-

NDS Leads $20 Million Investment in BlackArrow for Advanced Advertising

Amid all the coverage that online video advertising receives, it's also important to remember that advanced advertising in on-demand and pre-recorded TV continues to evolve. News today that NDS, one of the largest technology providers to multichannel video programming distributors ("MVPDs") is leading a $20 million Series C round in BlackArrow, a provider of advanced advertising solutions, is a reminder of progress. Last week I spoke to Todd Narwid, VP of New Media for NDS and Dean Denhart, BlackArrow's CEO, to learn more about the deal.

("MVPDs") is leading a $20 million Series C round in BlackArrow, a provider of advanced advertising solutions, is a reminder of progress. Last week I spoke to Todd Narwid, VP of New Media for NDS and Dean Denhart, BlackArrow's CEO, to learn more about the deal.

To put the deal and its upside in context, it's important to first understand there's a big difference between how online video advertising against free streams in the open Internet works vs. how advertising against VOD and DVR programs in paid, subscription-based services run by MVPDs works. In the Internet world, there are pretty well-established standards, allowing significant interoperability among sites and ad servers. While measurement challenges persist, the act of getting video ads inserted where they're supposed to be is now pretty straightforward.

Conversely, in the MVPD world, the first challenge is just getting ad serving systems approved and deployed. Because ads are served from within the MVPD's own infrastructure, new ad servers must be tested and integrated with existing video delivery infrastructure residing in distribution centers often called "headends" in the cable world. Unlike MVPDs' broadband deployments, much of MVPDs' TV delivery architecture pre-dates the Internet and therefore is heterogeneous and often difficult to integrate with. In addition, there are the tens of millions of deployed set-top boxes which also differ in their capabilities and openness. MVPDs have made significant progress in creating their own standards and in deploying advanced services, but as anyone who's ever tried to implement any kind of advanced service in the MVPD world can attest, it's hard work and has ground down many promising technology start-ups.

When I first wrote about BlackArrow, on its launch in Oct, '07, I liked its vision of delivering advanced advertising in VOD and DVR programs, but I noted the above challenges gave it a steep hill to climb. Since then, BlackArrow has made progress, deploying with Comcast in Jacksonville, FL and with other operators (though Dean isn't able to mention them due to MVPD restrictions). Still, MVPDs have so many priorities and their resources for testing and integrating new technology are limited. Further, there's a lingering sentiment that MVPDs have only made a half-hearted attempt to really monetize VOD and DVR.

Given these circumstance, the NDS deal appears to offer BlackArrow a lot of upside. As one of the largest technology providers to MVPDs globally ("conditional access" systems that provide secure MVPD video delivery are its main product line, among others), NDS immediately gives BlackArrow both credibility and significantly improved sales and support reach, particularly outside North America. The companies also announced a joint solution offering, which will be key to realizing actual sales Importantly, NDS gives BlackArrow improved financial footing for what promises to be a very long-term process of deploying advanced advertising by MVPDs. Conversely, for NDS, as Todd explained, BlackArrow provides the monetization piece of the puzzle that MVPDs need to create business cases to help them justify NDS's advanced technology delivery systems.

upside. As one of the largest technology providers to MVPDs globally ("conditional access" systems that provide secure MVPD video delivery are its main product line, among others), NDS immediately gives BlackArrow both credibility and significantly improved sales and support reach, particularly outside North America. The companies also announced a joint solution offering, which will be key to realizing actual sales Importantly, NDS gives BlackArrow improved financial footing for what promises to be a very long-term process of deploying advanced advertising by MVPDs. Conversely, for NDS, as Todd explained, BlackArrow provides the monetization piece of the puzzle that MVPDs need to create business cases to help them justify NDS's advanced technology delivery systems.

For MVPDs, who are witnessing the rapid adoption of online video and the threat of cord-cutting down the road, it is essential to be able to offer subscribers more flexible viewing options like VOD and DVR and to give their content partners opportunities to effectively monetize these views. This has been the Achilles heel of VOD and DVR to date, and the scarcity of ad-supported programs in VOD (particularly relative to what's available online) is a direct reflection of this.

Going forward, the challenge for MVPDs will only intensify as content providers face escalating choices about where to optimally monetize their programming. This is where BlackArrow fits in. Plus the company has always had a multi-platform vision, so once it's enabled for TV and DVR, BlackArrow could also provide a pathway to online monetization, which given MVPDs' TV Everywhere initiatives, is also a growing priority.

What do you think? Post a comment now (no sign-in required).

Categories: Advertising, Cable TV Operators, Deals & Financings, DVR, Satellite, Technology, Telcos, Video On Demand

Topics: BlackArrow, Comcast, NDS

-

Hurray - Net Neutrality is Dead, For Now

Yesterday's ruling by the D.C. Court of Appeals that the FCC didn't have the authority to cite Comcast for blocking BitTorrent traffic effectively kills "net neutrality," at least for now. That's a good thing and everyone who's interested in seeing continued innovation by broadband ISPs and new video competitors should be cheering the decision. I've been writing about the FCC's unnecessary net neutrality intrusion into the well-functioning ISP market for several years (here, here, here), and it's very encouraging to see this unanimous court decision.

For those not familiar with net neutrality, it would give the FCC the ability to regulate how broadband ISPs manage their networks in order to ensure that all content is delivered without any bias. Since net neutrality advocates have lacked any sustained pattern of broadband ISP misbehavior to point to as evidence for net neutrality's need, they have instead relied heavily on the argument that pre-emptive regulation is required because ISPs can't be trusted to keep their networks open, and that potential conflicts of interest (many ISPs like Comcast are also big video providers) will inevitably lead ISPs to favor their own services over others.

all content is delivered without any bias. Since net neutrality advocates have lacked any sustained pattern of broadband ISP misbehavior to point to as evidence for net neutrality's need, they have instead relied heavily on the argument that pre-emptive regulation is required because ISPs can't be trusted to keep their networks open, and that potential conflicts of interest (many ISPs like Comcast are also big video providers) will inevitably lead ISPs to favor their own services over others.

Concerns about impending, yet hypothetical ISP "fast lanes and slow lanes" have made great soundbites for net neutrality proponents and politicians. And yes, Comcast bungled how it blocked the BitTorrent traffic, and then how it explained itself. There have also been a handful of other ISP infractions. However, if the 70 million plus broadband households were asked to name a single instance where they felt their ISP degraded their access to a certain web site or video service, I am convinced that very few would be able to think of any.

This reflects the fact that broadband ISPs maintain open networks, rightfully policing against illegal behavior or disproportionate use. The ISP business works quite well, and in most parts of America, substantial competition exists between 2 or more providers (with more wireless ones on the way). Further, new video services and devices, which depend on ever-faster, and open broadband networks continue to proliferate, suggesting ample confidence by their backers that robust network access will be available. Consider: did Steve Jobs hesitate to introduce the iPad, which is heavily video-centric, out of fear for network availability? And how about Netflix, ABC, Discovery, MTV and other video providers who quickly introduced apps for the iPad - did they balk due to network concerns? Of course not.

Earlier this week, I calculated that at least $277.4 million was raised by early stage video companies in Q1 '10, bringing the total to at least $570.2 million over the last 4 quarters, despite the worst market circumstances in ages. As I've said many times, investors and entrepreneurs are undeterred though there are no formal net neutrality rules.

It's also important to remember that broadband networks have been built with private capital, in the process creating tens of thousands of well-paying technical and customer service jobs, plus countless other by the content and applications providers who freely ride these broadband pipes each day. And innovation continues, with numerous announcements of 50 and 100 megabit/second services now available. Tinkering with this vibrant sector of the economy with new regulations introduces the risk of unintended consequences.

Rather than presuming that broadband ISP will disrupt their own success formula by arbitrarily blocking supposed competitors, the FCC would be better off staying relentlessly vigilant of ISP behavior. If ISPs do misbehave - thereby offering clear evidence of the need for regulation - the Congress and the FCC should be prepared to act quickly. Until then net neutrality remains a solution in search of a problem, and Washington has plenty of real problems to work on without tackling imaginary ones.

What do you think? Post a comment now (no sign-in required).

Categories: Broadband ISPs, Regulation

-

Here's How Google TV Will Work - And What It Might Mean

Last week, the NY Times shared some details of "Google TV," the new set-top box Google is developing in partnership with Intel and Sony. The article provided a good outline, and now, based on additional information I've gathered, I'm able to provide new details on the box and also explain what it might mean.

The first and most important thing to know about Google TV is that it is not being positioned to induce users to "cut the cord" on their subscriptions to existing multichannel video programming distributors' ("MVPDs" like cable, satellite or telco) services. Or at least that's Google's initial positioning; whether it's genuine or really just a Trojan Horse game plan is another whole matter. For now anyway, Google is taking a "friend of the industry" approach, telling MVPDs that it's briefing that it is looking to complement their businesses by bringing the full Internet to the TV (this follows the same convergence theme as the new Kylo browser).

existing multichannel video programming distributors' ("MVPDs" like cable, satellite or telco) services. Or at least that's Google's initial positioning; whether it's genuine or really just a Trojan Horse game plan is another whole matter. For now anyway, Google is taking a "friend of the industry" approach, telling MVPDs that it's briefing that it is looking to complement their businesses by bringing the full Internet to the TV (this follows the same convergence theme as the new Kylo browser).

Google is contemplating an entirely novel strategy for its set-top box, seeking to insert it alongside the existing MVPD's set-top box by daisy chaining them together via HDMI connections. In other words, the MVPD's set-top's HDMI output would be connected to the Google TV set-top's HDMI input, and then its HDMI output would be connected to the TV. The authorized TV channels would still be delivered, but Google TV would collect data from the MVPD's set-top and introduce an entirely new UI for users to control their TV experience, to include searching and browsing channels. It would also add a host of new interactive web-type capabilities around the content.

Since the Google TV box would have a full browser and connect to the Internet via the user's WiFi or wired access, it would also bring all of the rest of the Internet to the TV as well, including the full breadth of online video (yes, that would mean one more thing for Hulu to block). My understanding is that on the whole, the Google TV experience is extremely impressive and well conceived. In short, it will get the attention of any MVPD executive who has a look at it and will certainly get them to thinking about how able - or unable - they are to deliver a similar experience themselves to their subscribers.

A key reason that Google is planning to insert its box this way is because it believes that in order to deliver a compelling Internet experience on TV requires a new web-based, and open platform. For Google that of course means Android, which it is vigorously proliferating on smartphones as well. Throw in Google's Chrome browser that it is promoting for online usage and you get a glimpse of how Google's multi-platform strategy comes together. While Sony would be making the box, you have to believe it will have Google branding on it, a first for the company in the living room too.

Categories: Cable TV Operators, Devices, Satellite, Telcos

Topics: Comcast, DISH Network, Google, Google TV, Intel, Sony

-

Google's 1 Gigabit Fiber Experiment is a PR Bonanza

I was deeply skeptical of Google's recently announced 1 gigabit/second fiber-to-the home experiment, but I will concede this: it appears to be influencing the broadband Internet access discussion and is turning into a PR bonanza for the company. Consider 2 of the latest examples: Comcast, America's largest broadband ISP, announced this week that it would make 100 megabit/second speeds available to all customers within 12-18 months and the FCC's new broadband plan set a goal of 100 million U.S. homes having 100 mbps within 10 years and that all schools, hospitals and government building should have 1 gbps access - goals that seem influenced by Google's experiment.

the broadband Internet access discussion and is turning into a PR bonanza for the company. Consider 2 of the latest examples: Comcast, America's largest broadband ISP, announced this week that it would make 100 megabit/second speeds available to all customers within 12-18 months and the FCC's new broadband plan set a goal of 100 million U.S. homes having 100 mbps within 10 years and that all schools, hospitals and government building should have 1 gbps access - goals that seem influenced by Google's experiment.

Meanwhile, as my former colleague and astute industry watcher Bruce Leichtman pointed out to me this week, the press continues to lavish attention on Google's plan, giving it all kinds of free PR. Bloomberg BusinessWeek ran a long article praising the company's fiber plan as providing the impetus to other broadband ISPs to increase their speeds. And my hometown paper the Boston Globe ran a feature this week about the lengths to which towns across Massachusetts are going to be selected as one of the coveted few areas to have Google deploy its network. Though Google hasn't wired a single one of the 71.8 million U.S. homes that subscribed to broadband at the end of '09, you'd think from the goings-on that they were the dominant player driving the market. You gotta love how well the Google PR machine works.

What do you think? Post a comment now (no sign-in required)Categories: Broadband ISPs

-

The Battle Over Movie Rentals is Intensifying

News this morning of a $30 million advertising campaign being launched by 8 Hollywood studios and 8 cable operators promoting "Movies on Demand" is fresh evidence that the battle over movie rentals is intensifying. According to the press release, the 12-week campaign, dubbed "The Video Store Just Moved In" is meant to raise consumer awareness of the convenience and affordability of renting movies on cable.

News this morning of a $30 million advertising campaign being launched by 8 Hollywood studios and 8 cable operators promoting "Movies on Demand" is fresh evidence that the battle over movie rentals is intensifying. According to the press release, the 12-week campaign, dubbed "The Video Store Just Moved In" is meant to raise consumer awareness of the convenience and affordability of renting movies on cable.

Cable Video-on-Demand (VOD) has been around for a long while (in fact 20 years ago my summer internship for Continental Cablevision was studying the ROIs for VOD's precursor, "Pay-per-view"). What's new more recently is the growth of so-called "day-and-date" availability - which means movies are released to VOD at the same time as they become available on DVD. The other recent phenomenon is the widespread adoption of digital set-top boxes and other technologies which makes selection, ordering and delivery easier than ever.

Day-and-date availability is a key competitive differentiator for cable vs. other options, though on the surface it seems somewhat incongruous that studios are on board with this considering their desire to protect DVD sales (this was the key goal of the 28-day "DVD sale" window Netflix and Warner Bros. recently created). Yet Kevin Tsujihara, president of Warner Bros. Home Entertainment Group said that apparently research has shown that simultaneous VOD release doesn't hurt DVD sales. All titles Warner Bros. releases to VOD this year will have day-and-date availability.

The day-and-date advantage is evident at least vs. Netflix for the 9 movies the press release cited as the opening slate being promoted: "Precious," "New Moon," "Ninja Assassin," "Pirate Radio," "Astro Boy," "Bandslam," "Did You Hear About the Morgans," Fantastic Mr. Fox" and "The Fourth Kind." A search on Netflix for the 9 revealed that 5 are listed as "Short wait," 1 becomes available on Mar 20th, 1 on Mar 23rd, and 2 on April 13th (none are available for streaming). However, it's a different story for Amazon - all of the cable VOD movies are currently available for rental from Amazon (except "Mr. Fox") and for purchase. The Amazon rental price is $3.99 for each, whereas the rental price from Comcast (my service provide) is $4.99.

For now anyway, it seems Hollywood studios have decided that cable VOD and online rental firms get day-and-date access, while subscription services like Netflix wait longer (btw Redbox too is being pushed into the "wait longer" category). According to the NY Times article, this is likely because VOD and online rental give studios a 65% share of revenue vs. lower percentages for other outlets.

For consumers, the cable VOD option is likely the most convenient and instantly gratifying. There's no new box to set up or pay for as with Roku, TiVo or another, which would be needed to access Amazon VOD, for example, on TV. For those that haven't bridged broadband to their TV with such a box or a direct connection, on-computer viewing only would be a limitation in the experience. Still, while the day-and-date option is key for those consumers who just have to see a particular title right then, because it's a la carte, it's a far more expensive option than a monthly Netflix subscription, which starts at $8.99/mo. Convenience clearly has its price.

Consumers aren't monolithic though; there isn't one right or wrong model. Each viewing option offers pros and cons and consumers will choose which one, given the particular moment or circumstance, best meets their needs. With the battle for movie rentals escalating, the real winner here looks like the consumer who is being presented more choices than ever.

What do you think? Post a comment now (no sign-in required).

Categories: Cable TV Operators, FIlms, Studios, Video On Demand

Topics: 20th Century Fox, Armstrong, Bend Broadband, Bright House Networks, Comcast, Cox, Focus Featu, Insight, iO TV, Time Warner Cable

-

TiVo's New Boxes are Very Cool But Old Challenges Persist

The two new boxes TiVo unveiled last night - the Premiere and the Premiere XL - go right to the top of my list of most impressive devices that handle both broadcast and broadband content in one seamless experience. The new boxes continue TiVo's pattern of always being one step ahead of the competition in delivering an outstanding user experience. All of that is the good news. The bad news is that unfortunately, nothing I learned in my briefing earlier this week with Jim Denney, TiVo's VP of Product Marketing, suggests that these boxes will find their way into any more than the relatively few homes that prior TiVo boxes have.

First the boxes themselves. The key Premiere innovation is that TiVo now elegantly recognizes broadband sources such as Netflix, Amazon, Blockbuster, YouTube and hundreds of others as bona fide content options, right alongside the customary broadcast and cable channels. That means that when you do a search for a specific TV program or movie, TiVo returns all the viewing options. Say for example it's Saturday night and you search for the classic movie "Raising Arizona." It may be on a cable channel the following Tuesday, but you want to watch it now. Well it is also available from Netflix's Watch Instantly. Assuming you've linked your Netflix account to the Premiere, a couple of clicks of the remote and you're watching right then. That type of all-in-one-box convenience isn't available elsewhere.

The TiVo browse and recommendation experience is tremendously improved also with a new "Discovery bar" - a strip of artwork and images from the programming that adds a lot of zip to the previously text-heavy browsing UI. Selecting an image triggers an expansion window with relevant details (program description, air time, cast, etc.) You can then immerse yourself in a "6 degrees of Kevin Bacon" IMDb-like experience by subsequently selecting an actor, subsequent movies, co-stars, etc, all in a rich, graphical interface. You can also select "Bonus Features" and immediately start reviewing accompanying clips from YouTube.

TiVo is also introducing "Collections," a set of curated categories like "Oscar Winning Films," "Sundance Award Winners" and "AFI's 10 Top 10" which, with accompanying artwork that are another quick, fun new way to browse for what's on (again these collections tap all broadcast and broadband sources). The gorgeous user experience is all built on Flash and is formatted for HD widescreen, to maximize the amount of real estate used. Another first for TiVo is a full QWERTY keyboard that slides out of the remote control for enhanced navigation.

That's a lot of new goodness from TiVo, which as expected comes at a price. The Premiere, with 320 GB of storage (enough for 45 hours of HD recording) is $299 and the Premiere XL, with 1 TB of storage is $499. Best Buy is again highlighted as a key marketing partner. Then of course there's the $13.95/mo TiVo service charge.

These are basically consistent with previous prices, suggesting that yet again TiVo will bump up against the brick wall of most consumers' resistance to buying expensive hardware. No matter how cool TiVo's boxes have been over the years, this is TiVo's traditional Achilles heel and it doesn't seem likely to lessen with the Premiere. When I highlighted this issue Jim allowed that the purpose of the standalone box is to be a "crucible of innovation" and that it is intended mainly for "discerning customers" (my interpretation: TiVo itself doesn't plan to sell a ton of Premiere boxes).

To address the sell-through problem, TiVo has worked hard to develop "TiVo-inside" relationships with video service providers, so that it can become more of a software and services company. For instance, I've been getting my TiVo service as part of my Comcast set-top box for a while now. With the Premiere announcements, TiVo said that RCN, a smallish American "overbuilder" and Virgin Media, a significant U.K. operator would include the Premiere features in their new set-top boxes, which is great.

However, no plans were revealed for what Comcast, by far the largest operator with TiVo inside, will do with the Premiere. In fact, one sticking point for Comcast is almost certainly the very access to broadband content that TiVo is trumpeting with the Premiere. My Comcast box frustratingly disables all of the previous "TiVoCast" broadband features I used to enjoy on my Series 2 box as Comcast seeks to maintain its "walled garden" approach. While RCN may be aggressive about providing access to 3rd-party broadband sources, I'm doubtful that Comcast will be given their own extensive TV Everywhere plans. That raises doubts about whether Comcast's TiVo customers will ever see the Premiere's full range of features.

And so all that brings us back to where TiVo always seems to find itself - with market-leading devices that have serious hurdles to widespread consumer adoption. I really hope there's a forthcoming breakthrough this time around for TiVo. Otherwise history will repeat itself yet again and TiVo will continue to be a well-respected, but relatively marginal player in the digital media landscape.

What do you think? Post a comment now (no sign-in required).

Categories: Cable TV Operators, Devices

Topics: Comcast, RCN, TiVo, Virgin Media

-

Google's Fiber-to-the-Home Experiment Could Cost $750 Million or More

I hope for Google's sake that it understands the cost to build its 1 gigabit/second ultra high-speed fiber network experiment announced today could be $750 million or more. Even for Google that's a very big number, especially considering the company has said it has no intention of actually pursuing this as a business. Of course, we don't know exactly what Google is forecasting its project costs to be, but using Verizon's FiOS numbers wouldn't be a bad starting point to do the math. So here goes.

Google said it would offer the gigabit service to between 50,000 and 500,000 people. Let's start at the high end of that range. Verizon has disclosed that it will spend $18 billion to pass approximately 18 million homes in its footprint with its FiOS fiber-to-the-home network. It's not fair to do a straight average and assume that Verizon is still paying $1,000/home passed given that its costs have no doubt declined over the years.

However, in Google's case, since it has approximately zero experience laying fiber in neighborhoods, and won't get the same level of vendor discounts that Verizon enjoys, it is probably fair to assume Google will spend at least $1,000 per home passed. So if it goes all the way to 500,000 homes, that's $500 million in neighborhood build-out costs. But that's only to wire the neighborhoods, then the service has to be deployed in the homes themselves. That means in-home wiring, on-premise equipment, labor, trucks, insurance, overhead, etc. Estimates for Verizon's per home cost vary, but $500 is in the range often cited. In Verizon's case they're also deploying a set-top box to deliver TV, which Google hasn't announced plans to do (more on that below), so that cost should be deducted. But on the flip side, once again, because Google has never wired a consumer's home (that I'm aware of anyway) it has a steep learning curve ahead of it, meaning its costs could be much higher than Verizon's.

But to make things easy, let's just use the $500 per installed home. So 500,000 homes at $500 apiece, another $250 million for the project. Add it to the $500 million for the neighborhood build-outs and the total is $750 million. This assumes Google decides to go all the way to 500,000. Obviously if it stopped at 50,000, the costs would be a lot lower.

However, there's another big caveat that could drive Google's costs far higher: passing 500,000 homes does not equal having 500,000 customers. It's impossible to predict what percentage of a community's residents would take the Google experimental service. One way of thinking about it is that around 65% of American homes currently subscribe to broadband Internet service. What percentage of those will Google lure? Say it's around 15%. So in a community with 100,000 residents for example, Google may get only get 9,750 people to take its gigabit service (100,000*.65*.15). That means Google may need to pass fiber by 10 homes for every one it gets as a participant in its experiment. Put another way, the $500 million homes passed budget could increase by a factor of 10x. (In case you're wondering, by comparison, Google's 2009 net income was $6.5 billion.) Each subscriber's home would have cost Google approximately $10,750 to connect.

Executives at cable operators and telcos - who build and operate residential networks for a living - are very familiar with modeling network deployment costs. But I wonder, how familiar do you think Google is? Does it know what it has bitten off here? And for what benefit exactly - to test next-generation apps? Hmm. Everyone knows video is the biggest bandwidth hog; an expensive experiment isn't going to change that. And also remember, Google only plans to sell broadband Internet access, not a full bundle with TV or voice. It says it will do this at competitive prices, which means around $50-$100/mo. At these revenue levels and with operating costs that I haven't even mentioned, it's inconceivable to me that there's a positive business case for Google's gigabit experiment.

I'm all for innovation and for pushing competitors along. But Google's experiment really has me scratching my head. No doubt the folks at Verizon, Comcast and other big broadband ISPs are wondering as well. It's one thing for Google to throw $2.5-$3 million at a 52-second Super Bowl ad, but quite another to be contemplating a $750 million experiment with ambiguous goals. What am I missing?

What do you think? Post a comment now (no sign-in required).

Categories: Broadband ISPs, Technology

Topics: Comcast, Google, Verizon

-

It's Official: Netflix Has Entered a "Virtuous Cycle"

Looking at Netflix's Q4 '09 and full year '09 results released late last Wednesday, plus Netflix's performance over the last 3 years, I have concluded the company has officially entered a "virtuous cycle." For those of you not familiar with the term, a virtuous cycle is when a single change or improvement leads to a cascading series of follow-on benefits which both reinforce themselves and add further momentum to the original change (a hyper "one good thing leads to another" scenario, if you will). Virtuous cycles are extremely rare in business, and when they happen they have profound implications.

The start of Netflix's virtuous cycle is obvious: the company's introduction of its free "Watch Instantly" streaming feature in January, 2007. Streaming has fundamentally changed the Netflix service offering and consumers are increasingly aware of this. Traditionally, Netflix subscription plans were defined by limits - 1 DVD out at a time for $8.99/mo, 2-out for $13.99/mo or 3-out for $16.99/mo. But with the company's decision to remove the confusing original caps it placed on streaming consumption and move to an unlimited model, Netflix is now providing enormous new value at the same DVD rental price points. Netflix has also changed how it advertises its services, strongly emphasizing streaming (see its home page for example). The "unlimited streaming" message is breaking through and Netflix subscriber growth momentum over the last 3 years reflects this.

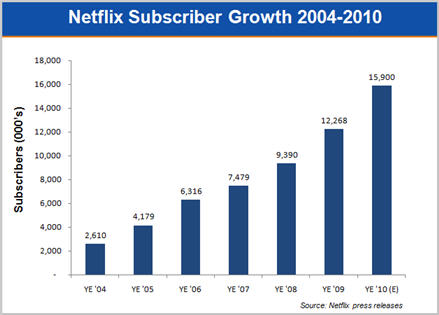

Subscribers grew to 12.3 million at the end of '09, 31% higher than YE '08. To get a sense of Netflix's momentum, '09 growth handily beat '08 (26%) and '07 (18%) growth. The 2.9 million subs added in '09 was 85% above the company's own 2009 beginning year forecast of 1.56 million sub additions. Looking ahead, the mid-point of Netflix's forecast for '10 is for another 30% growth in subs.

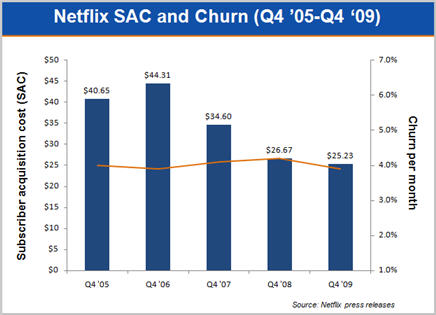

As the streaming benefits have resonated, it's very important to note that subscriber growth is actually getting progressively cheaper for Netflix to accomplish. As the following graph shows, Netflix's subscriber acquisition cost (SAC) has decreased by an impressive 43% from $44.31 in Q4 '06 to $25.23 in Q4 '09 (the 2nd lowest SAC in the company's history). Better still, the quality of these new subs seems high; average monthly churn in Q4 '09 was 3.9%, equal to the lowest churn the company has ever achieved. While Netflix isn't "buying" growth with low-quality additions (an old trick for subscription-oriented businesses), it is however putting more emphasis on the "1-out" service, which, with the addition of unlimited streaming, is an outstanding value for the low-end of the market. Netflix is eager to penetrate this segment, to whom $1 Redbox rentals are very attractive.

While Netflix's financials already reflect the virtuous cycle impact streaming is having on the business, it is likely there is much more to come as streaming takes further hold. Netflix revealed that 48% of its subscribers streamed at least 15 minutes/mo in Q4 '09, up from 41% in Q3 '09 and 26% in Q4 '08 (Incidentally, I think it's conceivable that 80% or more of recently-added subscribers are streaming). But it's just in the last year that Netflix streaming has begun to make the move from computer-only consumption to TV-based consumption, truly making it a mainstream experience. Netflix has inked deals with all the major game consoles (with a Wii marketing campaign beginning in '10), plus numerous CE devices, Blu-ray players, etc. Just ahead is a future where Wi-Fi will be ubiquitous in all new TVs and Netflix's deals with all the major TV manufacturers will ensure it is even more front and center for consumers.

To make streaming attractive, Netflix has had to essentially build a second content library. As I've suggested in the past, this isn't easy, as the company must navigate a thicket of pre-existing Hollywood rights and business relationships. Most notably, Netflix has run into the premium cable networks (HBO, Showtime, Starz and Epix) which have a monopoly on Hollywood's output for their release window. Netflix's deal with Starz was an important first step but still, I've been skeptical that Netflix would land streaming deals with the others.I'm now gaining more confidence that this will indeed happen, especially for these networks' original productions. Netflix is simply getting too big to ignore. It represents a whole new revenue opportunity for premium channels, plus an important loyalty-building outlet. Further out though, while Netflix CEO Reed Hastings says he wants the company to be a distributor for these premium channels, I think it's nearly inevitable that Netflix will compete head-on with them for Hollywood's output. Economics dictate that eventually it makes more sense for Netflix to bid directly for Hollywood rights than work through a premium channel middleman.

In fact, Netflix already has tons of Hollywood relationships, and its recent deal with Warner Bros, creating a 28-day DVD window is emblematic of how Netflix looks at streaming content acquisition going forward. In that superb deal, which was ludicrously criticized by some, Netflix simultaneously helped a critical partner sustain its DVD sales window, while gaining cheaper access to more DVD copies on day 29 and increased streaming rights for catalog titles. As Hastings pointed out on the Q4 earnings call, given the inconsistencies in DVD release strategies, most consumers have little-to-no idea when a title becomes available on DVD, so, while still early, opening up the 28 day window has caused no subscriber complaints. And the company's analysis of subscriber "Queues" indicates, just 27% of requests are for newly-released titles.

Importantly, Netflix's strategy is to pour savings from its DVD deals into streaming content acquisition. As I noted recently, Netflix's detailed subscriber data and usage analysis gives it a huge asymmetric advantage in negotiating additional streaming licenses from Hollywood. Netflix can surgically concentrate its resources on only those titles it knows its subscribers will value. Over time, as DVD sales continue to collapse, Netflix will be there to offer its subs a broader and broader rental selection.

The biggest challenge to Netflix for streaming content acquisition is how much it chooses to spend. Netflix's relatively small size among giants like Comcast and others is what prompted me to suggest over a year ago that Microsoft would acquire Netflix. I'm officially retracting that prediction now, as 2009 demonstrated how much streaming progress Netflix can make on its own. In fact, I think all rumors of a possible Netflix acquisition are off-base; I see the company remaining independent for some time to come.

Netflix is now riding a serious wave and its executives recognize the mile-wide opportunity ahead of it. The product is immeasurably stronger and more appealing with unlimited streaming included. That's in turn leading to impressive sub growth with much-reduced SAC and improving churn. The number of devices bridging Netflix to the TV is growing and portends ubiquity at some point down the road as these devices further leverage Netflix's platinum consumer brand. Streaming content selection is improving, bringing side benefits of reduced DVD postage and inventory costs. With millions of subscribers Netflix now has both the economics and the scale to be a very significant player in the video ecosystem.

Last but not least is a very favorable competitive climate. Aside from a hobbled Blockbuster, astoundingly, Netflix doesn't have any other direct DVD subscription/online streaming hybrid competitor (Amazon and Apple, are you paying attention?). And while Comcast and other multichannel video programming distributors ("MVPDs") are rolling out TV Everywhere services (5 years later than they should have, in my opinion), these are still early stage, and still encumbered by archaic regional limitations. Indeed, Netflix's growth may well cause these companies to consider their own over-the-top plans, as I've suggested.

For years I have been saying that broadband video is the single most disruptive influence on the traditional video distribution value chain. Netflix's success with streaming and the consequences that are yet to play out are resounding evidence of this. Above and beyond YouTube, Hulu, Amazon, Apple and others, Netflix is by far the most important video distributor to watch.

What do you think? Post a comment now (no sign-in required)

Categories: Aggregators, Devices

Topics: Comcast, Netflix, Warner Bros.

-

Brightcove Makes Its First Move Into TV Everywhere

This morning Brightcove is making its first TV Everywhere ("TVE") related announcement, introducing its "TV Everywhere Solution Pack" (TVE-SP), which is the Brightcove 4 enterprise edition augmented with new components and services to support TVE rollouts. It is also unveiling a strategic alliance with Ping Identity to integrate its PingFederate security software with TVE-SP, to enable user authentication and authorization. Lastly, Brightcove has promoted Eric Elia from VP of Professional Services to VP of TV Solutions, charged with leading the company's TVE initiatives. Brightcove's CEO and founder Jeremy Allaire briefed me last week.

To understand how TVE-SP fits in, it is important to quickly review the TVE model. To date, most discussion of TVE has focused on multichannel video programming distributors ("MVPDs") providing their subscribers with online access to TV programming through

their own portals or services, for no extra charge (e.g. Comcast's Fancast Xfinity TV). Receiving less attention so far is that the programmers who agree to participate in MVPD portals will likely require they are also able to offer their same programs on their own sites, which are an increasingly important part of their brand identity and direct-to-consumer focus.

their own portals or services, for no extra charge (e.g. Comcast's Fancast Xfinity TV). Receiving less attention so far is that the programmers who agree to participate in MVPD portals will likely require they are also able to offer their same programs on their own sites, which are an increasingly important part of their brand identity and direct-to-consumer focus. Something else that hasn't received a lot of attention to date is that not all MVPDs will follow Comcast's model of managing, hosting and delivering the online programs themselves. Rather, some MVPDs will prefer to provide just the barebones online navigation, with TV programmers providing an embeddable video player and also delivering all the programming. Less-resourced MVPDs could end of relying heavily on programmers to power their TVE offerings. Where programmers already have online video platforms such as Brightcove in place, these OVPs are in a position to influence how TVE operates. (As a sidenote, I've heard multiple times that Comcast itself is also offering a white labeled version of its FXTV portal to other MVPDs).

All of this means there's likely to be plenty of heterogeneity in TV Everywhere rollouts. Recognizing this, a key part of Brightcove's product strategy is aligning with Ping to use PingFederate and the SAML 2.0 standard for user authentication and authorization. SMAL is used to exchange data between domains (e.g. between a TV programmer, whose web site visitor is trying to access a certain program and an MVPD which holds that user's subscription profile). This type of secure exchange will be essential for TV programmers to offer their own programs on their own sites in a TVE world.

SAML has been widely used in the SaaS business applications and Ping itself lists Comcast, Cox, Bell Canada and Discovery, among others, as customers. However, I suspect these are likely on the enterprise side, not the consumer-facing side. As a result, Brightcove's approach will require significant testing before it will be deemed acceptable by MVPDs. In fact, Brightcove's new white paper indicates that additional standards are required and that some of this is underway at CableLabs, the cable industry's development lab.

It's also worth noting that thePlatform (owned by Comcast) has 4 of the top 5 U.S. cable operators, plus Rogers in Canada, as customers, and ExtendMedia has the major U.S. telcos, plus Bell Canada, as customers. With Brightcove powering video at 60+ TV programmer websites, there are no doubt some interesting dynamics ahead as these OVPs' customers negotiate their TVE relationships and influence the interoperability of their respective technology providers. For its part, thePlatform, which also supports many content providers' video, introduced last November an "Authentication Adaptor" as part of its media publishing system to smooth the authentication and authorization process for programmers offering TVE shows on their own sites.

Confused yet? This is pretty dense stuff, and illustrates some of the hurdles ahead for TVE's widespread rollout. Meanwhile, lurking over TVE's shoulder are the raft of over-the-top alternatives (e.g. Netflix, Boxee, Apple, Xbox, YouTube, etc.) that are sure to gain additional traction with consumers (as a sidenote, yesterday's Best Buy Sunday circular promoted no fewer than 5 Blu-ray players as Netflix compatible, with each showcasing the Netflix logo).

As the TVE story unfolds, Brightcove is sure to be in the middle of the action given its market presence and technical capabilities. But how it all shakes out remains to be seen.

What do you think? Post a comment now (no sign-in required).

(Note - Brightcove, thePlatform and ExtendMedia are VideoNuze sponsors)

Categories: Technology

Topics: Brightcove, Comcast, ExtendMedia, Ping Identity, thePlatform

-

Is Comcast Inching Toward Its Own Over-the-Top Play?

Question: How much difference is there between Comcast offering its TV Everywhere service to its own multichannel video subscribers in its geographical footprint, who have chosen to get their broadband Internet service from another company (e.g. Verizon, AT&T, etc) vs. Comcast offering TV Everywhere services to consumers who similarly get their broadband Internet service from one of these companies (or another cable operator), but happen to also get their multichannel video service from another company (e.g. another cable operator operating in a non-Comcast geographical area)?

If you answered "not that much," then you'll likely have the same reaction that I did upon reading last week's Light Reading article, "Comcast to Expand 'Xfinity' to DSL Subs," which describes Comcast's plan to offer its Fancast Xfinity TV (which I call FXTV) TV Everywhere service to those of its video subscribers who use DSL or some other method to connect to the Internet instead of Comcast's own broadband service by the second or third quarter of 2010.

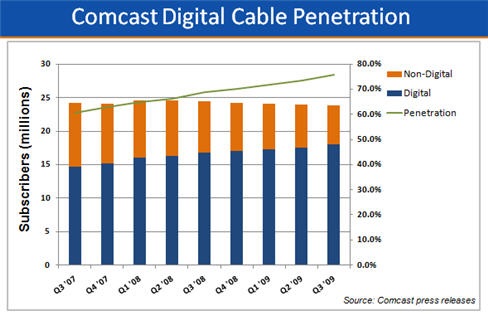

(As quick background, in December, Comcast launched the beta of its FXTV service, but it's only been available to homes that subscribe to both broadband and video, which is about 14 million out of the 24

million who subscribe to Comcast's video service. Of that 10 million difference, using the 70% national broadband penetration rate, I'd estimate there are about 3 million of Comcast's multichannel video subscribers who use Verizon, AT&T or someone else for their broadband access.)

million who subscribe to Comcast's video service. Of that 10 million difference, using the 70% national broadband penetration rate, I'd estimate there are about 3 million of Comcast's multichannel video subscribers who use Verizon, AT&T or someone else for their broadband access.)When I read the article, my reaction was: if Comcast is going to target this group of users, wouldn't the next logical step in FXTV's rollout be to offer it to non-Comcast video subscribers? This is the concept I suggested back in September in, "How TV Everywhere Could Turn Cable Operators and Telcos Into Over-the-Top's Biggest Players." In that post I argued that with sizable revenue per subscriber gains largely behind it, Comcast' big growth opportunity is to expand into other cable operators' territories, by offering FXTV as a TV Everywhere 2.0 over-the-top service in those areas.

To be sure, I noted that this type of move would be a serious breach of protocol in the insular cable industry, and with today's incomplete FXTV offering it wouldn't be viable competitively just yet anyway. But given nationally-oriented competitors like DirecTV, DISH Network and newer OTT alternatives like Netflix mobilizing, it seems logical that somewhere down the road, Comcast, whose geographical reach today only encompasses about 25% of American homes, will have to go national to stay even.

When Comcast's executives have been asked about the possibility of FXTV as an OTT service they have denied any intentions. With their hands full making sure FXTV is working properly for its current subscribers, that's probably the case, at least for now. Plus, with the NBCU deal facing regulatory scrutiny and the net neutrality debate heating up again, Comcast certainly isn't going to hint at anything that would further expand its dominance. But still, given competitive issues, will limiting FXTV access to its own multichannel video subscribers remain the case? It will be interesting to see if and when this changes.

What do you think? Post a comment now (no sign-in required).

Categories: Cable TV Operators

Topics: Comcast, TV Everywhere

-

Goodbye 2009, Hello 2010

It's time to say goodbye to 2009 and begin looking ahead to 2010.

2009 was yet another important year in the ongoing growth of broadband and mobile video. There were many exciting developments, but several stand out for me: the announcement and launches of initial TV Everywhere services, the raising of at least $470 million in new capital by video-oriented companies, YouTube's and Hulu's impressive growth to 10 billion streams/mo and 856 million streams/mo, respectively, the iPhone's impact on popularizing mobile video, the Comcast-NBCU deal, the maturing of the online video advertising model, the proliferation of Roku and other convergence devices and the growth of Netflix's Watch Instantly, just to name a few.

Looking ahead to next year, there are plenty of reasons to be optimistic about video's growth: the rollout of TV Everywhere by multiple providers, the proliferation of Android-powered smartphones and buildout of advanced mobile networks, both of which will contribute to mobile video's growth, the launch of Apple's much-rumored tablet, which could create yet another category of on-the-go content access, the introduction of new convergence devices, helping bridge video to the TV for more people, new made-for-broadband video series, which will help expand the medium's appeal, and wider syndication, which will make video ever more available.

In the midst of all this change, monetization remains the fundamental challenge for broadband and mobile video. More specifically, for both content providers and distributors, the challenge is how to ensure that the video industry avoids the same downward revenue spiral that the Internet itself has wrought on print publishers.

Regardless of all the technology innovations, high-quality content still costs real money to produce. If consumers are going to be offered quality choices, a combination of them paying for it along with advertising, is essential. While it's important to be consumer-friendly, this must always be balanced with a sustainable business model. In short, no matter what the size of the audience is, giving something away for free without a clear path for effectively monetizing it is not a strategy for long-term success.

VideoNuze will be on hiatus until Monday, January 4th (unless of course something big happens during this time). I'll be catching my breath in anticipation of a busy 2010, and hope you will too.

Thank you for finding time in your busy schedules to read and pass along VideoNuze. It's incredibly gratifying to hear from many of you about how important a role VideoNuze plays in helping you understand the disruptive change sweeping through the industry. I hope it will continue to do so in the new year.

A huge thank you also to VideoNuze's sponsors - without them, VideoNuze wouldn't be possible. This year, over 40 companies supported the VideoNuze web site and email, plus the VideoSchmooze evenings and other events. I'm incredibly grateful for their support. As always, if you're interested in sponsoring VideoNuze, please contact me.

Happy holidays to all of you, see you in 2010!

Categories: Advertising, Aggregators, Broadcasters, Cable Networks, Cable TV Operators, Devices, Mobile Video

Topics: Android, Comcast, Hulu, iPhone, NBCU, Netflix, YouTube

-

VideoNuze Report Podcast #44 - December 18, 2009

Daisy Whitney and I are pleased to present the 44th edition of the VideoNuze Report podcast, for December 18, 2009. This will be the last podcast for 2009, and we'd both like to say a huge thanks to everyone who's been listening in this year.

This week I start things off by providing further detail on my experience so far with Comcast's TV Everywhere initiative, Fancast Xfinity TV (or "FXTV" as I call it for short), which was released in beta to 14 million subscribers this week at no additional charge. On the whole I think it's a respectable effort, and in the big picture, is exactly what the company should be doing with online distribution. The main challenge for improving it is getting lots more content from ad-supported and premium cable networks, so that users are more likely to find what they're looking for. For all kinds of reasons, this won't be easy, but if any company can make it happen, it's surely Comcast.

Then Daisy reviews her '09 predictions and shares her "New Media Minute Awards for Excellence." She recognizes Kaltura, 5Min, boxee, Quantcast, and number 1 pick, MyDamnChannel. All have excelled this year, attracting new venture financing, signing new deals and growing their business. Daisy is particularly proud of MyDamnChannel because it also achieved profitability this year. Listen in to find out more.

Click here to listen to the podcast (14 minutes, 18 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Cable Networks, Cable TV Operators, Indie Video, Podcasts

Topics: 5Min, Boxee, Comcast, Kaltura, MyDamnChannel, Quantcast

-

My Review of Fancast Xfinity TV: Respectable Start With Room for Improvement

Amid much anticipation, Comcast launched its "Fancast Xfinity TV" (my shorthand will be "FXTV") service yesterday. FXTV is Comcast's TV Everywhere offering and it will initially be available only to the company's approximately 14 million "dual play" (digital cable + broadband Internet access) subscribers. Comcast is keeping a "beta" label on FXTV for now, to give it some time to work out the kinks. As a Comcast triple-play customer, I have access to FXTV and I played around with it yesterday and last night. While there's plenty of room for improvement, overall FXTV is off to a respectable start.

When dual play customers now visit Fancast they are immediately notified through a prominent pop-up that there's "Great News for Comcast Customers" about online access to over a 1,000 new shows and movies. "Get started" prompts the user to enter their Comcast.net email address and password, then a 17.5MB download begins which includes the Move Networks player and an Adobe Air application. After naming your computer (you're allowed up to 3 devices to access FXTV), the site reloads with the new FXTV Beta branding. All of that worked fine for me.

A prominent window at the top of the page promotes 4 current TV shows, but FXTV misses a big opportunity to immediately demonstrate its value by oddly showcasing just 1 program (TNT's "Men of a Certain Age,") that's not sourced from Hulu. Savvy users will know the rest are already freely available there. Why not promote 4 programs that are only available to FXTV users? And why not include messaging like "Exclusively for FXTV Users!" to remind users of the payoff for having just gone through a download process?

On the positive side, below this window, FXTV promotes programming from premium channels HBO, Starz and Cinemax. As a non-subscriber to Cinemax, when I clicked on "Juno," which had a little key icon, FXTV's authentication process kicked in, prompting a message to subscribe to Cinemax to watch. However, when I clicked "Learn more" my popup blocker interceded which meant I needed to disable it and then reload the page. The Cinemax promotional page that loads is generic from the Comcast.com web site, featuring a graphic of "Gran Torino" and promotions for 3 other movies. Comcast has a golden upsell opportunity when FXTV users click on premium content. It would no doubt improve its conversion ratio if the landing page were customized to load a graphic of the original movie or show selected at FXTV, well merchandised with trailers, clips and other information. A special offer/reward for FXTV users would also help.

Back on the FXTV site, below the premium channel promotions is an area for Full Episodes, categorized by "Celeb News," "The Hot List," "Dramas," etc. Once again, many of the thumbnails link to content that is freely available online and to all other Fancast users. Once again, I'm surprised that Comcast isn't doing more to promote programs that are only available to FXTV users, making it more explicit what's special about FXTV.

I clicked and watched parts of a number of shows and in general my experience was positive. I've read other reviews describing buffering delays, but I didn't experience any issues, or at least anything different than I typically do when starting videos at other sites. One thing Comcast disclosed on the press call yesterday was that FXTV would be available to dual play subscribers outside their homes. Recall that in the 5,000 person trial, users could only access the service from within their homes, so this is a major step forward. I haven't yet tested FXTV remotely, but will do so while in Florida next week.

The biggest challenge FXTV faces is content availability, particularly from the ad-supported cable networks. For example of last week's top 10 rated cable shows, only TNT's "The Closer" and "Men of a Certain Age" are available on FXTV. Among the top 10, there are no sports (football or WWE) or kids shows like "Sponge Bob" (Nick) or "Phineas and Ferb" (Disney) available. Even for #10 show "Keeping up With the Kardashians" the most recent episodes are from Season 2, back in May 2008 - and this is a show that's on E! Entertainment, a channel that Comcast itself owns! There are no episodes offered of my favorite cable show, AMC's "Mad Men."

The content selection on the premium channels HBO, Starz and Cinemax (note Showtime is not yet available on FXTV) is better, but not eye-popping. For example, the only episodes of HBO's "Entourage" that are available are from Season 2 in 2005, despite the fact that Comcast's CEO Brian Roberts specifically demonstrated and highlighted the idea that all episodes of Entourage would be available when he showed the service at the Web 2.0 conference less than 2 months ago. For some reason HBO must have pulled the rights to Entourage in this time.

A lot of the questions on the press call Comcast conducted yesterday focused on content availability and it's clear that obtaining the rights to distribute the full slate of cable programs online is devilishly complex. To be sure, Comcast has made progress, saying it has 27 networks are supplying programming, totaling 12K titles. There's no distributor in a better position to make online distribution happen than Comcast, yet as I wrote last week about Nielsen not yet being able to collect and then synthesize online viewership, Comcast (and other TV Everywhere providers) are subject to forces beyond their control.

Yet another complicating factor is how advertising in FXTV will work. Comcast said that for now, while "nobody really knows what works best," each network will be permitted to experiment with ad loads. It's not clear how long this will go on, nor what role Comcast will play to guide networks to a certain load. In the meantime though, the downside is that the user experience is inconsistent from one network to another. For an offering that's free to subscribers that's not a big drawback, but the lack of consistency does chip away at least a little bit from the overall experience.

Taken together, Comcast deserves credit for getting FXTV out the door just 6 months since announcing it this summer, which is light speed in cable TV terms. There are lots of ways it can and will be improved upon. Gaining credibility with content providers, so that FXTV can beef up its library is priority #1. As I've been saying for a while now, conceptually FXTV is right on all fronts - it preserves the paid consumer model for content providers, offers users enhanced value and helps Comcast and other providers defend against cord-cutting. Hopefully Comcast and other providers will sufficiently invest in these services to let them reach their full potential.

What do you think? Post a comment now.

Categories: Cable Networks, Cable TV Operators

Topics: Comcast, Fancast Xfinity TV, Hulu

-

4 Items Worth Noting for the Nov 30th Week (Alicia Keys on YouTube, Jeff Zucker's record, Comcast's Xfinity, SI's tablet demo)

Following are 4 items worth noting for the Nov 30th week:

1. Alicia Keys concert on YouTube is an underwhelming experience - Did you catch any of the Alicia Keys concert on YouTube this past Tuesday night celebrating World AIDS Day? I watched parts of it, and while the music was great, I have to say it was disappointing from a video quality standpoint -lots of buffering and pixilation, plus watching full screen was impossible.

I think YouTube is on to something special webcasting live concerts. Recall its webcast of the U2 concert from the Rose Bowl on Oct 25th drew a record 10 million viewers. That concert's quality was far superior, and separately, the dramatic staging and 97,000 in-person fans also helped boost the excitement of the online experience. It's still early days, but to really succeed with the concert series, YouTube is going to have to guarantee a minimum quality level. Notwithstanding, American Express, the lead sponsor of the Keys concert had strong visibility and surely YouTube has real interest from other sponsors for future concerts. It could be a very valuable franchise YouTube is building and is further evidence of YouTube's evolution from its UGC roots.

2. Being a Jeff Zucker fan is lonely business - In yesterday's post, "Comcast-NBCU: The Winners, Losers and Unknowns" I said I've been a fan of Jeff Zucker's since seeing him deliver a brutally candid and very sober assessment of the broadcast TV industry at the NATPE conference in Jan '08. My praise elicited a number of incredulous email responses from readers who vehemently disagreed, thinking Zucker's performance merits him being sent to the woodshed rather than to the CEO's office for the new Comcast-NBCU JV.

To be sure, NBC's abysmal performance under Zucker (falling from first place to fourth in prime-time), will be one of his legacies, but I take a broader view of his tenure. A good chunk of NBCU's cable network portfolio came to the company via the Vivendi deal around the time Zucker took over responsibility for cable. Since that time the networks have grown strongly in audience and cash flow has doubled from about $1 billion to a projected $2.2 billion in '09. NBCU added Oxygen (which combined with its iVillage property makes a strong proposition for women-focused advertisers) and The Weather Channel, in a joint buyout with two PE firms.

While Zucker's hiring of Ben Silverman to run NBC was a misstep, NBCU has enjoyed stability on the cable side, with two of the highest-regarded women in TV, Bonnie Hammer and Lauren Zalaznick cranking out hit after hit for their respective networks. A CEO's tenure is always a mixed one, with plenty of wins and losses. It can be hard to know how much of the wins to ascribe to the CEO personally, rather than the executives below, but at the end of the day, NBCU was transformed from a single network company to a cable powerhouse; even Zucker skeptics have to give him some credit for this.

3. Comcast rebrands On Demand Online to Fancast Xfinity TV - yuck! - Largely lost in the NBCU commotion this week was news that B&C broke that Comcast is changing the name of its soon-to-be-launched TV Everywhere service from On Demand Online to Fancast Xfinity TV. Yikes, the branding gurus need to head back to the drawing board, and quick. The name violates the first rule of branding: pronunciation must be obvious and easy. Not only is it unclear how you pronounce Xfinity, it's a an unnecessary mouthful that doesn't fit with any of Comcast's other workmanlike brands (e.g. "Digital Cable," "On Demand," "Comcast.net"). If we're talking about a new videogame targeted to teenage boys, Xfinity is great. If we're talking about a service that provides online access to TV shows, there's no need for something super-edgy. I'd suggest just sticking with "On Demand Online." But even more importantly, priority #1 is getting the product launched successfully.

4. Sports Illustrated demo builds tablet computing buzz - If you haven't seen SI's demo of its tablet version being shown off this week, it's well worth a look at the video here. Never mind that there isn't such a tablet device on the market yet, the rumors swirling around Apple's planned launch of one has created an air of inevitability for the whole category. As the SI demo shows, a tablet can be thought of a larger version of an iPhone (likely minus the phone), providing larger screen real estate to make the user experience even more interesting. It's fascinating to think about what a tablet could do for magazines in particular, along the lines of what the Kindle has done for books. The mobile video and gaming possibilities are endless. Judge for yourselves.

Enjoy the weekend!

Categories: Aggregators, Broadcasters, Cable TV Operators, Magazines, People

Topics: Comcast, NBCU, Sports Illustrated, YouTube

-

VideoNuze Report Podcast #42 - December 4, 2009

Daisy Whitney and I are pleased to present the 42nd edition of the VideoNuze Report podcast, for December 4, 2009.

Today's sole topic is of course the big news of the week, Comcast's acquisition of NBCU. Daisy and I chat about the winners/losers/unknowns that I detailed in my post yesterday. There are a lot of aspects to the Comcast-NBCU deal and the new entity will have wide-ranging implications for the media industry. Listen in to learn more.

Click here to listen to the podcast (15 minutes, 24 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Broadcasters, Cable Networks, Cable TV Operators, Deals & Financings, Podcasts

Topics: Comcast, GE, Hulu, NBCU, Podcast

-

Comcast-NBCU: The Winners, Losers and Unknowns

With Comcast's acquisition of NBCU finally official this morning (technically, it's not an acquisition, but rather the creation of a JV in which Comcast holds 51% and GE 49%, until GE inevitably begins unwinding its position), it's time to assess the winners, losers and unknowns from the deal, the biggest the media industry has seen in a long while. I listened to the Comcast investor call this morning with Brian Roberts, Steve Burke and Michael Angelakis and reviewed their presentation.

Here's how my list shakes out, based on current information:

Winners:

1. Comcast - the biggest winner in the deal is Comcast itself, which has pulled off the second most significant media deal of the decade (the first was its acquisition in 2002 of AT&T Broadband, which made Comcast by far the largest cable operator in the U.S.), for a relatively small amount of upfront cash. Comcast has long sought to become a major player in cable networks, but to date has been able to assemble an interesting, but mostly second tier group of networks (only one, E! has distribution to more than 90 million U.S. homes).

The deal moves Comcast into the elite group of top 5 cable channel owners, alongside Disney, Viacom, Time Warner and News Corp, with pro-forma 2010 annual revenues of $18.2 billion and operating cash flow of $3 billion. It also provides Comcast with a huge hedge on its traditional cable/broadband/voice businesses, as the JV, on a pro-forma basis would be 35% of Comcast's overall 2010 revenue of $52.1 billion, though importantly only 18% of its cash flow of $16.5 billion. On the investor call, Roberts emphasized that the deal should not be seen as the company diminishing its enthusiasm for the traditional cable business, but given the downward recent trends in fundamentals (vividly shown in slides from my "Comcast's Digital Transformation Continues" post 3 weeks ago), the conclusion that Comcast will be relying on its content business for future growth is inescapable.

2. Cable networks' paid business model/TV Everywhere - With Comcast's executives' platitudes about cable networks being "the best part of the media business," the fact that cable networks will contribute 80%+ of the JV's cash flow and the ongoing travails of the ad-supported broadcast TV business, the deal puts an exclamation mark on the primacy of the dual-revenue stream cable network model and Comcast's commitment to defending it (see "The Cable Industry Closes Ranks" for more on this.)

The deal can also be seen as cementing the paid business model for online access to cable networks' programs. Comcast is committed to having online distribution of TV programs emulate the cable model, where access is only given to those consumers who pay for a multichannel subscription service. Much as they may resist acknowledging it, Hollywood and the larger creative community must see Comcast as doing them a huge service by preserving the consumer-paid model, helping the video industry avoid the financial fate of newspapers, broadcasters and music. To be sure, some consumers will cut the cord and be satisfied with what they can get for free online, however it is unlikely to be a large number any time soon. As for aspiring over-the-top providers, they'll need to look outside the cable network ecosystem to generate competitive advantage.

3. Jeff Zucker - The current head of NBCU will migrate into the role of CEO of the JV, greatly expanding his portfolio and influence. Zucker has fought the good fight to preserve the NBC network's status, rotating in new creative heads, shifting Leno to primetime, backing Hulu, etc, but the reality, as he pointed out earlier this year, is that NBCU in his mind has long since become a cable programming company. I've been a Zucker fan since seeing him speak at NATPE in '08 when he laid out a sober assessment of the broadcast business. Through solid acquisitions and execution, Zucker has proved himself to be far more than the wonderboy of "Today" - he's going to fit in well at Comcast and be a great addition to its executive team.

Losers:

1. NBC broadcast network and the JV's 10 owned and operated stations - While Comcast executives said they "don't anticipate any need or desire to divest any businesses" and "take seriously their responsibility" to the iconic NBC brand, the reality is that with the broadcast business contributing just 10% of the JV's pro-forma annual cash flow, the network, and especially the stations, are not just in the back seat of the JV, they're in the third row. Though broadcast contributes 38% of the JV's pro-forma revenue and the deal is being struck near the bottom of the advertising recession, it's hard to see things improving much. Exceptions are the sports division (more on that below), the TV production arm and possibly the news division. The only thing saving the stations is retrans and Comcast's need to appease regulators to get the deal done and keep the regulators at bay thereafter.

2. Other cable operators, telcos and satellite operators - It's never good news when one of your main competitors owns the rights to a good chunk of the key ingredients in your product, yet that's the reality for all other cable operators, telcos and satellite operators. Sure Comcast must be disciplined about throwing its weight around too much, but if these distributors cried when NBCU (and other big network owners) forced bundling and drove fee increases, they haven't seen anything until Comcast runs the renewal processes. With 6 channels having 90+ million homes under agreement plus many others in the JV's portfolio, Comcast is in a very strong negotiating position. As the world moves online, the threat that Comcast eventually says to hell with other distributors and goes over the top itself (a scenario I described here), other distributors have even bigger problems ahead.

3. GE - Yes GE gets about $15 billion in cash and a graceful exit from NBCU, but 20 years since incongruously acquiring NBC, the question burns even brighter, what was GE doing in the entertainment business in the first place? Hasta la vista GE, time to focus on manufacturing turbines and unraveling the woes at GE Capital.

Unknowns:

1. Do content and distribution go together any better this time around - With the disastrous results of AOL-Time Warner still fresh in the mind, it's fair to ask whether vertical integration will work any better this time around. Sensitive to the issue and no doubt anticipating questions on it, Roberts said on the call that this is "a different time and a different deal" and, pointing to News Corp-DirecTV, noted that sometimes vertical integration does work. In addition, he highlighted that the deal's financials are not predicated on achieving any elusive synergies. Still, aside from the obvious benefits of getting bigger in cable networks, the primary reasons cited for Comcast pursuing the deal still have synergy at their core: a slide that clearly says that "Distribution Benefits Content" and "Content Benefits Distribution." As always there are plenty of opportunities to pursue in theory; the challenge is executing on them given the rampant conflicts and turf battles that inevitably ensue.

2. Hulu's future - the online aggregator was literally not mentioned once in the Comcast presentation and its logo only appears on just one of the 36 slides in the deck, yet its presence is hard to underestimate. Hulu is the embodiment of the free, ad-supported premium video model that Comcast is so fiercely committed to combating. So how does it fare when one of its controlling partners soon will be Comcast? In response to a question, Steve Burke said he sees "broadcast content going to Hulu" and that "Hulu and TV Everywhere are complementary products." He also tersely dismissed the much-rumored idea of a Hulu subscription offering. It's impossible to know what becomes of Hulu, but with such divergent interests among the owners, it wouldn't surprise me if Hulu is unwound at some point post closing.

3. ESPN's role - With the JV's NBC Sports assets, plus Comcast's Versus, regional sports networks and Golf Channel, the new JV is primed to play a bigger role in national sports. While Fox Sports and TNT have skirmished for high-profile rights deals with ESPN, the new JV has a much stronger hand to play. It's fair to wonder whether Comcast, which likely sends Disney a check for $70-80 million each month to carry ESPN to its 24 million subscribers, won't at some point say, "hey we can do some of this ourselves" and move to become a bona fide ESPN competitor. In fact, ESPN figures into a far larger Comcast vs. Disney story line in the media industry going forward. The two companies are incredibly dependent on each other, and yet are poised to become even tougher rivals. Expect to hear much more about this one.

4. Consumers - last but not least, what does the deal mean for consumers? Likely very little initially, but over time almost certainly an acceleration of digitally-delivered on-demand premium content - but at a price. Comcast has the best delivery infrastructure, with the JV, soon premier content assets and a persistent, if sometimes incomplete (as with VOD, for example) commitment to shape the digital future. I expect that will mean lots of experimentation with windows, multiplatform distribution and co-promotion across brands. Washington will scrutinize the deal thoroughly, but with continued public service assurances from Comcast, will eventually bless it. Then it will be vigilant for anything that smacks of anti-competitiveness. Consumers should buckle up, the next stage of their media experience is about to begin.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, Cable TV Operators, Deals & Financings

Topics: Comcast, GE, Hulu, NBCU

-

thePlatform Enables TV Everywhere for TV Networks, Lands New Customers

TV Everywhere is getting another shot of momentum this morning as thePlatform, one of the leading online video platform companies (and a subsidiary of Comcast) is rolling out new features aimed at giving TV networks greater control of their programs in the coming TV Everywhere world.

The key new feature is what thePlatform calls an "Authentication Adaptor," which is a mechanism for networks that want to offer their programs on their own web sites to authenticate users as current paying video subscribers of a multichannel video provider (recall that under current TVE plans it is a requirement to be a multichannel video subscriber in order to access programs online). The authentication adaptor works by instantly checking with appropriate multichannel providers' billing systems and returning a yes/no authentication response for that user.

If the user is authenticated, then the adaptor verifies that the specific program is available for viewing to that user, depending on what tier of service the user subscribes to. thePlatform does this by mapping each

individual show to specific channels that each have an ID. The channel IDs are in turn mapped to the multichannel provider's subscription packages. For example if you were to try watching "Entourage" on HBO.com, but you didn't subscribe to HBO the linear channel via your service provider (e.g. Comcast, Time Warner Cable, etc.), your request would be denied. As one can imagine, with the endless permutations of shows, networks, subscription packages and multichannel providers, linking all of this together and delivering fast response times to the user is quite a challenge.

individual show to specific channels that each have an ID. The channel IDs are in turn mapped to the multichannel provider's subscription packages. For example if you were to try watching "Entourage" on HBO.com, but you didn't subscribe to HBO the linear channel via your service provider (e.g. Comcast, Time Warner Cable, etc.), your request would be denied. As one can imagine, with the endless permutations of shows, networks, subscription packages and multichannel providers, linking all of this together and delivering fast response times to the user is quite a challenge. What's also interesting here is that if indeed a request has been denied, a marketing opportunity has been created for both the TV network and the multichannel provider. In the Entourage example above, the denial message could be accompanied by offers to watch now on a pay-per-view basis or to instantly become a subscriber to HBO via Comcast, or to buy the DVD, etc. Or maybe the offer is just to watch free clips to improve sampling. thePlatform supports the creation of these types of rules and integration to appropriate 3rd parties. This is a great example of how TV Everywhere also opens up the instant-gratification online economy to networks and video providers.

The new features gain in importance as thePlatform is also announcing this morning more than 20 TV networks have recently become customers including Fox Sports Networks, E!, G4, Style, Comcast Sports Group (a group of regional sports networks), Travel Channel, Big Ten Network and others yet to be named. As TV Everywhere rolls out next year, TV networks will become increasingly interested in offering their programs themselves, in addition to offering access on their distributors' web sites.