-

AT&T's New "Sponsored Data" Offering Could Make Mobile Video Truly Mobile

Mobile video is one of the hottest trends around. But the reality is that mobile video, is in fact, not very mobile. As I wrote last May, research firm Leichtman Research Group found that of people who watched video on their phone, 63% usually do so at home; for tablets, it's a whopping 89%. One of the big contributing factors to this is the availability of WiFi at home, which allows viewers to avoid using expensive wireless data plans when using their mobile device for video.

That's why a new plan announced yesterday by AT&T, dubbed "Sponsored Data," could have very interesting implications for moving mobile video outside the home, and potentially unleashing totally new mobile video use cases. With Sponsored Data, the content provider pays AT&T for the cost of the data consumed, rather than it counting against the user's monthly data cap. Sponsored Data would have the highest impact on video because it is by far the most data-intensive media format.Topics: AT&T

-

Still No Consensus On Broadband ISP Usage Cap Policies

AT&T made big headlines this week for unveiling a plan to cap monthly usage by its DSL subscribers at 150GB and its U-Verse subscribers at 250GB. Whereas other broadband ISPs like Comcast have long had a 250GB cap in place, what's different about AT&T's plan is that it is proactively saying it will charge $10 for every 50GB users exceed the limit. Other ISPs have tended to use the cap solely as a mechanism for throttling the tiny portion of users who exceed the cap, rather than as a way of generating extra revenue.

Categories: Broadband ISPs

Topics: AT&T, Comcast, FCC, Netflix, Verizon

-

CES Takeaway #2: Don't Count Out the Pay-TV Operators

(Note: Each day this week I'll be writing about one key takeaway from CES 2011.)

If you've been thinking that pay-TV operators were imminent roadkill due to burgeoning "over-the-top" consumption and imminent cord-cutting mania, then important news from CES 2011 should cause you to reassess your assumptions. Instead of new technology undermining pay-TV businesses (which is too often how media characterizes things), the largest operators are starting to show how technology can be used to create compelling new value for their subscribers and enhance their competitiveness even as they relinquish a little control.

At CES, pay-TV announcements focused primarily on 2 areas: extending viewing to tablet computers and eliminating the set-top box by delivering full channel line-ups over broadband to connected TVs. Comcast, the largest U.S. pay-TV operator, made announcements spanning both: live, in-home access on iPads, with on-demand access outside the home, plus Xfinity TV access on certain Samsung connected TVs and on its new Galaxy Tab tablet. Time Warner Cable announced deals with both Samsung and Sony to deliver its line-up to certain connected TVs as well. Dish Network also unveiled its "Remote Access" service for Android tablets, allowing both live and on-demand viewing using the Sling Adapter (it had announced this for iPads in December). Last fall, Dish was also the first pay-TV operator to integrate with Google TV.

Categories: Cable TV Operators, Devices, Satellite, Telcos

Topics: AT&T, Comcast, Netflix, Samsung, Sony, Time Warner Cable, Verizon

-

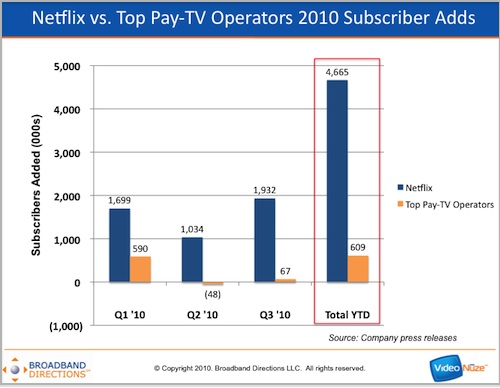

Netflix Has Added 8 Times As Many Subscribers in 2010 As Top Pay-TV Operators, Combined

Here's a pretty amazing factoid to end your week: in 2010 Netflix has added nearly 8 times as many subscribers as 8 of the top 9 pay-TV operators have, combined (#3 cable operator Cox is private and doesn't report). In the first 3 quarters of 2010, Netflix has added nearly 4.7 million subscribers while the top pay-TV operators have gained 609K.

Breaking down the pay-TV industry net gain further, the 2 main telcos (Verizon and AT&T) have added over 1.2 million subscribers and the 2 main satellite providers (DirecTV and DISH) have added 563K, while the top 4 reporting cable operators (Comcast, Time Warner Cable, Charter and Cablevision) have lost over 1.1 million.

Categories: Aggregators, Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

Top U.S. Pay-TV Operators Post Narrow Subscriber Gains in Q3, Rebounding From Q2 Loss

Eight out of the nine largest U.S. pay-TV operators have reported their Q3 '10 results, gaining a slim 66,700 video subscribers, a rebound from a loss of 47,600 subscribers in Q2 '10. The Q2 loss was the first on record for the industry and fueled speculation that "cord-cutting" due to adoption of Internet-delivered video alternatives was rising. With only mildly positive subscriber adds - and 5 of the top 8 operators actually losing subscribers in Q3 - fears that cord-cutting is rising will surely accelerate.

The 8 operators (privately-held Cox Cable, the 3rd-largest cable operator does not disclose its results) represent more than 85% of all U.S. pay-TV households. Though they collectively showed a quarterly gain, if Cox and other cable operators lost subscribers at a comparable rate as the 4 large cable operators in the top 8 (Comcast, Time Warner Cable, Charter and Cablevision), the industry as a whole would have actually lost about 97K subscribers in the 3rd quarter.

Categories: Cable TV Operators, Satellite, Telcos

Topics: AT&T, Cablevision, Charter, Comcast, Cox, DirecTV, DISH, Netflix, Time Warner Cable, Verizon

-

AT&T's "U-verse Mobile" App Gives Windows Phone 7 Users OTT Video Access

In the midst of all the Microsoft Windows Phone 7 launch hoopla today, AT&T announced a new offering with potentially significant implications: AT&T Wireless-Windows Phone 7 users will get access to a "U-verse Mobile" app that will allow them to download and watch TV shows on their Windows 7 device for a $9.95 monthly subscription. The twist is that it's not necessary to be a U-verse TV subscriber to be a U-verse mobile subscriber.

that will allow them to download and watch TV shows on their Windows 7 device for a $9.95 monthly subscription. The twist is that it's not necessary to be a U-verse TV subscriber to be a U-verse mobile subscriber.

By unbundling mobile access from its TV subscriptions, AT&T is in effect using wireless delivery to go over-the-top (OTT) of incumbent pay-TV operators in their incumbent territories. As a result AT&T is bringing new wireless-based competition and expanding the reach of its video service way beyond the limited geographies where its U-verse TV service is offered today.

Categories: Mobile Video, Telcos

-

Sezmi Expands to Malaysia With YTL Partnership - Template For 4G Carrier Deals in U.S.?

Sezmi is expanding into Malaysia, partnering with YTL Communications to provide the digital television service component of YTL's hybrid broadcast-wireless 4G "quadruple play" that also includes voice and data services. For Sezmi, the move is its first significant international deal, and could serve as a template for partnership deals in other developing countries that don't have or can't affordably build extensive wired broadband networks.

Importantly, the YTL deal also provides a possible glimpse of Sezmi's value as a partner to domestic U.S. carriers rolling out 4G service who might seek to offer a competitive over the top TV service. 4G is gaining momentum in the U.S. Just last week Verizon announced that it would introduce its 4G "LTE" service in 38 markets around the U.S. by the end of the year, with data speeds of 5-12 megabits per second. Both Clearwire and Sprint have already rolled out 4G services to over 50 market each and T-Mobile is in over 60 (albeit none of these always have 100% market coverage just yet). AT&T is planning to launch an extensive 4G network by mid-2011.

offer a competitive over the top TV service. 4G is gaining momentum in the U.S. Just last week Verizon announced that it would introduce its 4G "LTE" service in 38 markets around the U.S. by the end of the year, with data speeds of 5-12 megabits per second. Both Clearwire and Sprint have already rolled out 4G services to over 50 market each and T-Mobile is in over 60 (albeit none of these always have 100% market coverage just yet). AT&T is planning to launch an extensive 4G network by mid-2011.

Categories: Broadband ISPs, International, Telcos

Topics: AT&T, Clearwire, SezMi, Sprint, T-Mobile, Verizon, YTL

-

For Pay-TV Operators, Will TV Everywhere Be TV Nowhere?

I continue to be confounded by the fact that the pay-TV industry - both operators and cable TV networks - have not made more progress on TV Everywhere, their most important competitive initiative in the online era. Yesterday I got yet another dose of this sobering reality watching a panel discussion at ScreenPlays magazine's Media Innovations Summit in LA. The panel included Synacor's Ted May, Starz's John Penney, EPIX's Emil Rensing, thePlatform's Marty Roberts and AT&T's Dan York and was moderated by Marketing/PR executive Bob Gold.

It's not that industry executives can't articulate the value to both operators and networks. For pay-TV operators, it's providing increased value to paying subscribers, which helps both acquisition and retention efforts. For cable networks, its expanded audience reach and advertising, while maintaining their hybrid model of paid distribution and advertising. For both it's staying competitive by providing access to premium content for consumers when, how and where they want it.

Categories: Cable Networks, Cable TV Operators, Satellite, Telcos

Topics: AT&T, EPIX, Starz, Synacor, thePlatform

-

Reconciling iPhone 4's Video Push With AT&T's New Data Plans

To nobody's surprise, at Apple's Worldwide Developers Conference yesterday, Steve Jobs announced the new iPhone 4, a powerful machine with a focus on performance. It carries the specs of an iPad including an A4 processor and 800:1 contrast IPS display, along with a new 960x640, 326 pixels per inch "retina display," a pixel density that is indistinguishable to the human eye.

The new iPhone also squarely emphasizes video use - video chat, video shooting and editing and a new Netflix app that Jobs was obviously so excited about that he brought Netflix CEO Reed Hastings up on stage to do his own short demo.

Surprisingly though, the new iPhone's push to more video comes just days after AT&T published its new data plans that seem to disincent video-hungry power users. The new plans, which are slightly cheaper, cap users at 2GB for $25 a month with additional 1GB increments available for $10. While AT&T says that less than 2% of its users exceed the 2GB/mo threshold currently, surely new iPhone (not to mention iPad) users, tempted by all the tasty new video offerings, will start blowing through these limits, knowingly or unknowingly. In fact, it won't take much to exceed the limit; Clicker CEO Jim Lanzone estimated that just 1 HD episode of Mad Men will take up 1.51 GB, or more than 3/4 of the monthly allocation - before you've done anything else.

Categories: Mobile Video

Topics: Apple, AT&T, Flash, iPhone

-

Encoding.com Offers Multi-Bit Rate Support to Meet Spec for iPhones/iPads

This morning Encoding.com is announcing support for multi-bit rate encoding and "stream segmenting," to let its customers comply with Apple's HTTP streaming spec for delivering video in iPhone and iPad apps. Last week, Encoding.com's president Jeff Malkin explained to me that several of its customers had reported that video apps they had submitted to Apple for approval in the App Store had been rejected because they didn't offer multiple bit rates. A post last week on TechCrunch provided more background on Apple's requirements.

Encoding.com now offers its customers 3 pre-set encoding rates with additional ones configurable on demand. Subsequent to encoding and splitting the video into multiple segments, Encoding.com packages up the files and delivers them with XML to the specified CDN for HTTP streaming from standard web servers. The goal of multiple bit rates is to let the video adjust to varying available bandwidth, which in turn helps smooth the user's experience. Jeff reported that CarDomain, the largest auto enthusiast site, is now using Encoding.com's multi-bit rate. CarDomain had seen its app rejected by Apple repeatedly due to "bandwidth usage limitations."

delivers them with XML to the specified CDN for HTTP streaming from standard web servers. The goal of multiple bit rates is to let the video adjust to varying available bandwidth, which in turn helps smooth the user's experience. Jeff reported that CarDomain, the largest auto enthusiast site, is now using Encoding.com's multi-bit rate. CarDomain had seen its app rejected by Apple repeatedly due to "bandwidth usage limitations."

The backdrop here is that with more and more apps incorporating video, when WiFi isn't available, AT&T's 3G network comes under ever-increasing pressure. Just last week I posted on the sub-par experience several iPhone users I've surveyed have been having when trying to access the premium iPhone March Madness app on AT&T's 3G network (though to be fair a few others commented that their access has been ok). I had been surprised that Apple and AT&T felt confident enough in the latter's 3G network to approve this app in the first place, given the likely concurrence of viewing.

AT&T is obviously feeling more confident in its network - or at least in the buffer that Apple is creating by enforcing the multi-bit rate requirement - that more video-intensive apps seem to be passing through the approval process. In addition to the MMOD app, other examples include the new SlingPlayer app, announced last month, and Justin.tv's video app, which was unveiled last week. AT&T is likely trying to be more aggressive with these video apps as news continues to filter out that its iPhone exclusive will expire this year, opening up competition from other carriers.

Mobile video adoption is still well behind online, but the proliferation of mobile devices and apps that support video will no doubt accelerate usage. The next big device catalyst will of course be the iPad, coming this weekend. And as more ecosystem partners like Encoding.com provide the underlying tools to deliver seamless mobile video experiences, even more video-centric apps can be expected.

What do you think? Post a comment now (no sign-in required).Categories: Mobile Video, Technology

Topics: Apple, AT&T, CarDomain, Encoding.com, iPad, iPhone, Justin.tv, MMOD, Sling

-

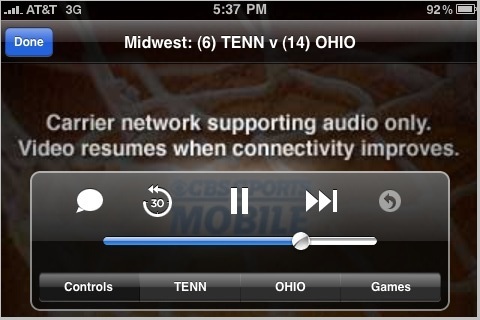

AT&T's 3G Network is Falling Short for Premium MMOD iPhone App

Two weeks ago I noted that the premium "March Madness on Demand" iPhone app, which allows live streaming of all MMOD games would be a big test for AT&T's 3G network, which has been repeatedly criticized for lack of capacity. Based on reports I've received from several friends who have been using the app both on AT&T's 3G network and on WiFi, it appears that AT&T is indeed falling short, with video quality highly inconsistent or video just plain unavailable (see iPhone screen grab below). Granted it's a small sample size, but they've tried it repeatedly and the pattern is pretty clear.

AT&T's network should come under further pressure as the field narrows and audience sizes surge. On a positive note, one friend took note of how incredibly cool it was to be eating lunch at Panera Bread watching live hoops on his iPhone (note, he was on their WiFi at the time). Mobile video is definitely here. On the flip side, I've watched a fair amount of various games online and I have to say I've been somewhat unimpressed by the quality of the streams. Last night's Cornell game (my alma mater) was a perfect example - full screen was highly pixilated and plain unwatchable. Even in standard size there were many stalls and the stream couldn't keep up with camera switches during fast-break coverage.

What have your experiences been like? Post a comment now (no sign-in required).Categories: Mobile Video, Sports

Topics: AT&T, CBS, iPhone, MMOD

-

March Madness on Demand iPhone App Will be Big Test for AT&T's 3G Network

College hoops bragging rights won't be the only thing on the line when the NCAA March Madness men's basketball tournament kicks off next week. Also under the microscope will the performance of AT&T's 3G network, since CBS Mobile announced earlier this week that its new $9.99 premium iPhone app will offer live streaming of all the tournament's games over AT&T's 3G, EDGE and Wi-Fi networks. As with last year there will also be a free "lite" app that will offer on-demand clips only.

Presumably AT&T, CBS and NCAA have modeled how many concurrent streams could be requested under different penetration rates for the app and feel comfortable with AT&T's ability to support these in a quality manner. Let's hope for their sake they got the math right. I continue to hear iPhone users expressing frustration with dropped calls and 3G availability, particularly in Manhattan (in fact I've resisted getting an iPhone for this very reason). AT&T does seem to be getting more confident in its 3G coverage though; just last month it approved Sling's SlingPlayer app for use on its 3G network. In that case, I thought that because few people would likely buy the $29.99 app the stakes weren't that high for AT&T. MMOD is a different story; if AT&T's 3G network fails there will be a horde of angry hoops fans banging on its doors.

feel comfortable with AT&T's ability to support these in a quality manner. Let's hope for their sake they got the math right. I continue to hear iPhone users expressing frustration with dropped calls and 3G availability, particularly in Manhattan (in fact I've resisted getting an iPhone for this very reason). AT&T does seem to be getting more confident in its 3G coverage though; just last month it approved Sling's SlingPlayer app for use on its 3G network. In that case, I thought that because few people would likely buy the $29.99 app the stakes weren't that high for AT&T. MMOD is a different story; if AT&T's 3G network fails there will be a horde of angry hoops fans banging on its doors.

What do you think? Post a comment now (no sign-in required)Categories: Mobile Video, Sports, Telcos

Topics: AT&T, CBS, iPhone, MMOD

-

Apple Approves SlingPlayer Mobile App with 3G; Milestone for Long-Form Mobile Streaming

One other noteworthy tidbit to come out of Mobile World Congress earlier this week was that Sling Media announced it got final approval from Apple to offer its SlingPlayer Mobile App in the App Store. SlingPlayer had been held up due to network concerns, but 2 weeks ago AT&T announced that it would let the SlingPlayer app stream live over its 3G network.

Though there aren't that many Sling users, and only a subset of them will pay the hefty $29.99 price for the SlingPlayer app, its clearance is a milestone because it truly enables high-quality place-shifting of long-form programming to a mobile device. It also steals some thunder from the FLO TV value proposition and offers a

meaningful precedent to others who might like to stream long-form programs to iPhones and other mobile devices down the road (Netflix? Hulu? Amazon?). It's somewhat of a mystery to me how AT&T's overtaxed 3G network can now support long-form video streaming when complaints are still rampant about call quality. I don't have an iPhone or a Sling box, but if a VideoNuze reader does, and downloads the SlingPlayer app, I would be very interested in hearing about your viewing experience.

meaningful precedent to others who might like to stream long-form programs to iPhones and other mobile devices down the road (Netflix? Hulu? Amazon?). It's somewhat of a mystery to me how AT&T's overtaxed 3G network can now support long-form video streaming when complaints are still rampant about call quality. I don't have an iPhone or a Sling box, but if a VideoNuze reader does, and downloads the SlingPlayer app, I would be very interested in hearing about your viewing experience.What do you think? Post a comment now (no sign-in required).

Categories: Devices, Mobile Video

Topics: Apple, AT&T, iPhone, Sling

-

Spotlight is on Video as Mobile World Congress Begins

As the biggest annual mobile conference - the Mobile World Congress - gets underway today in Barcelona, new initiatives from some of the biggest names in technology underscore the growing importance of smartphones and of mobile video specifically. Among the most important headlines:

- Microsoft's CEO Steve Ballmer is unveiling Windows Phone 7 which includes Xbox LIVE games, Zune video and audio, plus enhanced sharing. With Phone 7 Microsoft is continuing to vie for position in a crowded smartphone operating system landscape.

- Sony Ericsson is launching "Creations" allowing users to create and publish video, audio and images from their mobile phones in collaboration with professional developers.

- AT&T and 11 other mobile service providers, which together have about 2 billion subscribers, are introducing a new applications store designed to appeal to developers and compete head-on with Apple's App Store.

- Symbian is taking the wraps off its new Symbian 3 open source release, which includes support for HDMI, so that users can connect their Symbian phones to their TVs and watch 1080p video, in effect creating a Blu-ray player in your pocket.

- Intel and Nokia are merging their respective Moblin and Maemo software platforms to create MeeGo, a unified Linux platform to run across multiple devices.

- Adobe is providing an update that by mid-2010, its AIR runtime for building rich applications will be available for Android and that Flash 10.1 will be generally available for various mobile platforms, including Android. In addition, Adobe is announcing that Omniture, which Adobe recently acquired, will add mobile video measurement within its SiteCatalyst product.

While each announcement, plus countless others, have their own significance in the burgeoning mobile ecosystem, the one that's most relevant to mobile video specifically is the coming availability of Flash 10.1, especially for Android. Mobile video has been hampered to date with the lack of Flash player support on iPhones, so its pending launch on Android phones threatens to scramble the relative appeal of these devices for users eager to watch video from sites like Hulu on their smartphones.

Late last week I got a glimpse of how significant Flash on smartphones is from Jeff Whatcott, SVP of Marketing at Brightcove, which today is announcing an optimized version of its platform for Flash 10.1, to be released in the middle of 2010. Adobe has made the beta of Flash 10.1 available to content providers, and Jeff has a video showing how it works with Brightcove for its customers like NYTimes.com and The Weinstein Company.

Brightcove has done 3 things - optimized its template for mobile devices (so navigation and interactivity is seamless on the small screen), enabled auto-detect of mobile devices (so the correct Brightcove template is served) and leveraged cloud-based transcoding (so a mobile-ready H.264 encoded video is streamed). The goal is for Brightcove's customers to be able to deliver an optimized mobile and Flash experience identical to their online experiences, with minimal additional work flow. Brightcove provides the appropriate logic for mobile templates to its customers which they embed in their pages. When a user visits from a mobile device and clicks to watch video, the right Brightcove-powered experience is delivered.

All of the above activity is happening in the shadow of the now-dominant iPhone (and coming release of the iPad) which do not support Flash. As non-iPhone devices - and content providers - progressively incorporate Flash this year, it seems like the smartphone market is poised for another new turn. Flash is the dominant video player and as users look to replicate their online experiences on their smartphones, the void of Flash on iPhones will become even more pronounced. I don't underestimate Steve Jobs or Apple's ability to compete, but this will be one place where it feels like the iPhone will be at a real disadvantage. Apple is keen to prevent Flash from extending its online hegemony to mobile as well, so it will be interesting to see how it chooses to play this.

What do you think? Post a comment now (no sign-in required).

Categories: Mobile Video, Technology

Topics: Adobe, AT&T, Brightcove, Intel, Microsoft, Nokia, Sony Ericsson, Symbian

-

Scoring My 2009 Predictions

As 2009 winds down, in the spirit of accountability, it's time to take a look back at my 5 predictions for the year and see how they fared. As when I made them, they're listed below in the order of most likely to least likely to pan out.

1. The Syndicated Video Economy Accelerates

My least controversial prediction for 2009 was that video would continue to flow freely among content providers numerous third parties, in what I labeled the "Syndicated Video Economy" back in early 2008. The idea of the SVE is that "destination" sites for online audiences are waning; instead audiences are fragmenting to social networks, mobile devices, micro-blogging sites, etc. As a result, the SVE compels content providers to reach eyeballs wherever they may be, rather than trying to continue driving them to one particular site.

Video syndication continued to gain ground in '09, with a number of the critical building blocks firming up. Participants across the ecosystem such as FreeWheel, 5Min, RAMP, YouTube, Visible Measures, Magnify.net, Grab Networks, blip.TV, Hulu and others were all active in distributing, monetizing and measuring video across the SVE. I heard from many content executives during the year that syndication was now driving their businesses, and that they only expected that to increase in the future. So do I.

2. Mobile Video Takes Off, Finally

When the history of mobile video is written, 2009 will be identified as the year the medium achieved critical mass. I was bullish on mobile video at the end of 2008 primarily due to the iPhone's success and my expectation that other smartphones coming to market would challenge it with ever more innovation. The iPhone has continued its amazing run in '09, on track to sell 20 million+ units. Late in the year the Droid, which Verizon has relentlessly promoted, began making inroads. It also benefitted from Verizon highlighting AT&T's inadequate 3G network. Elsewhere, 4G carrier Clearwire continued its nationwide expansion.

While still behind online video in its development, mobile video is benefiting from comparable characteristics. Handsets are increasingly video capable, just as were computers. Mobile content is flowing freely, leaving the closed "on-deck" only model behind and emulating the open Internet. Carriers are making significant network investments, just as broadband ISPs did. A range of monetization companies have emerged. And so on. As I noted recently, the mobile video ecosystem is healthy and growing. The mobile video story is still in its earliest stages, we'll see much more action in 2010.

3. Net Neutrality Remains Dormant

Given all the problems the Obama administration was inheriting as it prepared to take office a year ago, I predicted that it would not expend energy and political capital trying to restart the net neutrality regulatory process. With broadband ISP misbehavior not factually proven, I also thought Obama's predilection for data in determining government action would prevail. However, I cautioned that politics is a tough business to predict, and so anything can happen.

And indeed, what turned out is that in September, new FCC Chairman Julius Genachowski launched a vigorous net neutrality initiative, despite the fact that there was still little data supporting it. With backwards logic, Genachowski said the FCC would be guided by data it would be collecting, though he was already determined to proceed. In "Why the FCC's Net Neutrality Plan Should Go Nowhere" I argued, among other things, that the FCC is way off the mark, and that in the midst of the gripping recession, to risk the unintended consequences that preemptive regulation carries, was foolhardy. Now, with Comcast set to acquire a controlling interest in NBCU, net neutrality advocates will say there's even more to be worried about. It looks like we can expect action in 2010.

4. Ad-Supported Premium Video Aggregators Shakeout

The well-funded category of ad-supported premium video aggregators was due for a shakeout in '09 and sure enough it happened. Players were challenged by little differentiation, hardly any exclusive content and difficulty attracting audiences. The year's biggest casualty was highflying Joost, which made a last ditch attempt to become a white label video platform before being quietly acquired by Adconion. Veoh, another heavily funded player, cut staff and changed its model. TidalTV barely dipped its toe in the aggregation waters before it became an ad network.

On the positive side, Hulu, YouTube and TV.com continued their growth in '09. Hulu benefited from Disney coming on board as both an investor and content partner, while YouTube improved its appeal to premium content partners and brought on Univision and PBS, among others. Aside from these, Fancast and nichier sites like Dailymotion and Babelgum, there isn't much left to the aggregator category. With TV Everywhere services starting to launch, the opportunity for aggregators to get access to cable programming is less likely than ever. And despite their massive traffic, Hulu and YouTube have significant unresolved business model issues.

5. Microsoft Will Acquire Netflix

This was my long ball prediction for '09, and unless something happens in the waning days of the year, I'll have to concede I got this one wrong. Netflix has remained independent and is charging along with its own streaming "Watch Instantly" feature, now used by over half its subscribers, according to recent research. Netflix has also broadened its penetration of 3rd party devices, adding PS3, Sony Bravia TVs and Blu-ray players, Insignia Blu-ray players this year, in addition to Roku, XBox and others. Netflix is quickly becoming the most sought-after content partner for "over-the-top" device makers.

But as I've previously pointed out, Netflix's number 1 challenge with Watch Instantly is growing its content selection. Though it has a deal with Starz, it is largely boxed out of distributing recent hit movies via Watch Instantly by the premium channels HBO, Showtime and Epix. My rationale for the Microsoft acquisition is that Netflix will need far deeper pockets than it has on its own to crack open the Hollywood-premium channel ecosystem to gain access to prime movies. For its part, Microsoft, locked in a pitched battle with Google and Apple on numerous fronts, could gain advantage with a Netflix deal, positioning it to be the leader in the convergence era. Meanwhile, others like Amazon and YouTube continue to circle this space.

The two big countervailing forces for how premium video gets distributed in the future are TV Everywhere, which seeks to maintain the traditional, closed ecosystem, and the over-the-top consumer device-led approach, which seeks to open it up. It's hard not to see both Netflix and Microsoft playing a major role.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Broadband ISPs, Deals & Financings, Mobile Video, Regulation, Syndicated Video Economy

Topics: Apple, AT&T, Fancast, FCC, Hulu, iPhone, Joost, Microsoft, Netflix, Veoh, Verizon, YouTube

-

Mobile Video Advertising Market Shows Strength

Mobile video advertising is showing strength, benefiting from consumer adoption of the "mobile Internet," strong growth in video-capable smartphones and improving availability of high-quality content for mobile devices.

I gained further insight on the mobile video ad opportunity in a conversation yesterday with Ujjal Kohli, the CEO of Rhythm New Media, a firm focused on mobilizing and monetizing TV programming that has raised

$27 million to date from a group of blue-chip of investors. Later this week Rhythm will formally unveil "RAMP," the Rhythm Advertising Media Platform, a mobile video ad network targeted to brands already advertising on TV who now also want to have a mobile presence.

$27 million to date from a group of blue-chip of investors. Later this week Rhythm will formally unveil "RAMP," the Rhythm Advertising Media Platform, a mobile video ad network targeted to brands already advertising on TV who now also want to have a mobile presence.Ujjal makes a strong case that mobile video is an ideal environment for brand building, and that it addresses many of the challenges that TV advertising itself is facing (clutter, distraction, fragmentation, inadequate frequency/targeting/measurability). Ujjal believes that the nature of mobile video consumption, with its relatively short duration, focused user sessions gives brands a renewed opportunity to engage their target audiences with hard-to-skip messages, not only in the prime-time window, but throughout the day as well.

Rhythm has been helping stoke the market for high-quality mobile video content by building video apps for clients like Discovery, E! Entertainment, TMZ, TV.com, Family Guy and others. App building has been a means to an end for the Rhythm, which is primarily focused developing its mobile video ad network. In Q4 the company has sold and run 20+ campaigns, for brands like MasterCard, Nikon, Toyota, Marriott, Anheuser-Busch and others. These are almost always 15 second spots repurposed from TV campaigns which is no surprise, as the mobile market is not yet big enough to warrant custom creative.

Ujjal explained that a key Rhythm differentiator is that its ads allow interactivity, or the ability for the user to click on an ad's call to action, as is common online. Rhythm has devised a way to incorporate interactivity in ads shown against videos viewed on iPhones, where the use of QuickTime doesn't enable linking. Ujjal said that click-through rates for its "interactive pre-roll" unit fall in the 2%-6% range, while a "full page" ad unit used for mobile photo viewing, (e.g. slide shows on TMZ.com) generate click-throughs up to 11%. Ujjal would not specify what volume of ads Rhythm is serving, except to say it's in the millions/month and that the CPMs are higher than in online video or TV itself.

I've been very bullish on mobile video for some time now, as I believe it is following a similar growth pattern as online video. The macro-trends supporting mobile video's growth are impressive: Nielsen believes that in Q4 '09, 40% of all phones sold will be smartphones and that by 2011 they'll be majority. By then Nielsen forecasts 90 million a month will be watching mobile video. According to its Q3 '09 A2/M2 report, almost 16 million are now watching mobile video/month, up 53% since Q3 '08. They are watching an average of 3 hours, 15 minutes/month. While this is inexplicably down a bit from a year ago, it's worth noting that the heaviest users, to nobody's surprise are age 12-17 (7 hours, 13 minutes) and 18-24 (4 hours, 20 minutes). As these segments age they'll no doubt carry along their mobile video expectations.

Another dynamic sure to have a positive impact on mobile video consumption is the intensifying competitive battle between carriers and between smartphone manufacturers themselves. The recent AT&T-Verizon ad war about their 3G availability is a glimpse of how these companies will use network capacity (key to a positive video experience) as a competitive lever. On the handset side, there is hyper activity: Motorola's Droid is off to a respectable start, a bevy of Google's Android-based smartphones are due in 2010, and, complicating things further, Google plans to release its own "unlocked" (i.e. carrier neutral) Nexus One smartphone next year. While the iPhone opened the smartphone floodgates, many others are now rushing to get a piece of the action.

The biggest uncertainty impacting mobile video's growth is the wireless networks' ability to keep up . All the snazzy smartphones in the world won't matter if users can't get 3G or better access to watch quality video. But, if broadband is any guide, wireless carriers will build out capacity to meet demand, driving up data plan subscriptions and their own ARPU. Broadband also illustrates that as the necessary building blocks fall into place, content providers will be motivated to take part, providing consumers with ever more choices. While it's still early days, taken together it looks as if big things lie ahead for mobile video and for those like Rhythm who can help monetize it.

What do you think? Post a comment now.

Categories: Advertising, Mobile Video

Topics: AT&T, Google, Rhythm New Media, Verizon

-

4 Items Worth Noting for the Dec 7th Week (boxee's box, AT&T's iPhone woes, Nielsen data, 3D is coming)

Following are 4 items worth noting for the Dec 7th week:

1. Boxee's new box with D-Link - It was hard to miss the news from boxee this week that it will be launching its first box, in partnership with D-Link, in early 2010. Boxee has gained a rabid early adopter following, but the high hurdle requirement of downloading and configuring its software onto a 3rd party device meant it was unlikely to gain mainstream appeal. Strategically, the new box is the right move for the company.

For other standalone box makers such as Roku, boxee's box, with its open source ability to easily offer lots of content, is a new challenge (though note, still no Hulu programming and little cable programming will be available on the boxee box). The indicated price point of $200 is on the high side, particularly as broadband-enabled Blu-ray players are already sub-$150 and falling. Roku has set a high standard for out-of-the-box usability whereas D-Link's media adaptors have never been considered ease-of-use standouts. Boxee's snazzy, but very unconventional sunken-cube design for the D-Link box is also risky. While eye-catching, it introduces complexity for users already challenged by how to squeeze another component onto their shelves. If boxee only succeeds in getting its current early adopters to buy the box it will have gained little. This one will be interesting to watch unfold.

2. AT&T tries to solve its iPhone data usage problem - In the "be careful what you ask for, you might just get it" category, AT&T Wireless head Ralph de la Vega revealed an interesting factoid this week at the UBS media conference: 3% of its smartphone (i.e. iPhone) users consume 40% of its network's capacity. Of course video and audio capabilities were one of the big ideas behind the iPhone, so AT&T should hardly be surprised by this result. AT&T, which has been hammered by Verizon (not to mention its users) over network quality, thinks the solution to its problem is giving heavy users unspecified "incentives" to reduce their activity. No word on what that means exactly.

Mobile video has become very hot this year, largely due to the iPhone's success. But the best smartphones in the world can't compensate for lack of network capacity. While AT&T is adding more 3G availability, it's questionable whether they'll ever catch up to user demand. That could mean the only way to manage this problem is to throttle demand through higher data usage pricing. That would be unfortunate and surely stunt the iPhone's video growth. Verizon, with its line of Android-powered phones, could be a key beneficiary.

3. Q3 '09 Nielsen data shows TV's supremacy remains, though early slippage found - Nielsen released its latest A2/M2 Three Screen Report this week, offering yet another reminder that despite online video's incredible growth, TV viewing still reigns supreme. Nielsen found that TV viewing accounted for 129 hours, 16 minutes in Q3. While that amount is more than 40 times greater than the 3 hours, 24 minutes spent on online video viewing, it is actually down a slight .4% from Q3 '08 of 129 hours 45 minutes.

How much weight should we give that drop of 29 minutes a month (which equates to just less than a minute/day)? Not a lot until we see a sustained trend over time. There are plenty of other video options causing competition for consumers' attention, but good old fashioned TV is going to dominate for a long time to come. This is one of the key motivators behind Comcast's acquisition of NBCU.

4. 3D poised for major visibility - In my Oct. 30th "4 Items" post I mentioned being impressed with a demo from 3D TV technology company HDLogix I saw while in Denver for the CTAM Summit. This Sunday the company will do a major public demonstration, broadcasting the Cowboys-Chargers in 3D on the Cowboys Stadium's 160 foot by 72 foot HDTV display. HDLogix touts its ImageIQ 3D as the most cost-effective method for generating 3D video, as it upconverts existing 2D streams in real-time, meaning no additional production costs are incurred.

Obviously those watching from home won't be able to see the 3D streaming, but it will surely be a sight to see the 80,000 attendees sporting their 3D glasses oohing and aahing. Between this and James Cameron's 3D "Avatar" releasing next week, 3D is poised for a lot of exposure.

Enjoy the weekend!

Categories: Devices, Mobile Video, Sports, Technology, Telcos

Topics: AT&T, Boxee, D-Link, HDLogix, iPhone, Nielsen, Roku

-

4 Items Worth Noting from the Week of September 7th

Following are 4 news items worth noting from the week of Sept. 7th:

1. Hulu's boss says it needs to charge for content - Bloomberg ran a story this week quoting Chase Carey, deputy chairman of News Corp (Fox's owner, and therefore a part-owner of Hulu) as saying at a BofA investor conference, "Ad-supported only is going to be a tough place in a fractured world....You want a mix of pay and free."

VideoNuze readers know that while I've admired Hulu's user experience from the start, I've long been critical of its thin ad model, which falls well short of generating revenue/program/viewer parity with traditional on-air program delivery. That lack of parity has caused Hulu's owners to cordon off access to Hulu on TVs for most viewers. But the networks' fear of cannibalizing their own P&Ls only frustrates loyal Hulu users, who neither understand nor care about such legacy concerns. All of this and more led me months ago to conclude a subscription offering is inevitable from Hulu. The impending TV Everywhere launches, which further marginalize ad-only business models, and now Carey's public remarks, solidify my thinking. We'll soon see some type of Hulu subscription tier.

2. Move Networks notches a win with Cable and Wireless deal - Score one for Move Networks, which this week announced Cable and its first tier 1 telco customer. Move enables C&W to deliver an HD, linear multichannel video service, plus on-demand and broadband content to its broadband customers, all through existing DSL connections. Move's repositioning, which I wrote about recently, obviates telcos' need to invest billions in upgrading their networks to get into the IPTV business. Indeed, Roxanne Austin, Move's CEO told me yesterday that C&W has for years considered all the various options for getting into video, but has never pulled the trigger until now. The deal covers up to 7 million homes and interestingly, rather than getting a license fee, Move will be paid a share of subscriber revenue. Roxanne says another big deal will be announced shortly.

3. iPod Nano gets video, battle with Cisco's Flip escalates - As you likely know, Steve Jobs unveiled the new iPod Nano this week, which incorporates an SD video camera. Following the iPhone 3GS adding video recording capability, I think it's pretty clear that Apple has decided video is the next big thing for its devices. As I suggested recently, Apple's embrace is going to drive user-generated video - and YouTube, as the undisputed home for it - to a whole new level.

But one wonders what this all means for Cisco's recently-acquired Flip video camera, and others from Creative, Sony, Kodak, etc? Cisco in particular has a lot on the line since it just shelled out almost $600M for Flip's parent Pure Digital. Granted Apple's devices are still SD, while Flip now emphasizes HD, but still, getting video recording "for free" as Jobs put it at the launch is pretty compelling for consumers. Even if the Flip deal doesn't work out as planned, Cisco will still be selling a whole lot more routers to handle all of this newly-generated broadband video, so it's a winner either way.

4. AT&T Wireless adding 3G capacity - In last Friday's "4 Items" post, I noted a great story the NY Times ran showcasing the frustrations that AT&T Wireless customers are experiencing due to the millions of data-intensive iPhones clogging up the network. AT&T has been hearing complaints from all sides, and this week announced 3G network upgrades in 6 cities this year, with plans to cover 25 of the top 30 U.S. cities by the end of next year, and 90% of its current 3G footprint by the end of 2011. These upgrades can't come soon enough for iPhone users. Meanwhile the company's YouTube video, featuring "Seth the blogger guy" explaining how AT&T is addressing network issues itself came under attack, as AdAge reported. There's no pleasing everyone.

Enjoy the weekend!

Categories: Advertising, Aggregators, International, Mobile Video, Technology, Telcos

Topics: Apple, AT&T, Cable and Wireless, Cisco, Hulu, iPod Nano, Move Networks, News Corp.

-

4 Items Worth Noting from the Week of August 31st

Following are 4 news items worth noting from the week of August 31st:

1. Nielsen "Three Screen Report" shows no TV viewing erosion - I was intrigued by Nielsen's new data out this week that showed no erosion in TV viewership year over year. In Q2 '08 TV usage was 139 hours/mo. In Q2 '09 it actually ticked up a bit to 141 hours 3 minutes/mo. Nielsen shows an almost 50% increase in time spent watching video on the Internet, from 2 hours 12 minutes in Q2 '08 to 3 hours 11 minutes in Q2 '09 (it's worth noting that recently comScore pegged online video usage at a far higher level of 8.3 hours/mo raising the question of how to reconcile the two firms' methodologies).

I find it slightly amazing that we still aren't seeing any drop off in TV viewership. Are people really able to expand their media behavior to accommodate all this? Are they multi-tasking more? Is the data incorrect? Who knows. I for one believe that it's practically inevitable that TV viewership numbers are going to come down at some point. We'll see.

2. DivX acquires AnySource - Though relatively small at about $15M, this week's acquisition by DivX of AnySource Media is important and further proof of the jostling for position underway in the "broadband video-to-the-TV" convergence battle (see this week's "First Intel-Powered Convergence Device Being Unveiled in Europe" for more). I wrote about AnySource earlier this year, noting that its "Internet Video Navigator" looked like a content-friendly approach that would be highly beneficial to CE companies launching Internet-enabled TVs. I'm guessing that DivX will seek to license IVN to CE companies as part of a DivX bundle, moving AnySource away from its current ad-based model. With the IBC show starting late next week, I'm anticipating a number of convergence-oriented announcements.

3. iPhone usage swamps AT&T's wireless network - The NY Times carried a great story this week about the frustration some AT&T subscribers are experiencing these days, as data-centric iPhone usage crushes AT&T's network (video is no doubt the biggest culprit). This was entirely predictable and now AT&T is scrambling to upgrade its network to keep up with demand. But with upgrades not planned to be completed until next year, further pain can be expected. I've been enthusiastic about both live and on-demand video applications on the iPhone (and other smartphones as well), but I'm sobered by the reality that these mobile video apps will be for naught if the underlying networks can't handle them.

4. Another great Netflix streaming experience for me, this time in Quechee VT courtesy of Verizon Wireless - Speaking of taxing the network, I was a prime offender of Verizon's wireless network last weekend. While in Quechee, VT (a pretty remote town about 130 miles from Boston) for a friend's wedding, I tethered my Blackberry during downtime and streamed "The Shawshank Redemption" (the best movie ever made) to my PC using Netflix's Watch Instantly. I'm happy to report that it came through without a single hiccup. Beautiful full-screen video quality, audio and video in synch, and totally responsive fast-forwarding and rewinding. I've been very bullish on Netflix's Watch Instantly, and this experience made me even more so.

Per the AT&T issue above, it's quite possible that occupants of neighboring rooms in the inn who were trying to make calls on their Verizon phones while I was watching weren't able to do so. But hey, that was their problem, not mine!

Enjoy the weekend (especially if you're in the U.S. and have Monday off too)!

Categories: Aggregators, Deals & Financings, Devices, Mobile Video

Topics: AnySource, Apple, AT&T, comScore, DivX, Intel, iPhone, Netflix, Nielsen, Verizon Wireless

-

2009 Prediction #2: Mobile Video Takes Off, Finally

As promised, each day this week I'm sharing one prediction for 2009, with each one getting progressively bolder as the week progresses (and yes, I'll concede - as a number of you privately pointed out to me - yesterday's forecast that the Syndicated Video Economy would grow in '09 was a pretty wimpy start). So moving out a little further on the limb, today's prediction #2 is that video delivered directly to mobile/wireless devices will take off in '09, finally.

For those of you who have been following mobile/wireless video delivery, this has been a market that's perpetually been "just around the corner." In fact, a little over a year ago when I was planning VideoNuze, several people suggested that I shouldn't just focus on broadband delivery (as I define it to mean high-speed wired delivery of video to a home or business), but also mobile/wireless video. But after doing some due diligence I concluded that the market wasn't there yet, and that the vast majority of new video activity would be focused on wired broadband. Indeed, I think that's how '07 and much of '08 have shaped up.

However, having tracked recent activity in the mobile video space, I think '09 is going to be a big year of growth and recognition for this new medium (in fact, an old friend gently chastised me over lunch last week for even drawing a distinction between wired and wireless delivery, saying, "come on, it's ALL broadband!" I think he makes a very fair point.)

What has traditionally held back mobile delivery are a lack of video-capable devices, voice and text-focused wireless networks and a closed "on-deck" paradigm, which is the wireless carrier's version of the cable and satellite industry's proverbial walled-garden.

These limitations have now been mostly addressed, or are in the process of being addressed. On the device side, the most notable video-capable device is of course the iPhone, which by my calculations has already sold over 13 million units and is on its way to almost 20 million by the end of the year. Everyone I know who has an iPhone - especially kids - are infatuated with the video feature (if you've never seen it, especially now using AT&T's 3G network, get thee to an Apple store immediately!). In '09, the iPhone is poised for even greater popularity as Wal-Mart begins stocking it, possibly for just $99. Recession or not, the iPhone is going to remain white hot.

Not to be lost in the iPhone's phenomenal wake are many other new video-capable phones. There's of course the new G1 from T-Mobile, powered by Android, Google's new mobile OS. I got my first look at one last week, and though not as sleek as the iPhone, I was able to watch excellent YouTube video. There are plenty of others to choose from as well, including the Samsung Propel, the LG Incite, the new BlackBerry Storm and the latest mother-of-all-phones, the Nokia N64, which comes with 16GB of internal memory (enough for 40 hours of video). Whereas many of us today carry phones incapable or barely capable of viewing video, in '09 the replacement process will be in full swing.

Of course, all the cool devices in the world don't matter unless you have a robust underlying network and the freedom to view what you want. On this front, the wireless carriers' push to build out their next generation 3G networks finally allows sufficient bandwidth to view high-quality video (though not HD yet). Next up is 4G, first from Clearwire, the SprintNextel-Intel-Google-cable industry consortium that's deploying its WiMax network with speeds of up to 6 Mbps downstream being promised. There's also MediaFLO, Qualcomm's mobile broadcasting platform that has steadily built out an ecosystem of technology, carrier and content partners.

Last but not least are the consumer-focused services and applications. Until recently, this market has mainly consisted of packaged subscription services like Verizon's VCast and MobiTV, which itself recently announced more than 5 million subscribers. The combination of new devices and networks promises to bring an increase in on-demand, web-based, ad-supported video consumption (plus paid downloads to be sure, courtesy of the iPhone mainly). Another interesting twist is the advent of live broadcasting from mobile devices, powered by providers like Qik, Kyte and Mogulus. These all supercharge the Twitter micro-blogging phenomenon.

All of this underscores why the distinction between wired and wireless broadband really becomes meaningless over time. The mobile experience is going to seem more and more like the one you have sitting at your computer, with the added benefit of portability. To throw a blue-sky variable into the mix, one wonders if at some point you'll simply plug your phone into your TV and watch streamed or downloaded video that way, rather than through a set-top box or a wired broadband connection. There's a convergence concept for you!

Years in the making, mobile/wireless video is finally upon us, and '09 is going to be a big year. That's good news for all of us as consumers, and it surely means I'll be working a lot harder to stay on top of things.

What do you think? Post a comment now.

Previous, Prediction #1: Syndicated Video Economy Grows

Tomorrow, 2009 Prediction #3

Categories: Devices, Mobile Video

Topics: Android, Apple, AT&T, BlackBerry, Clearwire, Google, iPhone, LG, Medi, Nokia, Samsung, SprintNextel, T-Mobile, Verizon, Wal-Mart

Posts for 'AT&T'

Connect with VideoNuze

Exclusive News Roundup

- Netflix Sees Potential For Video Podcasts, More Creator Content on Platform The Hollywood Reporter

- Netflix Q1 Results Top Expectations as Streamer Stops Reporting Subscriber Counts Variety

- Samsung TV Plus Says It Is Now The Top FAST Platform, With 700 Channels Streaming In U.S. Deadline

- Patreon tests a native live video feature where creators can stream 24/7 TechCrunch

- Tariff Confusion Leaves Advertisers ‘Paralyzed’ and ‘Somber’ NY Times

- Hollywood Is Cranking Out Original Movies. Audiences Aren’t Showing Up. WSJ