-

4 Items Worth Noting (Hulu, TiVo-Emmys, GAP-VMIX, Long Tail) for Sept 21st Week

Following are 4 news items worth noting from the week of Sept. 21st:

1. Bashing Hulu gains steam - what's going on here? - These days everyone seems to want bash Hulu and its pure ad-supported business model for premium content. Last week it was Soleil Securities releasing a report that Hulu costs its owners $920 per viewer in advertising when they shift their viewership. This week, it was a panel of industry executives turn. Then a leaked email from CBS's Quincy Smith showed his dissatisfaction with Hulu, and interest in trying to prove it is the cause of its parent networks' ratings declines.

What's happening here is that the world is waking up to the fact that although Hulu's user experience is world-class, its ad model implementation is simply too light to be sustainable. I wrote about this a year ago in "Broadcast Networks' Use of Broadband Video is Accelerating Demise of their Business Model," following up in May with "OK, Hulu Now Has ABC. But When Will it Prove Its Business Model?" Content executives are finally realizing that it is still too early to put long form premium quality video online for free. Doing so spoils viewers and reinforces their expectation that the Internet is a free-only medium. When TV Everywhere soon reasserts the superiority of hybrid pay/ad models, ad-only long-form sites are going to get squeezed. At VideoSchmooze on Oct 13th, we have Hulu's first CEO George Kliavkoff on our panel; it's going to be a great opportunity to understand Hulu's model and dig further into this whole issue.

2. TiVo data on ad-skipping for Emmy-winning programs should have TV industry alarmed - As if ad-skipping in general wasn't already a "hair-on-fire" problem for TV executives, research TiVo released this week on ad-skipping behavior specifically for Emmy-winning programs should have the industry on DEFCON 1 alert. Using data from its "Stop | Watch" ratings service, TiVo found that audiences for the winning programs in the 5 top Emmy categories - Outstanding Comedy Series, Drama Series, Animated Program, Reality-Competition and Variety/Music/Comedy Series - all show heavier than average (for their genre) time-shifting. The same pattern is true for ad-skipping; the only exception is "30 Rock" (winner of Outstanding Comedy Series) which performs slightly better than its genre average.

The numbers for AMC's "Mad Men" (winner of Outstanding Drama Series), are particularly eye-opening: 85% of the TiVo research panel's viewers time-shifted, and of those, 83% ad-skipped. (Note as an avid Mad Men viewer, I've been doing both since the show's premiere episode. It's unimaginable to me to watch the show at its appointed time, and with the ads.) The data means that even when TV execs produce a critical winner, their ability to effectively monetize it is under siege. How long will BMW sign up to be Mad Men's premier sponsor with research like this? TiVo's time-shifting data shows why network executives have to get the online ad model right. When TV Everywhere launches it will cater to massive latent interest in on-demand access by viewers; it is essential these views be better monetized than Hulu, for example, is doing today.

3. Radio stations push into online video as GAP Broadcasting launches with VMIX - Lacking its own video, the radio industry has been a little bit of the odd man out in the online video revolution. Some of the industry's bigger players like Clear Channel have jumped in, but there hasn't been a lot of momentum, especially with the ad downturn. But this week GAP Broadcasting, owner of 116 stations in mostly smaller markets announced a partnership with video platform and content provider VMIX. I talked to VMIX CEO Mike Glickenhaus who reported that radio stations are starting to get on board. For GAP, VMIX is providing an online video platform, premium content from hundreds of licensed partners, user-generated video tools and sales training, among other things. GAP's goal is to be a "total audience engagement platform" not just a radio station. Sounds right, but there's lots of hard work ahead.

4. So is there a "Long Tail" or isn't there? Ever since Chris Anderson's book "The Long Tail" appeared in 2006 there have been researchers challenging his theory which asserts that infinite shelf space drives customer demand into the niches. The latest attempt is by 2 Wharton professors, who, using Netflix data, observe that the Long Tail effect is not ironclad. Sometimes it's present, sometimes it's not. Anderson disputes their findings. The argument boils down to the definitions of the "head" and "tail" of the markets being studied. Anderson defines them in absolute terms (say the top 100 products), whereas the Wharton team defines them in terms of percentages (the top 1 %).

I've been fascinated with the Long Tail concept since the beginning, as it potentially represents a continued evolution of video choice; over-the-air broadcasting allowed for 3 channels originally, cable then allowed for 30, 50, 500, now broadband creates infinite shelf space. Independent online video producers and their investors have bet on the Long Tail effect working for them to drive viewership beyond broadcast and cable. With Nielsen reporting hours of TV viewership holding steady, we haven't yet seen cannibalization. However, with Nielsen, comScore and others reporting online video consumption surging, audiences may be carving out time from other activities to go online and watch.

Enjoy your weekends! There will be no VideoNuze on Monday as I'll be observing Yom Kippur.

Categories: Advertising, Aggregators, Broadcasters, Indie Video, Radio

Topics: AMC, GAP Broadcasting, Hulu, Long Tail, Netflix, VMIX

-

4 Items Worth Noting from the Week of September 7th

Following are 4 news items worth noting from the week of Sept. 7th:

1. Hulu's boss says it needs to charge for content - Bloomberg ran a story this week quoting Chase Carey, deputy chairman of News Corp (Fox's owner, and therefore a part-owner of Hulu) as saying at a BofA investor conference, "Ad-supported only is going to be a tough place in a fractured world....You want a mix of pay and free."

VideoNuze readers know that while I've admired Hulu's user experience from the start, I've long been critical of its thin ad model, which falls well short of generating revenue/program/viewer parity with traditional on-air program delivery. That lack of parity has caused Hulu's owners to cordon off access to Hulu on TVs for most viewers. But the networks' fear of cannibalizing their own P&Ls only frustrates loyal Hulu users, who neither understand nor care about such legacy concerns. All of this and more led me months ago to conclude a subscription offering is inevitable from Hulu. The impending TV Everywhere launches, which further marginalize ad-only business models, and now Carey's public remarks, solidify my thinking. We'll soon see some type of Hulu subscription tier.

2. Move Networks notches a win with Cable and Wireless deal - Score one for Move Networks, which this week announced Cable and its first tier 1 telco customer. Move enables C&W to deliver an HD, linear multichannel video service, plus on-demand and broadband content to its broadband customers, all through existing DSL connections. Move's repositioning, which I wrote about recently, obviates telcos' need to invest billions in upgrading their networks to get into the IPTV business. Indeed, Roxanne Austin, Move's CEO told me yesterday that C&W has for years considered all the various options for getting into video, but has never pulled the trigger until now. The deal covers up to 7 million homes and interestingly, rather than getting a license fee, Move will be paid a share of subscriber revenue. Roxanne says another big deal will be announced shortly.

3. iPod Nano gets video, battle with Cisco's Flip escalates - As you likely know, Steve Jobs unveiled the new iPod Nano this week, which incorporates an SD video camera. Following the iPhone 3GS adding video recording capability, I think it's pretty clear that Apple has decided video is the next big thing for its devices. As I suggested recently, Apple's embrace is going to drive user-generated video - and YouTube, as the undisputed home for it - to a whole new level.

But one wonders what this all means for Cisco's recently-acquired Flip video camera, and others from Creative, Sony, Kodak, etc? Cisco in particular has a lot on the line since it just shelled out almost $600M for Flip's parent Pure Digital. Granted Apple's devices are still SD, while Flip now emphasizes HD, but still, getting video recording "for free" as Jobs put it at the launch is pretty compelling for consumers. Even if the Flip deal doesn't work out as planned, Cisco will still be selling a whole lot more routers to handle all of this newly-generated broadband video, so it's a winner either way.

4. AT&T Wireless adding 3G capacity - In last Friday's "4 Items" post, I noted a great story the NY Times ran showcasing the frustrations that AT&T Wireless customers are experiencing due to the millions of data-intensive iPhones clogging up the network. AT&T has been hearing complaints from all sides, and this week announced 3G network upgrades in 6 cities this year, with plans to cover 25 of the top 30 U.S. cities by the end of next year, and 90% of its current 3G footprint by the end of 2011. These upgrades can't come soon enough for iPhone users. Meanwhile the company's YouTube video, featuring "Seth the blogger guy" explaining how AT&T is addressing network issues itself came under attack, as AdAge reported. There's no pleasing everyone.

Enjoy the weekend!

Categories: Advertising, Aggregators, International, Mobile Video, Technology, Telcos

Topics: Apple, AT&T, Cable and Wireless, Cisco, Hulu, iPod Nano, Move Networks, News Corp.

-

YouTube Movie Rentals: An Intriguing But Dubious Idea

Last week the WSJ broke the news that YouTube is in talks with Lionsgate, Sony, MGM and Warner Bros. about launching streaming movie rentals. On the surface this is an intriguing proposition: the 800 pound gorilla of the online video world tantalizing Hollywood with its massive audience and promotional reach. However, when you dig a little deeper, I believe it's a dubious distraction for YouTube, which is still trying to prove that it can make its ad model work.

I appreciate all the possible reasons YouTube is eyeing movie rentals. To evolve from its UGC roots, the company has been anxious for more premium content to monetize. But with Hulu locking up exclusive access

to ABC, Fox and NBC shows for at least the next year and a half or longer, full-length broadcast TV shows are largely unavailable. And now TV Everywhere threatens to foreclose access to cable TV programs. All this makes movies even more attractive.

to ABC, Fox and NBC shows for at least the next year and a half or longer, full-length broadcast TV shows are largely unavailable. And now TV Everywhere threatens to foreclose access to cable TV programs. All this makes movies even more attractive. Then there's Google's uber mission to organize the world's information. YouTube executives are savvy enough to know that not all content can be delivered solely on an ad-supported basis - not yet nor possibly ever (for more about the challenges of effectively monetizing broadcast TV shows, let alone movies, see my prior posts on Hulu). To succeed in gaining access to certain content, offering a commerce model is ultimately essential. Since YouTube has already put in place some key commerce-oriented infrastructure pieces like download-to-own and click-to-buy, rolling out a rental option is less of a stretch. Lastly, YouTube can position itself to Hollywood as a more flexible partner and viable alternative to Apple's iTunes.

Regardless, YouTube movie rentals are still a dubious idea for at least 3 reasons: they're a distraction from YouTube's as yet unproven ad model, there are too many competitors and too little opportunity to differentiate itself and the revenue opportunity is relatively small.

Focus on getting the ad model working right - Given its market-leading 40% share of all online video streams, I've long believed that YouTube is the best-positioned company to make the online video ad model work. YouTube has made solid progress adding premium content to the site that it can monetize, but it still has a lot of work ahead to make its ads profitable. As I wrote in June, Google's own senior management cannot yet clearly articulate YouTube's financial performance, causing many in the industry to worry about YouTube's sustainability. Some might assert that YouTube can keep tweaking the ad model while also rolling out rentals but I disagree. With the ongoing ad spending depression, YouTube must stay laser-focused on making its ad model work, and also on communicating its success.

Too many competitors, too little differentiation - It's hard to believe the world really needs another online option for accessing movies, and mainly older ones at that. There's Hulu, iTunes, Netflix, Amazon, Xbox and soon cable, satellite and telcos rolling out movies on TV Everywhere, just to name a few. Maybe YouTube has some secret differentiator up its sleeve, but I doubt it. Rather, it will be just one more comparably-priced option for consumers. And in some ways it will actually be inferior. For example, unlike Netflix and Amazon, YouTube's browser-centric approach means watching movies on YouTube will remain a suboptimal, computer-based experience. Unless YouTube is willing to pay up big-time, there's also no reason to believe it will get Hollywood product any earlier than proven services like Netflix and iTunes.

Revenue upside is small - It's hard to estimate how many movie rentals YouTube could generate, but here's one swag, which shows how limited the revenue opportunity likely is. Let's say YouTube ramped up to .5% of its 120M+ monthly U.S. viewers (assuming it had U.S. rights only to start) renting 1 movie per week (not a trivial assumption considering virtually none of YouTube's users have ever spent a dime on the site and there are plenty of existing online movie alternatives). YouTube's revenue would be 600K rentals/week x $4/movie (assumed price) x 30% (YouTube's likely revenue share) = $720K/week. For the full year it would be $37.4M. With YouTube's 2009 revenue estimates in the $300M range, that's about 12% of revenue. Nothing to sneeze at, but not world-beating either, especially as compared to YouTube's massive advertising opportunity.

Given these considerations, I contend that YouTube would be far better off trying to become the dominant player in online video advertising, replicating Google's success in online advertising. Like all other companies, YouTube has finite resources and corporate attention - it should focus where it can become a true leader. There's enough quality content and brands willing to partner with YouTube on an ad-supported basis to keep the company plenty busy, and on the road to eventual financial success.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, FIlms, Studios

Topics: Hulu, Lionsgate, MGM, Sony, Warner Bros., YouTube

-

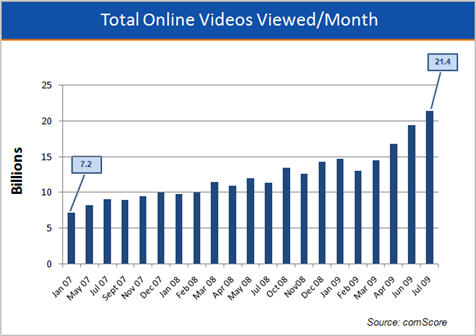

comScore's Online Video Data Charts for Jan '07-July '09 Available for Download

Last Thursday comScore released July 2009 data from its Video Metrix service showing record online video usage for the month. I've been charting comScore's data for 2 1/2 years, making updates each month when comScore provides new data. Today I'm offering these charts as a complimentary download (if you incorporate them into your presentations please identify comScore as the source). Here's an example slide for total online videos viewed per month:

Not surprisingly, a number of content providers have informally told me that their internal data and what comScore reports for them doesn't neatly tie out (anyone who's ever tried to reconcile number from internal analytics, ad servers and external measurement sources can relate to these discrepancies). Nonetheless, comScore's data provides at least one consistently-measured data set on the industry, which is quite useful.

Some of the record July numbers benefit from Michael Jackson's death and also from the lull in original TV episodes. Still, the comScore trendlines are pretty impressive. I share these charts at the beginning of presentations that I often make to industry executives to underscore broadband video's rapid growth. Some of the more noteworthy numbers that are highlighted on the slides include:

- A near tripling of total videos viewed per month from 7.2 billion in Jan '07 to 21.4 billion in July '09.

- A 229% increase in the average number of online videos watched per viewer per month from 59 in Jan '07 to 135 in July '09.

- A 331% jump in the number of minutes of video watched per average viewer per month from 151 minutes (2 hours 31 minutes) in Jan '07 to 500 (8 hours 20 minutes) in July '09.

- Looking just at YouTube, its share of all videos viewed has increased from 16.2% in Jan '07 to 41.9% in July '09. YouTube is the 800 pound gorilla of the market month in and month out. For example, in July '09, the #2 ranked video provider was Viacom Digital with 3.8% share of views, less than a tenth of YouTube's. YouTube accounts for nearly all of Google's 8.9 billion monthly views. To help put that number in perspective, it roughly equals the industry's total views in Sept '07. YouTube is also used more intensively than any other video site, with 74.1 average videos per viewer vs. #2 Viacom Digital with 19.2 average videos per viewer.

- Hulu's monthly videos viewed have increased from 88 million in May '08 to 457 in July '09, a greater than 5x increase in just its first 15 months in existence.

By virtually every measure the industry continues to experience rapid adoption. As I've noted before, in addition to continuing to grow viewership, the industry's key challenge is to further monetize all this video, either through advertising or paid models (subscriptions, pay-per-use or as a value add to other paid services).

What do you think? Post a comment now.

Categories:

Topics: comScore, Hulu, YouTube

-

Hulu is Broadcast TV Networks' Best Bet for Generating Online Video Payments

Last Monday, in "Netflix's ABC Deal Shows Streaming Progress and Importance of Broadcast TV Networks," I tried making the case that from Netflix's perspective, in order for its Watch Instantly streaming service to succeed, it would most likely need to strike more deals with the broadcast TV networks (as it announced with ABC).

Now how about the flip side of the question: how can broadcast TV networks make online video payments a significant revenue stream?

There is certainly no lack of interest by broadcasters in getting paid for online access to their content. For example, CBS has joined Comcast's TV Everywhere trial, and its CEO Leslie Moonves has been outlining his arguments for why cable's authentication plans should generated new revenue for the network. News Corp head (and Fox owner) lately Rupert Murdoch hasn't been shy about his interest in charging for content, though his first focus appears to be on newspapers. And Disney CEO Bob Iger (and ABC owner), recently told the WSJ, "People are going to pay for content. We are not worried about that." Meanwhile NBC's Jeff Zucker is trying to reposition NBCU as a cable network company (i.e. one that sells ads AND gets paid for its programs).

For broadcast TV networks though, figuring out how to get paid for online distribution is not trivial. Years of giving viewers free access to their shows has set expectations. Consider for example recent CBS research in which respondents were asked if they could watch a program online for free with commercials or pay $1.99 for it; 92% chose the former. This echoes mountains of research that has reached similar conclusions (a conundrum likewise bedeviling newspapers who are also seeking to charge for their content).

As I think through how broadcasters can succeed with getting paid, I keep returning to 3 core beliefs: first, broadcasters' efforts should not be undertaken individually, but rather through its joint initiative Hulu, second, the model needs to be subscription-based, not per program-based and third, the subscription service should be made in partnership with incumbent video service providers (cable, satellite, Netflix, etc.) and convergence device makers (Roku, Xbox, etc.).

Hulu has established a strong online brand, built a large audience and demonstrated online savvy. I have the most confidence in Hulu to be able to identify the differentiators needed to drive new value vs. free,

including things like more timely access to hit programs, deeper libraries, higher quality streaming, options for downloading and mobile, etc. And assuming the federal government didn't step in and cry "collusion!" Hulu would provide the greatest negotiating leverage.

including things like more timely access to hit programs, deeper libraries, higher quality streaming, options for downloading and mobile, etc. And assuming the federal government didn't step in and cry "collusion!" Hulu would provide the greatest negotiating leverage. The key challenge for Hulu would be gaining the rights from the networks, producers, talent and others to launch such a comprehensive service. These stakeholders would be understandably wary, not knowing exactly how to value what they'd be providing.

Several months ago, I suggested a Hulu subscription service was in the offing, but so far Hulu has stayed on message, only emphasizing its free, ad-supported model. I hope it and its parents recognize that time is of the essence. With each passing day, as more people use Hulu ever more intensively, their expectations for free are being set, thereby raising the bar on their eventual willingness to pay. I do believe broadcast networks have any opportunity to evolve their business model and charge, but they must not dither. The online medium is still immature enough that they can influence its rules by acting now.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters

Topics: ABC, CBS, FOX, Hulu, NBC

-

Catching Up on Last Week's Industry News

I'm back in the saddle after an amazing 10 day trip to Israel with my family. On the assumption that I wasn't the only one who's been out of the office around the recent July 4th holiday, I've collected a batch of industry news links below so you can quickly get caught up (caveat, I'm sure I've missed some). Daily publication of VideoNuze begins again today.

Hulu plans September bow in U.K.

Rise of Web Video, Beyond 2-Minute Clips

Nielsen Online: Kids Flocking to the Web

Amid Upfronts, Brands Experiment Online

Clippz Launches Mobile Channel for White House Videos

Prepare Yourself for iPod Video

Study: Web Video "Protail" As Entertaining As TV

In-Stat: 15% of Video Downloads are Legal

Kazaa still kicking, bringing HD video to the Pre?

Office Depot's Circuitous Route: Takes "Circular" Online, Launches "Specials" on Hulu

Upload Videos From Your iPhone to Facebook Right Now with VideoUp

Some Claims in YouTube lawsuit dismissed

Concurrent, Clearleap Team on VOD, Advanced Ads

Generating CG Video Submissions

MJ Funeral Drives Live Video Views Online

Why Hulu Succeeded as Other Video Sites Failed

Invodo Secures Series B Funding

Comcast, USOC Eye Dedicated Olympic Service in 2010

Consumer Groups Push FTC For Broader Broadband Oversight

Crackle to Roll Out "Peacock" Promotion

Earlier Tests Hot Trend with "Kideos" Launch

Mobile entertainment seeking players, payment

Netflix Streams Into Sony Bravia HDTVs

Akamai Announces First Quarter 2009 State of the Internet Report

Starz to Join Comcast's On-Demand Online Test

For ManiaTV, a Second Attempt to be the Next Viacom

Feeling Tweety in "Web Side Story"

Most Online Videos Found Via Blogs, Industry Report

Categories: Advertising, Aggregators, Broadcasters, Cable Networks, Cable TV Operators, CDNs, Deals & Financings, Devices, Indie Video, International, Mobile Video, Technology, UGC

Topics: ABC, C, Clearleap, Clippz, Comcast, Concurrent, Hulu, In-Stat, Invodo, iPod, Kazaa, Nielsen, Office Depot, Qik, VideoUp, YouTube

-

VideoNuze Report Podcast #19 - June 5, 2009

Below is the 19th edition of the VideoNuze Report podcast, for June 5, 2009.

Daisy was in New York this week for the "NewFronts," a day-long meeting that Digitas sponsored, mainly for independent online video creators and media buyers/agencies. The goals were to educate the market and fuel advertiser interest. Daisy reports that despite the mixed news coming out of the independent video world this year, it was an upbeat gathering.

I provide additional detail on Microsoft's announcement this year of new entertainment-oriented features for XBox 360. The gaming console continues to take on more of a convergence positioning, with new instant-on 1080p video, live streams, Zune integration, etc. With an installed base of 30 million users, Microsoft has a prime opportunity to drive convergence and get a video foothold. The new Xbox 360 features coincide with last week's Hulu Desktop announcement and this week's YouTube XL unveiling.

Click here to listen to the podcast (14 minutes, 47 seconds)

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Advertising, Aggregators, Devices, Indie Video, Podcasts

Topics: Digitas, Hulu, Microsoft, NewFronts, Podcast, XBox, YouTube

-

YouTube XL Reflects Google's Browser-Centric Worldview

YouTube's announcement this week of "YouTube XL," an optimized version of its site meant for viewing on larger screens caught my attention as it appeared to be another building block in broadband-to-the-TV convergence. I spoke with Chris Dale, a YouTube spokesman to learn more.

On the one hand YouTube XL is a great offering for early adopters who have connected their computers directly to their TVs. XL offers large, easy-to-use navigation that scales depending on the size of your display and HD video quality. And Chris added that given Chrome and Android compatibility, XL creates some very cool functionality. Some video isn't yet rights-cleared, that will likely change over time. XL builds on the "YouTube for Television" initiative introduced in January for Sony PS3 and Nintendo Wii.

On the other hand, long-term, XL is a limited-appeal offering, because it reflects Google's browser-centric worldview. As Chris explained, from CEO Eric Schmidt on down, there's a conviction that the "browser as the platform" is going to dominate entertainment and information distribution. This is certainly the way the online world works today, as practically all of broadband-delivered video is consumed within a browser context. (In fact, this is one of the things that made last week's Hulu Desktop announcement so noteworthy, a large aggregator introducing an app that breaks the browser-only paradigm.)

The problem is that historically at least, the non-online, TV world hasn't been browser-based. Instead, various set top boxes (whether from cable/satellite/telco or from newer convergence players) rely on their own applications to present and manage video. Given this disconnect, new convergence devices and services will instead need to rely on YouTube APIs if they want to access YouTube's vast trove of content, unless they start building in browsers. This is how AppleTV, Sony Bravia, TiVo and others have worked with YouTube in the past. My concern is how much investment attention will convergence-oriented APIs be getting from YouTube when the company's emphasis is clearly on the browser.

Back in March '08, I wrote, "YouTube: Over-the-Top's Best Friend" in which I asserted that for emerging convergence devices and video service providers, YouTube would be the perfect partner. It has the best-known video brand, the largest catalog and the best promotional reach. I still believe that. YouTube could be a formidable disruptive force in over the top if it had a strategy to do so. With its browser focus though, it's hard to see that happening.

In these tough economic times, I don't blame YouTube, or others, from prioritizing. However, my sense is that by taking a more passive approach to convergence, YouTube is opening the door a little wider for others like Netflix who are more aggressively pursuing convergence opportunities, as well as incumbents like Comcast and Time Warner Cable who are just getting going on bridging broadband video to their set-top boxes. As the clear online video market share leader, YouTube has a pretty golden opportunity to aggressively chart new ground and cause likely market disruption. That it's choosing not to means others have a little less pressure on them.

What do you think? Post a comment now.

Categories: Aggregators, Devices

-

May '09 VideoNuze Recap - 3 Key Themes

Following are 3 key themes from VideoNuze in May:

1. Hulu Moves to Center Stage

Already on a roll, Hulu gained lots of mind share in May. After YouTube it is clearly the most-buzzed about video site - not a bad accomplishment for a site that just celebrated its one year anniversary.

The month began with the announcement that Disney would invest in Hulu, at last making available ABC and other programs in Hulu's ever-growing portal. Hulu gained stature during the month as the statistic from comScore released in late April - that Hulu was now the #3 most-popular video site, with 380 million video views in March - was repeatedly recirculated. (Hulu was separately disputing data released from Nielsen showing a far-smaller audience.)

In addition to the Disney content, Hulu also announced its first live event, tonight's concert from the Dave Matthews Band. Capping the month was last week's Hulu Labs announcement, showcasing the desktop app that moves Hulu one step closer to being TV-ready.

Hulu's growth and top-notch user experience continue to set the pace in the online video world. Still, as I noted in my post about the Disney deal, what's still unproven is the Hulu business model and how it plans to navigate the convergence of broadband and TV. The spin coming from its owners is that financial progress is being made, yet Hulu's per program viewed revenues continue to be a fraction of those derived from on-air viewership. Sooner than later, I predict the Hulu growth story is going to start to give way to the Hulu financial story, which may yet include subscriptions.

2. Susan Boyle Shows Power and Conundrum of Viral Video

It was hard to miss the Susan Boyle phenomenon in May. As of last Thursday (before the finale of "Britain's Got Talent" in which she placed second) her original video had generated over 235 million views, according to tracking firm Visible Measures. Ms. Boyle's sensational performance has mainstreamed the term "viral video." The idea that you can become a worldwide personality is truly a broadband-only invention.

Yet 3 1/2 years after SNL's "Lazy Sunday" video became the first bona fide big media YouTube hit (despite NBC's efforts), the process for copyright holders and distributors to monetize these viral wonders remains immature. The NY Times described the interplay over the Boyle viral videos between YouTube, Fremantle, ITV and others, and why those hundreds of millions of views are still under-monetized. But with broadband distribution's increasing importance, this won't last; viral monetization rights are inevitably going to become a key part of the upfront negotiating mix.

3. Mobile video growth

Mobile video continued to get a lot of attention from content providers, service providers and handset makers in May, with initiatives from NBC, NBA, E!, Samsung, Sling, among others (a full listing of mobile video news is here). The mobile video ecosystem is responding to data indicating surging consumer acceptance, primarily driven by the iPhone. In May Nielsen released a report indicating mobile user growth from Feb '07 to Feb '09 was 74%, and that iPhone users are 6 times more likely to consume mobile video. The crush of new smartphones coming in the 2nd half of '09 promises that mobile video usage is going to continue growing rapidly. Limelight's acquisition of mobile ad insertion company Kiptronic is likely the tip of the deal iceberg as companies position themselves for mobile.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Mobile Video, Video Sharing

Topics: Disney, Hulu, iPhone, Kiptronic, Limelight, NBC, YouTube

-

Hulu Desktop Induces More Head-Scratching About Role of Screens

Yesterday Hulu announced Hulu Labs - "a place to try out experimental projects from Hulu and share your feedback while they're still in development." Four current projects are listed, "Hulu Desktop," "Video Panel Designer," "Recommendations" and "Time-Based Browsing."

Hulu Desktop, a browser-less app for surfing videos with a Windows Media Center or Apple remote

controls moves Hulu yet another step closer to the proverbial "10 foot" or TV-like experience. Yet as Peter Kafka at AllThingsD rightly notes, Hulu continues to draw a seemingly arbitrary distinction between screens. It's fine with the Hulu folks to use Desktop to watch on a large monitor connected to your computer. But if you want to watch on an actual TV (via Boxeee, for example) that's a no-no.

controls moves Hulu yet another step closer to the proverbial "10 foot" or TV-like experience. Yet as Peter Kafka at AllThingsD rightly notes, Hulu continues to draw a seemingly arbitrary distinction between screens. It's fine with the Hulu folks to use Desktop to watch on a large monitor connected to your computer. But if you want to watch on an actual TV (via Boxeee, for example) that's a no-no. So even as Hulu admiringly pushes the bounds to improve its users' experiences, it is going to continue to find itself in wrapped around the axle trying to explain itself. What would change all this and make Hulu's owners agnostic to whether you watch Hulu's programs on PCs or TVs? Simple: Hulu demonstrating it can generate ad revenue at parity (or better) with traditional on-air delivery. Once it can do that, then these distinctions will melt away. Problem is, despite Jeff Zucker asserting that Hulu is ahead of plan, the reality is that Hulu is nowhere close to achieving parity (nor has it shared a roadmap for doing so).

Until this happens, things like Hulu Desktop are neat, but will only cause more head-scratching among Hulu's tech-savvy early-adopter audiences.

What do you think? Post a comment now.

Categories: Aggregators

Topics: Hulu

-

Other Analysts Waking Up to Concerns About Hulu's Business Model

I have to say, I chuckled a little when I read this morning's Online Media Daily story, "Opening a Pandora's Boxee" about a new report from Laura Martin at Soleil Securities titled "Content's $300B Gamble." I haven't read the report, but the article says that it expresses concern that ad revenues for programs watched online could be 60% lower than when watched on-air, "threatening TV's the TV platform's price umbrella."

The reason I chuckled is because I've been saying the same things for months now (for example, see "Broadcast Networks' Use of Broadband is Accelerating Demise of Their Business Model" and "OK, Hulu Now Has ABC. But When Will It Prove Its Business Model?") It's nice to see others starting to understand these important issues as well.

Recently I've had a number of conversations with TV and broadband executives who are similarly concerned about what role Hulu is going to play longer term for the broadcast industry, given the current absence of a proven business model for the site. There are some pretty strong feelings out there, ranging from "Hulu is totally misguided and will be the downfall of the broadcast industry" to "the Hulu team is so smart, they're bound to figure it out." One way or the other, with Hulu's growing popularity, I continue to believe that the broadcast industry's fortunes are increasingly tied to Hulu's financial success.

What do you think? Post a comment now.

Categories: Advertising, Aggregators

Topics: Hulu

-

Recent Cable, Broadcast Financial Performance Suggests Hulu Subscription Model Should be Coming

As the annual "upfronts" - the TV industry's program preview and ad sales extravaganza - kick off today, the recent financial performance of the network TV industry and the cable TV industry continue to diverge. The cable network model, powered by both ad sales and monthly affiliate fees, is proving very durable in the Great Recession, while the ad-only network TV model has been hammered. One conclusion from these numbers is that Hulu's owners must be pushing to figure out how the site can introduce a paid subscription model.

I pulled together financial information for a select group of companies comparing performance for the recently concluded March 31 quarter vs. a year ago.

As the chart shows, operating income increased for all the cable networks and revenue was up for all of them as well, except Scripps Networks, where it was flat. The press release commentary from these cable networks was the same: affiliate revenues are up, with ad sales soft, but not disastrous. Cable operators like Comcast and Time Warner Cable also fared well in the quarter with both revenue and operating income/cash flow increasing.

Contrast this with the broadcast TV numbers for Disney, Fox and CBS, all of which operate both TV networks and own local TV stations. Disney fared the best, with revenues down 2% and operating income down 38%. CBS followed with revenues down 12% and operating income down 49%. Fox was affected the worst, with revenues down 29% and operating income down 99%. As two examples of purely local station performance, Gannett's broadcasting segment revenues were down 16% and operating income down 24%, with Sinclair's revenues down 19% and operating income down 43% (before an impairment charge). The commentary from all the broadcasters was the same: the ad market is terrible, and they're doing their best to contain costs (meaning laying off staff).

As the TV industry gears up to sell billions of dollars of ad time this week, a clear lesson from the above financial performance is that it is essential to diversify into the paid subscription ecosystem instead of relying on advertising alone. Disney, Fox and NBCU have recognized this for a while and have strongly built up their portfolio of cable networks.

With ad sales in the doldrums, it's hard not to wonder what Disney, Fox and NBCU, the three major owners of Hulu, are thinking about with respect to Hulu's own business model, which is of course currently 100% reliant on ads. I mean, if your incumbent business model is frayed, wouldn't it make sense, when essentially "starting over" online, to aggressively pursue the one that is resilient even in the recession?

Hulu's exclusive online lock on high-quality programming from 3 of the 4 broadcast networks would seem to position the company perfectly for a subscription play. If its owners looked hard at the divergent fortunes of cable vs. broadcast, it seems inevitable we'll see some type of paid subscription offering from Hulu - either directly or through distributors - sometime in the near future.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks

Topics: CBS, Disney, FOX, Hulu, NBCU

-

April '09 Recap - Innovation is Alive and Well in the Broadband Video Space

Looking over last month's posts with an eye for 2-3 themes to extract for my recap post today, I was instead struck by one overarching theme: innovation is alive and well in the broadband video space. Other sectors of the economy may have ground to a halt in the current recession, but whether it's new technologies, new service models or new approaches by traditional media companies, the pace of innovation in all things related to broadband video seems only to be accelerating.

Here are some of the examples from last month's posts:

New technologies

- SundaySky - a new approach to dynamically generate videos out of web site content

- HD Cloud - cloud-based encoding and transcoding plus 3rd party syndication

- Market7 - web-based platform for collaboratively creating and producing video

- FreeWheel - ad management/distribution company raises another $12M

New service models

- Sezmi - next-gen video service provider aiming to replace cable/satellite/telco

- TurnHere - distributed video production services for the corporate market

- Babelgum - premium-quality content destination for independent producers

- YuMe Mindshare iGRP - new measurement unit to compare on-air and online ad performance

- YouTube-Disney - short-form promotional deal

New approaches by traditional media companies

- Disney-Hulu - Exclusive 3rd party online distribution for established broadcast network

- Cable networks launching webisodes - online initiatives to attract and retain new online audiences

- New York magazine video re-launch - emphasis on curating best-of-the web videos with brand

- WWE Smashup - fan-submitted video mashup content driving awareness of on-air special

Now granted I have an eye out for broadband innovations so this list is somewhat self-serving. But remember that for every item above I was probably pitched on 2-3 others that I didn't write about due to time limitations. Some of these other items may have been picked up by other news outlets and captured in the news aggregation side of VideoNuze, while plenty of them likely received little attention.

My point is that throughout the whole broadband video ecosystem there is a vibrant sense of entrepreneurialism that is slowly but surely remaking the traditional video landscape. To be sure, not all of this stuff is going to work out; either business models will be faulty, technologies won't deliver as promised or consumers will reject what they're being offered. Nonetheless, from my vantage point, the wheels of innovation continue to spin faster. That makes it a very exciting time to be part of the industry.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Technology

Topics: Babelgum, Disney, FreeWheel, HD Cloud, Hulu, Market7, New York, SezMi, SundaySky, TurnHere, WWE, YouTube, YuMe

-

OK, Hulu Now Has ABC. But When Will It Prove Its Business Model?

OK, Hulu now has ABC in its corner for the next 2 years, along with a re-upped program exclusivity commitment from NBC and Fox. But the nagging question remains: even with all its premium content, fabulous user experience and surging traffic, when will Hulu prove its business model? How that question gets answered will be the real test of Hulu's ultimate success. And with 3 of the 4 broadcast networks now hitching themselves to the Hulu locomotive, the answer is also going to be pivotal to how the industry navigates the broadband video era.

To be clear, VideoNuze readers know that I've been a big fan of Hulu from Day 1. The site has only gotten better over time, not only with more content added, but by continued improvements in the user experience. All of this has no doubt contributed to Hulu's rapid rise up the usage rankings, landing it in the top 3 for the first time in March, with 380M views, according to comScore.

A source familiar with the Disney deal told me the deal was entirely predicated on Disney's desire to tap into Hulu's audience in order to increase ABC's online reach. Among other evidence indicating Hulu's upside potential, comScore data apparently showed that only 8% of the ABC.com audience visits Hulu and only 13% of the Hulu audience visits ABC.com.

To me, three indicators of how much the Hulu deal meant to ABC are the 2 year exclusivity commitment, the

redistribution rights for ABC programs to 3rd parties Hulu gained (except for grandfathered ABC partners), and that ABC will allow its programs to be viewed outside of its much-celebrated video player for the first time.

redistribution rights for ABC programs to 3rd parties Hulu gained (except for grandfathered ABC partners), and that ABC will allow its programs to be viewed outside of its much-celebrated video player for the first time. Importantly, the former two terms effectively foreclose any full-length program distribution deal with YouTube and others. For now at least, ABC will limit its relationship with YouTube to clips only. That's a pretty big call; remember YouTube is the category leader that not only has a 40% share of the market, but is also currently over 15 times the size (in streams) of Hulu. There's also YouTube's relationship with Google, which of course has the most formidable online monetization engine (albeit one that hasn't been fully leveraged by YouTube as yet).

The YouTube decision underscores my ambivalence about the broadcast networks' singular embrace of Hulu because there's little evidence that Hulu has yet developed a profitable or sustainable business model. I've written previously about the paucity of ads in Hulu (and broadcasters' own sites for that matter) and how this is creating user expectations that are going to be hard to reset when more ads are inevitably loaded in. One of the reasons users love Hulu is because it is so light on ads. But will Hulu's traffic flatten or decline when the non-skipppable ad load is 2x, 3x or 4x what it is currently?

Increasingly though, it's not just the ad quantity that's an issue for Hulu, it's also its ad quality. I took some time last night to sample a number of programs on Hulu ("Fringe," "Family Guy," "The Office," "The Daily Show," "Bones"). What I found were the same repetitious ads running throughout all the shows, from a relatively small number of advertisers such as Nissan, AT&T and Swiffer. I detected no meaningful targeting (e.g. I saw a number of Swiffer ads that seem misdirected at this 45 year-old male viewer). Worse, there were an alarmingly high number of PSAs (likely unpaid) from the likes of the Ad Council, Goodwill, One Laptop Per Child, American Diabetes Association, etc. In some cases these were the only ads playing during an entire episode.

Further, there was no evidence of customized ad creative or formats meant to incent deeper engagement (unless you count the companion banners prompting users to click to learn more). Deeper engagement and interactivity are supposed to be the calling cards of broadband video advertising. But the ads on Hulu appear to be the same as seen on-air, suggesting Hulu hasn't been able to persuade its brand advertisers to invest in custom creative to leverage the Hulu environment.

Now I know we're in a recession, but still, over a year since Hulu's official launch, and with its tremendous traffic growth, I think all of this is cause for real concern. Hulu is being embraced by the broadcast industry as its main online video vehicle, yet it isn't close to proving it has a model that can actually make money. I don't have insight as to what's going on here, but I hope the networks that are exclusively entrusting their prized programs to Hulu - and consequently incenting huge real-time shifts in viewer behavior - do.

Longer term of course, the networks' bet on Hulu becomes even more profound. That's because as convergence devices of every stripe bring broadband viewing all the way to users' TVs, there's going to be inevitable cannibalization of viewing traditionally done through linear on-air/cable delivery. (Btw, despite much-heralded research to the contrary, anecdotal evidence suggests this is happening already. Just go ask any college student about their viewing behavior.)

Down the road, networks are going to be increasingly reliant on broadband-based ad revenue as their main meal ticket. And if all that's being served up are digital pennies, nickels or dimes - as I believe Hulu is delivering today - then even all the usage in the world will still leave the networks very hungry indeed.

Now that ABC has thrown in with Hulu, you have to believe CBS will as well. With all of the networks on board, they're increasingly betting the industry on the hope that Hulu can figure out its business model. For their sake, let's hope it can.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters

Topics: ABC, CBS, FOX, Hulu, NBC

-

Disney to Buy Into Hulu

Here I am at BWI airport getting ready to send today's VideoNuze email and in pops the news that Disney is taking an equity stake in Hulu, bringing lots of its prized programming along. The rumor mill has swirled for a while that a deal was forthcoming, now it's here. The press release is not yet up on the Disney site. I'll have more thoughts later.

Categories: Aggregators, Broadcasters, Deals & Financings

-

YouTube Continues Its March Up the Content Quality Ladder

Late yesterday YouTube announced "a new destination for TV shows and an improved destination for movies," moves that continue the site's evolution from its UGC/video sharing roots to an aggregator of premium-quality video.

The reality is that this evolution has been underway for some time now, and I expect it will only continue. Two weeks ago in "6 Reasons Why the Disney-YouTube Deal Matters" I explained again why, as the 8,000 pound gorilla of the online video market, YouTube is in an excellent position to partner with premium content providers. In a media landscape marked by massive audience fragmentation, the online destination (YouTube) that accounts for 40-50% of all streams and is 15 times as big as the #2 destination (Hulu) is quite simply a must-have promotion and distribution partner.

The new destinations address what has been an ongoing Achilles' heel for the site - enabling users to easily find premium video "needles" in YouTube's user-generated "haystack." YouTube's UI weaknesses for

premium video have been highlighted by the gold-plated user experience Hulu - and more recently TV.com and Sling.com - have brought to market. The sites have quickly gained passionate fans, and at least in the case of Hulu, significant viewership.

premium video have been highlighted by the gold-plated user experience Hulu - and more recently TV.com and Sling.com - have brought to market. The sites have quickly gained passionate fans, and at least in the case of Hulu, significant viewership. From a design perspective, while there's nothing I would call truly breakthrough about YouTube's premium destinations, they are still a step forward and a solid start. For users solely interested in premium content, they help organize things nicely. There's a decent selection of content, including titles from deals with MGM, BBC, CBS, Crackle and Lionsgate and lots of other partners, which will no doubt continue to grow.

Possibly more important though, is that for content providers they show how YouTube is serious about addressing their needs for clean, well-lit spaces. Premium content providers want the benefits of being in the massive YouTube site, but without the risk of their brands showing up too close to scruffy UGC material. Being clustered with other premium content is a must.

YouTube's concurrent beta launch of Google TV Ads Online, which allows targeted instream ads, is another positive for premium content providers. Beyond YouTube's massive traffic, Google's potent monetization capabilities are the other reason I've been so bullish on YouTube's prospects for premium content. As I wrote on Monday, with increased DVR penetration driving rampant ad-skipping, broadcast and cable's traditional ad model is looking more and more defunct. Online video ads offer a lot of promise as an even higher value ad medium, but much of it is still unproven. Having large players like Google and YouTube involved is significant for showing online video advertising's true upside.

One last take on this is how YouTube continues to position itself in the "over-the-top" sweepstakes, where multiple competitors are vying to be viewed as bona fide substitutes for cable/satellite/telco subscribers itching to cut the cord. I remain skeptical that the trickle of cord-cutters is going to turn into a gusher any time soon, but I will say that with its move up the content ladder, YouTube continues to burnish its standing as a must-have partner for any convergence device-maker looking to make over-the-top inroads (e.g. Roku, Vudu, AppleTV, etc.). YouTube is the most-recognized online video brand, the most-heavily trafficked, and increasingly a credible alternative to premium aggregators like Hulu and others.

For everyone in the online video ecosystem, YouTube continues to be a key player to watch.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, FIlms

Topics: Disney, Google, Hulu, Sling, TV.com, YouTube

-

YouTube to Merge with Hulu, Entity to be Renamed Either "YouLu" or "HuTube"

In a surprising turn-of-events, VideoNuze has learned that Google will acquire Hulu and merge it with YouTube. The resulting entity will be named either 'YouLu' or 'HuTube.' The merger brings together the two most-trafficked video sites into a powerful new player.

In an interesting twist, the final acquisition price has not yet been determined. Instead, the price will be based on a new algorithm Google is creating to accurately measure just how effective Hulu is at turning its

users' brains into 'creamy giggity-goo' as Seth MacFarlane asserts it will in the latest of Hulu's alien-inspired ads. The algorithm will actually be able to count how many more of users' brain cells die as a result of watching shows on Hulu beyond the cells that already died due to regular on-air network TV viewership.

users' brains into 'creamy giggity-goo' as Seth MacFarlane asserts it will in the latest of Hulu's alien-inspired ads. The algorithm will actually be able to count how many more of users' brain cells die as a result of watching shows on Hulu beyond the cells that already died due to regular on-air network TV viewership. It turns out that Hulu's positioning as an 'evil plot to destroy the world' was considered highly synergistic with Google's longstanding mantra to 'do no evil.' Google CEO Eric Schmidt revealed that the company decided some time ago to move beyond its good-guy image, saying, "Look, we got a lot of mileage out of that 'doing no evil' malarkey, but it's time to get real. We're an avaricious multi-billion company now, and all these wacky tree-hugging green initiatives our engineers keep dreaming up can't hide that." He added, "We really admire the traction Hulu is getting by turning 'evil' into a virtue and want to tap into that concept further. Those Hollywood guys beat us hands-down when it comes to creativity."

For its part, Hulu's owners' decision to merge with YouTube, for a price not yet quantifiable, can only be seen as waiving the white flag of surrender. In an email exchange between Jeff Zucker, NBCU's CEO and Peter Chernin, Fox's former CEO (who made the original Hulu deal), obtained by VideoNuze, Zucker's frustration with Hulu's distant second place status is palpable. Among other things he says, "I thought we had dumbed down our shows as much as possible, but YouTube has clearly tapped into audiences' insatiable appetite for the inane. Who would have thought that skateboard-riding cats crashing into walls would have more audience appeal than our $2 million/episode scripted dramas. There really is no accounting for taste."

In response Chernin is quoted as saying, "Rupert always thought Hulu was a small potatoes deal, not really

capable of losing a large, exciting amount of money. On the other hand, YouTube has been a gigantic black hole for Google, so the opportunity to join forces and achieve scale at losing money together was just incredibly compelling." He added, "Plus, you have to remember, Rupert's heart is really in newspapers. He continues to think this whole Internet thing is a fad that will eventually blow over, with people returning to newspapers as their trusted source of news and propaganda. So the company is logically positioning itself to have sizable video losses to offset expected massive gains in newspaper profitability."

capable of losing a large, exciting amount of money. On the other hand, YouTube has been a gigantic black hole for Google, so the opportunity to join forces and achieve scale at losing money together was just incredibly compelling." He added, "Plus, you have to remember, Rupert's heart is really in newspapers. He continues to think this whole Internet thing is a fad that will eventually blow over, with people returning to newspapers as their trusted source of news and propaganda. So the company is logically positioning itself to have sizable video losses to offset expected massive gains in newspaper profitability."Meanwhile, in a meeting with employees, Hulu CEO Jason Kilar reportedly sought to put a positive spin on the merger. Employees who have Twittered the meeting say that to pump up employee enthusiasm he re-told stories of how much fun it was to originally come up with the name 'Hulu,' reportedly saying, "Look how much mileage we got of one ridiculous-sounding made-up name, just imagine the branding possibilities of the even more-ridiculous sounding names YouLu or HuTube..." Negotiations are already underway with the Chinese portal and domain parking company that own the respective URLs.

The merger left many industry analysts scratching their heads. Representative of their reaction, VideoNuze's Will Richmond said, "Geez, I never thought we'd see a more nonsensical media merger than the one between Time Warner and AOL, but I think this YouLu/HuTube thing might just be it. Let's hope it's not for real, and is just some kind of April Fool's Day joke cooked up by an industry analyst to provide some once-per-year, cheap laughs."

Categories: Aggregators, Deals & Financings

Topics: FOX, Hulu, NBCU, YouTube

-

NBC.com is Missing At Least 75% of Potential Ad Revenue in Obama-Leno Video

Watching President Obama's appearance on "The Tonight Show with Jay Leno" on NBC.com over the weekend was a classic reminder of how so many sites miss out on so much of their total broadband video advertising opportunity.

The interview, which lasts over 24 minutes, carried just one 15 second pre-roll ad, (for Subway, when I watched it) along with a companion banner. Twice during the interview, Leno interrupted the President to pause for a TV commercial break, but when he did so, there was no mid-roll ad inserted by NBC.com. There was also no post-roll ad appended, just a promo graphic for the show itself.

If you figure there were at least 4 potential 15 second avails (1 pre-roll, 1 post-roll and 2 mid-rolls), but only the pre-roll was filled, it means that NBC.com missed out on 75% of the potential ad revenue that each full stream viewer would have generated. In reality the percentage is probably even higher because the mid-rolls could likely be 30 seconds or more.

That degree of under-monetization is pretty disappointing. Don't get me wrong, I'm not advocating that broadband video streams become overwhelmed with ads, which would surely cause a consumer backlash. But I do believe that providers of premium content like NBC.com (and there are few videos more premium than the first time ever a U.S. President has appeared on the "Tonight Show") must recognize and monetize their opportunities effectively. There are at least three reasons why:

First, and most obviously, broadcast networks' poor recent financial performance demands that they seize every available money-making opportunity. Not doing so is just bad business. How many businesses succeed long-term when they don't execute on all chances to generate revenue?

Second, NBC.com and other premium video providers are setting a bad precedent for consumers' expectations. If I can watch 24 minutes of Leno with just one 15 second ad, then if and when NBC.com tries to increase the ad load, I'm inevitably going to be displeased. In short, NBC is devaluing its own content by not serving notice to broadband viewers NOW, that a "price" - in the form of watching ads - must be paid for access.

Third, and tying together the first two reasons, is that it is urgent that networks learn how to achieve economic parity between programs viewed via broadband delivery vs. on-air delivery.

That's because the era of broadband-connected TVs has already begun, and is poised to gain further steam as new devices and connected TVs proliferate.

As this happens, online viewing will no longer be merely supplemental for many viewers to on-air, as it often (thought not exclusively) is today. Rather it will be substitutive. That means viewers will watch Leno via broadband on their TVs, instead of via cable/satellite/telco or over-the-air delivery. Just as "Tonight" would never go 24 minutes on-air without an ad pod (which consists of more than one just 15 second ad btw); NBC.com should never let this happen online. Doing so will cause major damage to its future P&L.

In his Media Summit interview last week, NBCU's Jeff Zucker said the company has already evolved from "digital pennies" to "digital dimes." Yet Hulu's recent stiff-arming of Boxee underscores the reality that networks are nowhere close to economic parity between online and on-air delivery of their programs today. Neither consumers nor technology are standing still waiting for them to catch up. Behaviors, expectations and future economics are being formed right now.

NBC.com - and others - need to be mindful of this and ensure that when they put their premium video online they're fully capitalizing on their ad opportunities. If they don't, then 5 years from now Mr. Zucker will wind up like so many of today's newspaper CEOs - lamenting, not praising, his company's "digital dimes," long after his "analog dollars" have evaporated.

What do you think? Post a comment now.

Categories: Advertising, Broadcasters

-

The Video Industry's Winners and Losers 10 Years from Now: 5 Factors to Consider

Last week a publicly-traded communications-equipment company invited me to speak to a group of investment analysts it had assembled for its annual "investor day." In the Q&A session following my presentation I took a question that I'm not often asked, nor do I give much thought to: "10 years from now, who will be the video industry's winners and losers?"

It's a far-reaching question that doesn't lend itself well to an impromptu answer. Also, while it's great fun to prognosticate about the long run, I've found that it's also a complete crapshoot, which is why my focus is much shorter-term. I've long-believed there are just too many variables in play to predict with any sort of certainty what might unfold 10 years into the future.

Still, as I've thought more about the question, it seems to me that there are at least 5 main factors that will influence the video industry's winners and losers over the next 10 years:

1. Penetration rate of broadband-connected TVs -There's a lot of energy being directed to "convergence" technologies and devices which connect broadband to the TV. Broadband to the TV is a big opportunity for video providers outside the traditional video distribution value chain. It's also a minefield for those who have dominated the traditional model, such as broadcasters. The Hulu-Boxee spat demonstrates this. A high rate of adoption of broadband to the TV technologies will result in more openness and choice for consumers. That's a good or a bad thing depending on where you currently sit.

2. The effectiveness of the broadband video ad model - A large swath of broadband-delivered video is and will be ad-supported. But key parts of the broadband ad model such as standards, reporting and the buying process are still not mature. There's a lot of work going into these elements which is promising. The extent to which the ad model matures (and the economy rebounds) will have a huge influence on how viable broadband delivery is. Producers need to get paid to do good work or it won't get done. The imploding newspaper industry offers ample evidence. Those with robust online ad models like Google are likely to play a key role in helping distribute and monetize premium content.

3. How well the broadcast industry adapts to broadband delivery - The broadcast TV industry generates about $70 billion of ad revenue annually. But both broadcast networks and local stations are on the front lines of broadband's change and disruption, putting a chunk of that ad revenue up for grabs. With broadband-to-the-TV coming, broadcast networks must figure out how to make broadband-only viewership of their programs profitable on a stand-alone basis (i.e. when the online viewing is the sole viewing proposition). Local stations face bigger challenges. As the Internet was to newspapers, broadband delivery is to local stations. They face a slew of new competitors for ad dollars and audiences, while losing their exclusive access to network programming. To what extent they're able to reinvent themselves will determine how much share they hold on to and how much others peel off.

4. How aggressively today's video providers (cable/telco/satellite) and new paid aggregators pursue broadband video delivery - While anecdotes about "cord-cutting" will no doubt only intensify, the reality is that if today's video providers adapt themselves to broadband realities, they are likely to be as strong or stronger 10 years from now. The recent moves from Comcast and Time Warner are encouraging signs that the cable industry gets that being ostriches about the importance of broadband delivery is a road to nowhere. Consumers expect more flexibility and value; incumbents are in a tremendous position to deliver. Ownership of local broadband access networks that serve consumers' unquenchable bandwidth demands is going to be a very good business to be in. That all said, new paid aggregators like Netflix, Amazon and Apple could well steal some share if they aggressively beef up their content, offer a competitive user experience and deliver a better value. They could have a major impact on online movie distribution in particular.

5. The level of investment in startups - The venture capital industry, crucial to the funding of early-stage innovative technology companies, is going through its own turmoil. The industry's limited partners have been wounded by the market's drop, causing VCs to raise smaller funds (if they're even able to do this), limit the number of investments they make, and shy away from betting on big transformational startups. Plenty of strong video technology companies are still successfully raising money, but it's harder than ever. Lots of potentially promising ideas are going begging. The length and severity of the economic slowdown will have a big effect on just how much funding new technologies that can potentially reshape the video landscape over the next 10 years.

So there are 5 factors to consider in how the video landscape shapes up over the next 10 years. Now back to the here and now..

What's your crystal ball say? Post a comment now.

Categories: Advertising, Aggregators, Broadcasters, Cable TV Operators, FIlms

Topics: Boxee, Comcast, Google, Hulu, Time Warner

-

Clarifying Comcast's and Time Warner's Plans to Deliver Cable Programming Via Broadband to Their Subscribers

Summary:

What: Major cable operators Comcast and Time Warner intend to offer broadband access to cable programs for the first time, but they have provided few specifics to date, thereby creating a swirl of confusing interpretations. This post seeks to clarify their plans.

Important for whom: Cable networks, other content providers, cable operators, consumers

Potential benefits: Flexible access and first-time online availability of popular cable programs.

Background

Since the WSJ reported two weeks ago today that Comcast and Time Warner Cable plan to offer online access to cable TV programming to their subscribers, there has been a significant amount of confusion and misinterpretation about what these companies are actually planning to do. Absent official statements from either company, there has been an ongoing debate about whether cable operators, who want to defend their traditional model, were moving to choke off the largely open access to broadband video that users have grown accustomed to.

Things got more confusing this past Monday when AdAge ran an interview ("TV Everywhere -- As Long As You Pay For It") with Jeff Bewkes, CEO of Time Warner Inc. in which he elaborated on a company initiative dubbed "TV Everywhere" that major cable network owners such as Time Warner Inc. Viacom, NBCU, Discovery and others are said to be collaborating on. Bewkes outlined a broad online vision including the idea that cable programming could also be available on sites like Hulu, MySpace, Yahoo and YouTube as well, provided that users were paying a fee to some underlying service provider (cable/satellite/telco).

A wrinkle in the interview was exactly whom Bewkes was speaking for, since Time Warner Inc. (or "TWI" which owns the cable networks CNN, TNT, TBS, etc.) plans to spin off as an independent entity Time Warner Cable ("TWC"), which operates cable systems serving 14 million subscribers. After the split, set for next week, which of these companies would actually be sponsoring the "TV Everywhere" vision?

The NYTimes' technology reporter Saul Hansell then picked up on the interview and wrote a piece on the paper's widely-read "Bits" blog entitled "Time Warner Goes Over the Top," which provocatively began, "Just as soon as Time Warner has divested itself from the cable business, Jeff Bewkes, its chief executive, is preparing to stab the cable industry in the back. That's what I read in an interview with Mr. Bewkes in Advertising Age..."

Saul went on to describe his interpretation of one particular Bewkes comment as implying that Time Warner Inc. would offer its networks directly to consumers (or "over the top" of cable operators), thereby setting off a domino effect in which others' networks did the same, all of which would ultimately lead to the destruction of the cable industry business model.

The attention all of this received, particularly in the blogosphere, prompted a fair number of people to contact me and ask what's really going on here.

Time Warner's Plans

Yesterday I spoke with Keith Cocozza, TWI's spokesman, who said that Bewkes's comments do represent both TWI and TWC. Their mutual vision is to have cable programming offered not just at TWC's

RoadRunner portal, but also at various third-party aggregators (Hulu, etc.) so long as they subscribe to any multichannel video service (whether from TWC, Verizon, DirectTV, etc.). They do envision offering a streaming-only service for those that don't want the traditional cable subscription, but it would only be available in their geographical footprint. All of that means that there's in fact no over-the-top threat involved here at all. TWI and TWC are "agnostic" about third-party aggregator access to the cable programs, because they recognize that people want to go to whatever sites make them most comfortable. And they do not plan to charge subscribers extra for online access.

RoadRunner portal, but also at various third-party aggregators (Hulu, etc.) so long as they subscribe to any multichannel video service (whether from TWC, Verizon, DirectTV, etc.). They do envision offering a streaming-only service for those that don't want the traditional cable subscription, but it would only be available in their geographical footprint. All of that means that there's in fact no over-the-top threat involved here at all. TWI and TWC are "agnostic" about third-party aggregator access to the cable programs, because they recognize that people want to go to whatever sites make them most comfortable. And they do not plan to charge subscribers extra for online access. From a consumer standpoint, all of this is quite enlightened. But from an operational standpoint, it feels incredibly complex. For example, I asked Keith about how a remote user, seeking to watch programs at a third party aggregator's site like Hulu, would be authenticated as an actual customer of a video service provider? While acknowledging it's too early to have all the answers, he said a test TWC has conducted in Wisconsin with HBO has shown this not to be a big technical problem. I don't agree. It's hard enough for companies to do a bilateral account integration (e.g. tying a user's Amazon account to a user's TiVo account); the idea of doing multilateral account integration (the numerous combinations of potential aggregators and service providers) is fraught with complexity and seems highly daunting.

Then there are financial issues to address. With no incremental subscriber payments, online program delivery needs to be sustained through ads alone. This would be quite workable if it were just cable operators and networks involved (they could split the ad avails proportionately as they've traditionally done with linear delivery), but by allowing third-party aggregators in too, a third mouth now needs to be fed. That will trigger a whole new negotiating dynamic, as each aggregator lobbies for a different share. And it's questionable whether there's even enough ad revenue for three parties to begin with, though Keith believes there is.

Comcast's Plans

Conversely, Kate Noel, Comcast's spokeswoman, told me yesterday that while it's still early to say anything definitive about Comcast's plans for distribution through third-party aggregators, their first priority is distribution of

cable programs on their own sites (e.g. Fancast, Comcast.net) and the networks' own sites. Comcast seems to have more of a "walk, before you run" approach. It recognizes that protecting subscribers' privacy in any account integration is crucial so it plans to proceed carefully. I tried to pin Kate down on whether Comcast intends to charge for online access. Again she felt it was too early to be definitive, but it sounds like they're leaning toward a no-charge model as well. The timeline is to begin rolling out access in the 2nd half of '09.

cable programs on their own sites (e.g. Fancast, Comcast.net) and the networks' own sites. Comcast seems to have more of a "walk, before you run" approach. It recognizes that protecting subscribers' privacy in any account integration is crucial so it plans to proceed carefully. I tried to pin Kate down on whether Comcast intends to charge for online access. Again she felt it was too early to be definitive, but it sounds like they're leaning toward a no-charge model as well. The timeline is to begin rolling out access in the 2nd half of '09.Clearly there are a lot of moving pieces involved with these companies' plans. In general Time Warner has a more aggressive, yet I believe far less pragmatic, plan. They're trying to get all the way to the end zone right away, when just advancing the ball further downfield would be real progress for today's broadband users seeking improved access to premium content. Time Warner's "TV Everywhere" seems like a great vision, but it would take years to fully implement. Comcast's plan is probably achievable in a year or less. Either way, major cable operators finally seem to have the ball rolling toward broadband distribution of cable programming. As I pointed out last week, this can only be viewed as a positive.

What do you think? Post a comment now.

(btw, if you want to learn more about all this, come to the Broadband Video Leadership Evening on March 17th in NYC, where we'll dig deeply into these issues with our top-notch panel)

Categories: Cable Networks, Cable TV Operators

Topics: Comcast, Hulu, MySpace, Time Warner Cable, Yahoo, YouTube

Posts for 'Hulu'

Connect with VideoNuze

Exclusive News Roundup

- Google commits to video generation, announces Veo 3.1 Lite 9to5 Google

- Roku launches a standalone app for Howdy, its $2.99 streaming service TechCrunch

- Spectrum TV App to Launch on Amazon Fire TV Devices TV Tech

- Netflix, Eager for More NFL, Is Looking at a Four-Game Package WSJ

- Ampere: Global Subscription Streaming Video Revenue Topped Record $150 Billion in 2025 Media Daily News

- What Is YouTube’s Dominance Doing to Us? We Asked Its C.E.O. NY Times