences like these no doubt play out daily as pay-TV subscribers seek convenient, on-demand access to their favorite programs. The TV Everywhere model works because it still requires a valid paid subscription, so the current monetization model is unharmed. But the incremental value to viewers is substantial. With services like Netflix and Hulu Plus increasingly available on every conceivable online and mobile device, consumers' expectations are being raised. If the pay-TV industry (both operators and networks) can't meet or exceed the experiences that a sub $10/mo service can deliver, then they shouldn't be surprised when subscribers begin dropping their expensive pay-TV services.Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

Topics: TV Everywhere

-

6 Key 2011 Trends in Online and Mobile Video

Yesterday Colin Dixon from The Diffusion Group and I presented a webinar describing our 6 key trends for 2011 in online and mobile video. Colin is one of the sharpest analysts of the pay-TV and online/mobile video industries and we had no shortage of ideas to sort through. Our list is a joint effort, and during the webinar we each presented the 3 trends we felt the strongest about. In today's post I share and explain each one. At the end of the webinar we conducted a poll asking attendees whether they agreed or disagreed with our predictions. I've noted those results in bold font. If you want to download the slides and/or hear more of our detailed discussion, just register for the on-demand version of the webinar and you'll be emailed a link.

Categories: Aggregators, Broadband ISPs, Cable TV Operators, Mobile Video, Predictions, Regulation, Satellite, Technology, Telcos

Topics: FCC, Google, Net Neutrality, Netflix, TV Everywhere

-

5 Items of Interest for the Week of Dec. 5th

Once again I'm pleased to offer VideoNuze's end-of-week feature highlighting and discussing 5-6 interesting online/mobile video industry news items that we weren't able to cover this week. Read them now or take them with you this weekend!

Categories: Advertising, Aggregators, Broadcasters, Cable TV Operators, Mobile Video, Telcos

Topics: ABC, Disney, eMarketer, Hulu Plus, Netflix, Nielsen, TV Everywhere, Verizon Wireless

-

5 Items of Interest for the Week of Nov. 29th

Following the Thanksgiving break last Friday, VideoNuze's end-of-week feature of curating 5-6 interesting online/mobile video industry news items that we weren't able to cover this week, is back. Read them now or take them with you this weekend!

Categories: Aggregators, Broadband ISPs, Devices, Mobile Video, Regulation, Telcos, UGC

Topics: Comcast, FCC, IDC, Level 3, Magid, Net Neutrality, Nielsen, Verizon Wireless, Viacom, YouTube

-

Are Live Sports Pay-TV's Firewall or Its Albatross?

I've long assumed that live sports carried on cable TV networks (e.g. ESPN, Fox Sports, TNT, TBS, NFL Network, regional sports networks, etc.) would be a key firewall against cord-cutting since the games they air are unavailable online. In other words, if you're a sports fan, dropping your pay-TV subscription would be unthinkable. While I still believe that's mostly true, recently I've started wondering if it's possible that sports actually may also be an albatross for pay-TV operators, limiting their ability to effectively compete with online-only alternatives.

I use the word albatross because pay-TV providers actually have very little flexibility to offer non-sports fans lower-priced packages that don't include sports-oriented channels. In fact, the most surprising aspect of last week's announcement by Time Warner Cable of a new lower-priced tier called "TV Essentials" it's testing is that it will exclude ESPN, which is virtually unheard-of in pay-TV packaging. Because the underlying deals that cable networks have with sports leagues and rights-holders are so expensive, the networks try to get carried on the most popular pay-TV service tiers, thereby ensuring the highest number of subscriber homes (basic cable networks are paid by distributors on a per subscriber basis, so the more subscriber homes, the higher their revenue).

Categories: Cable Networks, Cable TV Operators, Satellite, Sports, Telcos

Topics: ESPN, Fox Sports, NFL Network, TBS, Time Warner Cable, TNT

-

How About Some Actual Data in the Cord-Cutting Debate?

No sooner did SNL Kagan's press release, announcing that the U.S. pay-TV industry had lost 119K subscribers in Q3 '10, following a loss of 216K subscribers in Q2, hit the wire today, than the blogosphere was alight with a fresh round of posts that cord-cutting was to blame. This chorus was surely egged on by Kagan senior analyst Ian Olgeirson's remark in the press release that "it is becoming increasingly difficult to dismiss the impact of over-the-top substitution on video subscriber performance." That remark was a notable change of tone from Kagan's Q2 release which ascribed subscriber losses solely to the country's ongoing economic woes.

Note however that Olgeirson only offered his opinion, rather than any actual, hard data from Kagan about cord-cutting's impact. That is characteristic of both sides of the current cord-cutting debate - lots of opining, but little-to-no reliable data. In my own Q3 analysis - in which I suggested that the pay-TV as a whole likely lost around 97K subscribers in Q3 (though the group of 8 of the top 9 pay-TV operators actually gained subscribers) - I noted that nobody truly knows the impact of cord-cutting, yet anyway.

Categories: Cable TV Operators, Satellite, Telcos

Topics: SNL Kagan

-

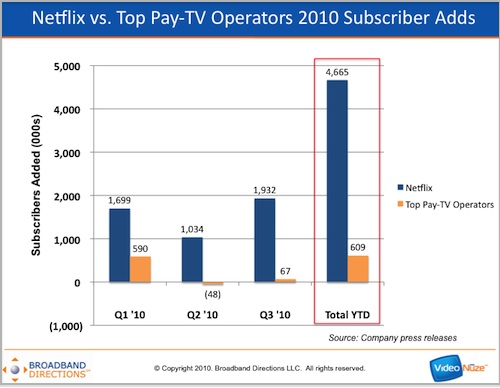

Netflix Has Added 8 Times As Many Subscribers in 2010 As Top Pay-TV Operators, Combined

Here's a pretty amazing factoid to end your week: in 2010 Netflix has added nearly 8 times as many subscribers as 8 of the top 9 pay-TV operators have, combined (#3 cable operator Cox is private and doesn't report). In the first 3 quarters of 2010, Netflix has added nearly 4.7 million subscribers while the top pay-TV operators have gained 609K.

Breaking down the pay-TV industry net gain further, the 2 main telcos (Verizon and AT&T) have added over 1.2 million subscribers and the 2 main satellite providers (DirecTV and DISH) have added 563K, while the top 4 reporting cable operators (Comcast, Time Warner Cable, Charter and Cablevision) have lost over 1.1 million.

Categories: Aggregators, Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

Top U.S. Pay-TV Operators Post Narrow Subscriber Gains in Q3, Rebounding From Q2 Loss

Eight out of the nine largest U.S. pay-TV operators have reported their Q3 '10 results, gaining a slim 66,700 video subscribers, a rebound from a loss of 47,600 subscribers in Q2 '10. The Q2 loss was the first on record for the industry and fueled speculation that "cord-cutting" due to adoption of Internet-delivered video alternatives was rising. With only mildly positive subscriber adds - and 5 of the top 8 operators actually losing subscribers in Q3 - fears that cord-cutting is rising will surely accelerate.

The 8 operators (privately-held Cox Cable, the 3rd-largest cable operator does not disclose its results) represent more than 85% of all U.S. pay-TV households. Though they collectively showed a quarterly gain, if Cox and other cable operators lost subscribers at a comparable rate as the 4 large cable operators in the top 8 (Comcast, Time Warner Cable, Charter and Cablevision), the industry as a whole would have actually lost about 97K subscribers in the 3rd quarter.

Categories: Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

Entone Introduces FusionTV To Help Telcos Blend OTT With Linear TV

IPTV vendor Entone jumped into the connected device fray today with a new managed service called "FusionTV" for telcos looking to offer a hybrid linear TV/broadband/online video package. Entone's CEO Steve McKay briefed me on the company's plans last week.

For consumers, FusionTV's appeal is that it brings together several value propositions into one user experience: linear HDTV, whole home DVR, online video and media sharing. As a result consumers don't need to buy and wire together a DVR or connected device (or multiple of these for additional rooms), and also don't need to disrupt their existing video source, whether that be telco, satellite, over-the-air, etc. For the telcos (primarily tier 2), FusionTV is a new value added service to improve the competitiveness of their broadband service, while also helping bring online video under their roof, thus preempting over-the-top cord-cutting.

together a DVR or connected device (or multiple of these for additional rooms), and also don't need to disrupt their existing video source, whether that be telco, satellite, over-the-air, etc. For the telcos (primarily tier 2), FusionTV is a new value added service to improve the competitiveness of their broadband service, while also helping bring online video under their roof, thus preempting over-the-top cord-cutting.

-

6 Items of Interest for the Week of Oct. 18th

It was another busy week for online/mobile video, and so VideoNuze is continuing its Friday practice of curating 5-6 interesting industry news items that we weren't able to cover this week. Read them now or take them with you this weekend!

Networks block Google TV to protect themselves

Yesterday news started breaking that ABC, CBS and NBC are blocking access by Google TV. There are numerous concerns being cited - potential disruption of advertising, encouraging cord-cutting, incenting piracy, diminished branding, unsatisfactory ad splits with Google, and general worry about Google invading the living room. Each item on its own is probably not enough to motivate the blocking action, but taken together they are. Still, doesn't it feel a little foolish that broadcasters would differentiate between a computer screen and a TV screen like this? For Google, it's more evidence that nothing comes easy when trying to work with Hollywood. I'm trying to find out more about what's happening behind the scenes.

TWC Lines Up For ESPN Online Kick

An important milestone for TV Everywhere may come as early as next Monday, as #2 cable operator Time Warner is planning to make ESPN viewing available online to paying subscribers. Remote access is part of the recent and larger retransmission consent deal between Disney and TWC. TV Everywhere initiatives have been slow to roll out, amid cable programmers' reluctance. Further proving that remote authenticated access works and that it's attractive with a big name like ESPN would increase TV Everywhere's momentum.

Hulu Plus, Take Two: How's $4.95 a Month?

Rumors are swirling that Hulu may cut the price of its nascent Hulu Plus subscription service in half, to $4.95/mo. That would be a tacit recognition of Hulu Plus's minimal value proposition, largely due to its skimpy content offering. As I initially reported in August, over 88% of Hulu Plus content is available for free on Hulu.com. More important, Netflix's streaming gains have really marginalized Hulu Plus. Netflix's far greater resources and subscriber base have enabled it to spend far bigger on content acquisition. Even at $4.95, I continue to see Hulu Plus as an underwhelming proposition in an increasingly noisy landscape.

Viacom Hires Superstar Lawyer to Handle YouTube Appeal

Viacom is showing no signs of giving up on its years-long copyright infringement litigation against Google and YouTube. This week the company retained Theodore Olson, a high-profile appellate and Supreme Court specialist to handle its appeal. While most of the world has moved on and is trying to figure out how to benefit from YouTube's massive scale, Viacom charges on in court.

Verizon to sell Galaxy Tab starting November 11th for $599.99

Verizon is determined to play its part in the tablet computer craze, this week announcing with Samsung that it will sell the latter's new "Tab" tablet for $600 beginning on November 11th. The move follows last week's announcement by Verizon that it will begin selling the iPad on Oct. 28th, which was widely interpreted as the first step toward Verizon offering the iPhone early next year. Apple currently owns the tablet market, and it remains to be seen whether newcomers like the Tab can break through. For his part, Apple CEO Steve Jobs said on Apple's earnings call this week that all other tablets are "dead on arrival." Note, if you want to see the "Tab" and learn more about how connected and mobile devices are transforming the video landscape, come to the VideoSchmooze breakfast at the Samsung Experience on Wed., Dec. 1st.

One-Third of US Adults Skip Live TV: Report

A fascinating new study from Say Media (the entity formed from the recent merger of VideoEgg and Six Apart), suggesting that 56 million, or one-third of adult Internet users, have reduced their live TV viewership. The research identified 2 categories: "Opt Outs" (22 million) who don't own a TV or haven't watched TV in the last week and stream more than 4 hours/week, and "On Demanders" (34 million) who also stream more than 4 hours/week and report watching less live TV than they did a year ago. Not surprisingly, relative to Internet users as a whole, both Opt Outs and On Demanders skew younger and higher educated, though only the latter had higher income than the average Internet user. This type of research is important because the size of both the ad-supported and paid markets for live, first-run TV is far larger than catalog viewing. To the extent its appeal is diminishing as this study suggests poses big problems for everyone in the video ecosystem.

Categories: Aggregators, Broadcasters, Cable Networks, Cable TV Operators, Devices, Mobile Video, Telcos

Topics: ABC, Apple, CBS, ESPN, Google TV, Hulu Plus, iPad, NBC, Samsung, Say, Time Warner Cable, TV Everywhere, Verizon, Viacom, YouTube

-

Cable's Original Programs Should Be A Bulwark Against Cord-Cutting

A WSJ article today, "TV's Alternate Universe," about the proliferation and inventiveness of basic cable programs, provides an unintentional reminder of the value these shows have as a bulwark against cord-cutting. The article points out that basic networks will spend $23 billion this year on 1,462 originals, up from $14 billion on 863 shows just 5 years ago. The fact that these shows are both finding an audience and that they are virtually unavailable for free online makes them highly strategic assets as the pay-TV industry is increasingly buffeted by over-the-top video competition.

Two years ago, in "Cutting the Cord on Cable: For Most of Us It's Not Happening Any Time Soon," I argued that there are 2 key reasons mass-scale cord-cutting was unlikely, at least in the short term: first, the difficulty of watching online-delivered video on TVs (instead of on computers) limited its appeal as a substitute for pay-TV service for mainstream consumers, and second, the loss of numerous popular cable entertainment programs resulting from cord-cutting would give many people pause.

Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

Topics: AMC, FX, Lifetime, Spike TV, TNT, TV Land, USA

-

AT&T's "U-verse Mobile" App Gives Windows Phone 7 Users OTT Video Access

In the midst of all the Microsoft Windows Phone 7 launch hoopla today, AT&T announced a new offering with potentially significant implications: AT&T Wireless-Windows Phone 7 users will get access to a "U-verse Mobile" app that will allow them to download and watch TV shows on their Windows 7 device for a $9.95 monthly subscription. The twist is that it's not necessary to be a U-verse TV subscriber to be a U-verse mobile subscriber.

that will allow them to download and watch TV shows on their Windows 7 device for a $9.95 monthly subscription. The twist is that it's not necessary to be a U-verse TV subscriber to be a U-verse mobile subscriber.

By unbundling mobile access from its TV subscriptions, AT&T is in effect using wireless delivery to go over-the-top (OTT) of incumbent pay-TV operators in their incumbent territories. As a result AT&T is bringing new wireless-based competition and expanding the reach of its video service way beyond the limited geographies where its U-verse TV service is offered today.

Categories: Mobile Video, Telcos

-

Sezmi Expands to Malaysia With YTL Partnership - Template For 4G Carrier Deals in U.S.?

Sezmi is expanding into Malaysia, partnering with YTL Communications to provide the digital television service component of YTL's hybrid broadcast-wireless 4G "quadruple play" that also includes voice and data services. For Sezmi, the move is its first significant international deal, and could serve as a template for partnership deals in other developing countries that don't have or can't affordably build extensive wired broadband networks.

Importantly, the YTL deal also provides a possible glimpse of Sezmi's value as a partner to domestic U.S. carriers rolling out 4G service who might seek to offer a competitive over the top TV service. 4G is gaining momentum in the U.S. Just last week Verizon announced that it would introduce its 4G "LTE" service in 38 markets around the U.S. by the end of the year, with data speeds of 5-12 megabits per second. Both Clearwire and Sprint have already rolled out 4G services to over 50 market each and T-Mobile is in over 60 (albeit none of these always have 100% market coverage just yet). AT&T is planning to launch an extensive 4G network by mid-2011.

offer a competitive over the top TV service. 4G is gaining momentum in the U.S. Just last week Verizon announced that it would introduce its 4G "LTE" service in 38 markets around the U.S. by the end of the year, with data speeds of 5-12 megabits per second. Both Clearwire and Sprint have already rolled out 4G services to over 50 market each and T-Mobile is in over 60 (albeit none of these always have 100% market coverage just yet). AT&T is planning to launch an extensive 4G network by mid-2011.

Categories: Broadband ISPs, International, Telcos

Topics: AT&T, Clearwire, SezMi, Sprint, T-Mobile, Verizon, YTL

-

For Pay-TV Operators, Will TV Everywhere Be TV Nowhere?

I continue to be confounded by the fact that the pay-TV industry - both operators and cable TV networks - have not made more progress on TV Everywhere, their most important competitive initiative in the online era. Yesterday I got yet another dose of this sobering reality watching a panel discussion at ScreenPlays magazine's Media Innovations Summit in LA. The panel included Synacor's Ted May, Starz's John Penney, EPIX's Emil Rensing, thePlatform's Marty Roberts and AT&T's Dan York and was moderated by Marketing/PR executive Bob Gold.

It's not that industry executives can't articulate the value to both operators and networks. For pay-TV operators, it's providing increased value to paying subscribers, which helps both acquisition and retention efforts. For cable networks, its expanded audience reach and advertising, while maintaining their hybrid model of paid distribution and advertising. For both it's staying competitive by providing access to premium content for consumers when, how and where they want it.

Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

Topics: AT&T, EPIX, Starz, Synacor, thePlatform

-

Time Warner's "Premium Video-on-Demand" Experiment is a Blind Alley

Talk about an initiative that flies in the face of all prevailing sentiment: Time Warner is moving forward on testing a new window for early-release movies on VOD priced at $20-30 apiece in 2011, according to comments its CFO John Martin made yesterday at the Goldman Sachs conference. Never mind the wrath the idea will stir up among movie theater owners whose traditional windows get cannibalized as a consequence (Disney learned about that with its "Alice in Wonderland" early DVD release experiment last February), the real issue is that pay-TV operators should deem the idea a non-starter.

wrath the idea will stir up among movie theater owners whose traditional windows get cannibalized as a consequence (Disney learned about that with its "Alice in Wonderland" early DVD release experiment last February), the real issue is that pay-TV operators should deem the idea a non-starter.

Typical VOD rental rates of $4-5 already look expensive to consumers compared to Netflix's $9 all-you-can-eat monthly plans and Redbox's $1 DVD rentals. And while there are scenarios where getting a group or family together to watch a movie makes sense, it's getting harder than ever to do so. The reality is that families are atomizing to their individual activities; perusing or playing on Facebook, watching YouTube/Hulu/Netflix/etc., playing with the Wii or Farmville, chatting on Skype, shopping on Amazon, etc. Corralling this crowd and getting them to agree on any one movie is already a challenge; the prospect of paying $20-30 for the pleasure just sets the bar that much higher.

Categories: Cable TV Operators, FIlms, Satellite, Studios, Telcos

Topics: Disney, Netflix, Redbox, Time Warner, Time Warner Cable

-

New Net Neutrality Ad Campaign Draws in Google's Co-Founders

When it comes to net neutrality, I've learned to expect the unexpected, as any sense of a formal process was long-ago abandoned in favor of an ad hoc free-for-all by interested parties. That was epitomized by the recent partnership between Google and Verizon which joined up to go rogue by proposing their own net neutrality recommendations in August. Though they thought they were moving the ball forward on the issue, they were promptly scorched by net neutrality advocates for endorsing vague private Internet lanes and exempting wireless from any new regulations.

Now the latest chapter in the net neutrality battle is unfolding with an online ad campaign, featuring an online petition directed to Google's co-founders Sergey Brin and Larry Page, to live up to Google's corporate motto "don't be evil" by walking away from the Verizon deal. The campaign is funded by the Progressive Change Campaign Committee and other advocacy groups like MoveOn and Free Press. The petition's web site states that over 334,000 people have signed on so far. Ironically the ads are being bought through Google itself, and on Facebook.

Sergey Brin and Larry Page, to live up to Google's corporate motto "don't be evil" by walking away from the Verizon deal. The campaign is funded by the Progressive Change Campaign Committee and other advocacy groups like MoveOn and Free Press. The petition's web site states that over 334,000 people have signed on so far. Ironically the ads are being bought through Google itself, and on Facebook.

Categories: Broadband ISPs, Regulation, Telcos

-

Are Pay-TV Providers Getting Hit By a Perfect Storm in Q3?

The U.S. pay-TV industry, which as a whole lost multichannel video subscribers for the first time in Q2 '10, may be heading for a soft 3rd quarter as well. As Multichannel News reported yesterday, Time Warner Cable's CFO Rob Marcus said at a conference this week that Q3 "video net losses are pacing ahead" of where they were in Q3 '09. He attributed the downturn to recession-related factors of high unemployment, high home vacancy rates and slow new home formation. Though that's a fair explanation, it's only one element in a perfect storm pay-TV operators now find themselves battling.

Aside from the above recession-related matters, pay-TV operators are also up against belt-tightening that's rooted in basic household economics. As Craig Moffett at Sanford Bernstein pointed out in a note last weekend, in the past 25 years, cable and satellite spending has increased from 1/2 of 1% of discretionary spending to 1.4%, a growth rate that's triple other household discretionary line items.

Categories: Cable TV Operators, Satellite, Telcos

Topics: Sanford Bernstein, Time Warner Cable

-

Pay-TV Industry Loses Subscribers in Q2 '10 For First Time Ever; Cable Bears Brunt

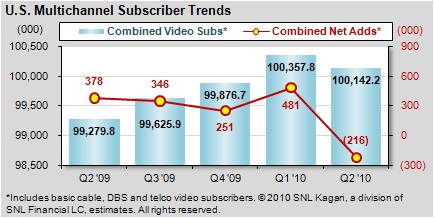

Research firm SNL Kagan is reporting today that the U.S. pay-TV industry (cable/satellite/telco) lost 216,000 multichannel TV subscribers in Q2 '10, the first time the industry as a whole has lost subscribers. Cable operators bore the brunt of the losses, dropping 711,000 subscribers, with Kagan saying 6 of the 8 operators reporting suffered record quarterly losses. By contrast, telcos added 414,000 subs in the quarter and satellite providers gained 81,000. The losses leave cable's industry share at 61%, down from 63.6% a year ago.

Kagan analyst Mariam Rondeli ascribed the quarterly losses to low housing formation and high unemployment due to the ongoing recession, coupled with churn due to promotions from last year's broadcast digital transitions expiring. Rondeli pointed out that over-the-top video alternatives were not the cause. By comparison, the pay-TV gained 378,000 subscribers in Q2 '09, meaning there was a swing of 594,000 subscribers year-over-year. U.S. Pay-TV providers as a whole ended Q2 '10 with 100.1 million subscribers.

Looking ahead, I've heard some murmurs that Q3 '10 could be softer than in prior years, again partially due to the recession, but also because seasonal college students' subscriptions may be reduced due to over-the-top alternatives. While we've yet to see any tangible evidence of cord-cutting, the first impact may simply be slower multichannel sign-ups from younger users more accustomed to watching online. We'll see.

What do you think? Post a comment now (no sign-in required).Categories: Cable TV Operators, Satellite, Telcos

Topics: SNL Kagan

-

TV Everywhere On Track for 30-50 Million Homes By End of 2010: Turner Exec

TV Everywhere services will be available to 30-50 million U.S. homes by the end of this year, according to Jeremy Legg, SVP of Business Development and Multi-Platform Distribution at Turner Broadcasting whom I spoke to last week. Jeremy characterized the 30 million number as "realistic" and 50 million as "plausible." Turner is part of Time Warner, which has been the most significant proponent among content providers of TV Everywhere services; Jeremy is the point person at Turner for its efforts.

I've thought TV Everywhere was a smart concept since it was unveiled last summer, in a high-profile news conference with Time Warner's CEO Jeff Bewkes and Comcast's CEO Brian Roberts. Since then though, pay-TV distributors in the U.S. have been relatively quiet about their TV Everywhere rollout milestones, leading me to grow skeptical about whether they're putting enough muscle behind their efforts. As I argued recently, the stakes for TV Everywhere success have grown considerably as Netflix in particular has ramped up its online offerings, getting closer and closer to pay-TV players' traditional turf.

Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

-

Netflix-Epix Deal Ratchets Up Importance of TV Everywhere

Today's Netflix-Epix deal should be setting off alarms in the CEO suites of major cable operators around the country that TV Everywhere must get rolled out ASAP. The Epix deal underscores the extent of Netflix's financial resources and its ambition to gain a bigger chunk both of consumers' entertainment mindshare and their spending.

The first, a shift in mindshare, is already underway. With 15 million subscribers, an expanding streaming library, countless ways to view (e.g. iPad, Xbox, Roku, Blu-ray, etc, etc), a value-packed $9/mo entry tier and a customer-focused brand, Netflix has established a reputation for itself as the cutting edge video leader. In social settings these days, it is practically inevitable that someone will bring up how they're streaming Netflix content to the device of their choosing and how cool it is. Conversely, despite the cable industry's numerous positive digital TV efforts, it is still dogged by lagging customer service, often confusing pricing tiers and suboptimal user experiences.

Categories: Aggregators, Cable TV Operators, Telcos

Topics: Comcast, EPIX, Netflix, Time Warner Cable

Posts for 'Telcos'

Connect with VideoNuze

Exclusive News Roundup

- Netflix Sees Potential For Video Podcasts, More Creator Content on Platform The Hollywood Reporter

- Netflix Q1 Results Top Expectations as Streamer Stops Reporting Subscriber Counts Variety

- Samsung TV Plus Says It Is Now The Top FAST Platform, With 700 Channels Streaming In U.S. Deadline

- Patreon tests a native live video feature where creators can stream 24/7 TechCrunch

- Tariff Confusion Leaves Advertisers ‘Paralyzed’ and ‘Somber’ NY Times

- Hollywood Is Cranking Out Original Movies. Audiences Aren’t Showing Up. WSJ