-

Video Usage is Creating a Hairball for Broadband ISPs, Others

The explosion in broadband video consumption is creating a significant and growing hairball for broadband Internet Service Providers, content providers, regulators and others. The core problem is that ISPs' networks are getting overwhelmed by the sheer volume of video being consumed each day.

ISPs have several ways to address the situation, but unfortunately none are perfect. For example, Comcast's approach until recently has been to use network management tools to block or slow certain kinds of traffic, such as peer-to-peer. P2P is a particular issue for cable ISPs because it uses scarce "upstream" bandwidth. Network management is highly technical, making it hard for policy-makers to understand it, let alone legislate it. So Comcast is now facing a sanction from the FCC over its network management practices (which it says it's moving away from anyway), because the FCC didn't consider them "reasonable" by its own vague definition.

Time Warner Cable is experimenting with another approach: tiers of service carrying bandwidth caps for users. This is a little bit like today's cell phone model - you buy a package of minutes, and if you go over, you pay extra. Though that may sound reasonable, it invites all kinds of confusion for consumers (e.g. "do I watch that show on CBS.com? Maybe I'd better not, I think my kids have watched a lot of YouTube clips this week and I don't want to go over my cap."). Content providers are justifiably concerned about this potential scenario. Separately, for its part, AT&T recently tried to clarify what its users can and cannot expect from their broadband subscriptions.

Yet another route is for broadband ISPs to adopt a much more expansive technical approach to how content is hosted in their networks and delivered to their users. Equipment vendors like Alcatel-Lucent and Cisco believe that ISPs could convert the current bandwidth problem into a full-fledged business opportunity. This would involve ISPs deploying hardware and software that would enable "managed services," each to be delivered at a specified quality level and for a specified price. So rather than a consumer buying a tier, they would buy a specific service offering (e.g. unlimited Hulu, with HD delivery guaranteed).

This wouldn't be a totally unfamiliar concept. Content providers have been buying managed hosting/delivery services for years from CDNs like Akamai, Limelight, Level 3 and others which guarantee certain delivery metrics. But these CDNs' guarantees can't reach into the "last mile" the ISPs' networks serve. So as ever-more bandwidth intensive content is launched such as HD and long-form, content providers should have an increasing motivation to see last mile ISPs offer comparable managed services offerings from ISPs as well.

However, ISP managed services would require fundamental changes in how these companies currently work together, and also invites concerns from "net neutrality" advocates that ISPs could bias in favor of one content provider or another when making their deals. Though compelling in concept, there are many details to sort out in the managed services approach, making it a longer-term option.

All of this just scratches the surface of the growing bandwidth hairball. Layer on the free-speech advocates like Free Press and Public Knowledge and the politicians looking to make hay with constituents and it's evident that the debate over bandwidth is only going to intensify.

What do you think? Post a comment now.

Categories: Broadband ISPs, Regulation

Topics: Alcatel-Lucent, AT&T, Cisco, Comcast, FCC, Net Neutrality, Time Warner

-

thePlatform's New Cable Deals: Finally, an Industry Push into Broadband Video Delivery?

thePlatform, the video management/publishing company that's been a part of Comcast since early '06, had a very good day yesterday. First it jointly announced with Time Warner Cable a deal to power the #2 cable operator's Road Runner portal. And the Wall Street Journal ran a story stating that it has also signed deals with the cable industry's #3 player Cox Communications and #5 player, Cablevision Systems, which thePlatform corroborates.

Netting all this out, thePlatform will now power 4 of the top 5 cable industry's broadband portals (all except

Charter Communications), with a total reach exceeding 28 million broadband homes, according to data collected by Leichtman Research Group. That also equals approximately 44% of all broadband homes in the U.S. And it's a fair bet that thePlatform's industry penetration will further grow.

Charter Communications), with a total reach exceeding 28 million broadband homes, according to data collected by Leichtman Research Group. That also equals approximately 44% of all broadband homes in the U.S. And it's a fair bet that thePlatform's industry penetration will further grow.I caught up with Ian Blaine, thePlatform's CEO yesterday to learn a little more about the deals and whether the industry's semi-standardization around one broadband video management platform harkens a serious, and I'd argue overdue, industry push into broadband video delivery.

Ian noted that of its various customer deals, the ones with distributors like these are particularly valuable because of their potential for "network effects." This concept means that content and application providers are more likely to also adopt thePlatform if their key distributors are already using it themselves. Ian's point is very valid, as I constantly hear from content providers about the costs of complexity in dealing with multiple distributors and their varying management platforms. Yet the potential is only realized if the distributors actually build out and promote their services, offering sizable audiences to would-be content partners.

This of course has been the aching issue in the cable industry. While they've had their portal plays for years, they've been eclipsed in the hearts and minds of users by upstarts ranging from YouTube to Hulu to Metacafe to countless others, each now drawing millions of visitors each month. While solidly utilitarian, cable's portals (with the possible exception of Comcast's Fancast) are not generally regarded as go-to places for high-quality, or even UGC video. That's been a real missed opportunity.

Ian thinks the industry is experiencing an awakening of sorts, now recognizing the massive potential it's sitting on. This includes its content relationships, network ownership and huge customer reach. Of course, all of this was plainly visible in 1998 as broadband was first taking off, yet here we are 10 years later, and it somehow seems discordant to think the industry is only now grasping its strategic strengths.

Some would explain this as the cable industry being more of a "fast follower" than a true pioneer, a posture that has helped the industry avoid hyped-up and costly opportunities others have chased to their early graves. Others would offer a less charitable explanation: the industry's executives have either been asleep at the switch, overly focused on defending traditional closed video models against open broadband's incursion, or both.

In truth, and as I've mentioned repeatedly, the broadband video industry is still very early in its development, making a "fast follower" strategy still quite viable. Semi-standardization on thePlatform gives the industry a huge potential advantage in attracting content providers. It also gives the industry a more streamlined mechanism for bridging broadband video over to the TV, an area of intense interest now being pursued by juggernauts including Microsoft, Apple, Sony, Panasonic and others.

Still, cable operators' broadband video delivery potential (and the true upside of thePlatform's omnipresence) rests more on whether cable operators are finally going to embrace broadband as an eventual complement, and possibly even successor to their traditional video business model. That would be a major leap for an industry better known for cautious, incremental steps. Time will tell how this plays out.

What do you think? Post a comment!

Categories: Cable TV Operators, Devices, Technology

Topics: Apple, Cablevision, Comcast, Cox, Microsoft, Panasonic, Sony, thePlatform, Time Warner

-

Hulu Out-Executing Comcast in On-Demand Programming?

The crew over at Hulu must be gleefully fist-bumping each other this week as Hulu scored a key strategic and public relations coup in adding to its lineup two of Comedy Central's most popular programs, "The Daily Show with Jon Stewart" and "The Colbert Report." Though officially positioned as a test, Hulu still deserves big-time kudos as the deal is an endorsement of its value proposition.

The deal and Hulu's execution illustrate a larger point that I've been making for a while: one of broadband's three key disruptions is that it enables new aggregators to gain an edge on larger incumbents by changing the dynamics of competition. To be more specific, in this case, I think that Hulu has out-executed Comcast, America's #1 cable operator by delivering new value to consumers and gaining important PR momentum. Here's why:

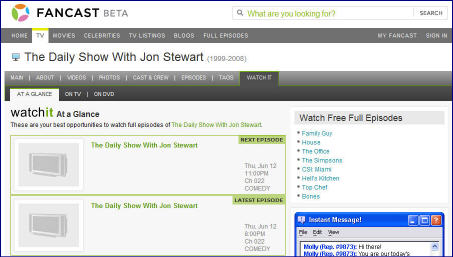

Fancast, which is Comcast's online portal (in beta), actually announced a deal with Comedy Central back on May 19th for access to these same programs and others. Yet go to Fancast and search for "Daily Show" and, as shown below, you won't find any Daily Show full episodes available, just an assortment of short clips and times when it's on TV. A Comcast spokesperson told me that Comcast's implementation is imminent, but its delay in getting the programs up and running is accentuated when you consider that Comedy Central must have done its distribution deal with Fancast BEFORE its deal with Hulu.

Second, and more concerning is that, as a Comcast digital subscriber, when I tried to find The Daily Show and Colbert in Comcast's VOD menu, all that is available are five older Colbert clips and 1 older Daily Show clip. My guess is these haven't been updated in a while. No full-length Daily Show or Colbert programs are available at all in VOD.

While the Comcast spokesperson told me that the company works closely with its programming partners like Viacom to figure out the optimal mix of programming to make available on VOD, I think an unavoidable conclusion here is that Comcast (and other cable operators) is constrained by its inability to monetize VOD programming with advertising (what this week's "Project Canoe" is meant to address) and to easily add new programming on the VOD menu. These programming gaps create opportunities for upstarts like Hulu to capitalize on.

It may be unfair to zero in so narrowly on Comcast's execution with Daily Show/Colbert, yet things weren't much different when I searched for MTV's popular "The Hills" on Hulu, Fancast and Comcast's VOD. While Hulu doesn't appear to have a deal for full episodes of "The Hills" it masks this cleverly by providing thumbail images and easy navigation back to MTV's site where the video lives, for over 50 episodes (this is tactic Hulu uses for ABC's shows as well). On the other hand, Fancast displays just 5 full episodes, 2 from this season and 3 from last. And on VOD there are also just 5 episodes, though all from this season.

I think it's pretty significant that Hulu, a site that only went live 3 months ago can not only gain access to hit Comedy Central programs like Daily Show/Colbert, but can execute quickly. Hulu is using its advantages - flexible technologies, interactive features (clipping, embedding, sharing), monetization capability, savvy PR and startup pluck to compete with far-larger incumbents like Comcast.

Of course Comcast racks up billions of VOD views each year and has vast resources, making it an important player in on-demand programming. Yet Hulu has managed to make Comcast's advantages look a little less intimidating. I asked the Comcast spokesperson about this. She acknowledged Hulu's progress, but maintained that Comcast believes its mulit-platform approach is stronger.

In the big picture that's true, but when it comes to winning consumers' hearts and minds, it's often execution, not broad strategy that carries the day. And don't forget, when Hulu is unshackled from the PC - with its content freely riding Comcast's broadband pipes all the way to the TV - execution will matter even more.

This week Hulu provided a textbook example of how broadband-only aggregators can gain a foothold against well-established incumbents. Comcast and other incumbents should be taking notice and getting their game on.

What do think? Post a comment and let everyone know!

Categories: Advertising, Aggregators, Cable Networks, Cable TV Operators

Topics: Comcast, Comedy Central, Fancast, Hulu, The Colbert Report, The Daily Show, Viacom

-

Where's Project Canoe's New CEO?

At the recent Cable Show in New Orleans, Comcast's president Steve Burke said that Project Canoe's new CEO would be announced on June 1. However, June 1 has come and gone without any news. Project Canoe, which Mugs covered for VideoNuze recently, is the cable industry's new interactive ad system, meant to draw national advertisers to cable's VOD and other advanced video delivery platforms. A rumor has circulated widely that David Verklin, former CEO of Aegis North America (a large advertising service firm) would get the nod, but nothing has been made official. I haven't heard what is causing the delay. If you know, post a comment...

Categories: Advertising, Cable TV Operators

Topics: Comcast, Project Canoe

-

All Eyes on Cable Industry's "Project Canoe"

To the disappointment of many, it looks like there won't be any big news about the cable industry's "Project Canoe" at the Cable Show convention in New Orleans this week.

Project Canoe is a high-profile partnership among the nation's six largest cable companies (Comcast, Time Warner Cable, Cablevision, Cox Communications, Charter Communications and Bright House Networks) to enable national interactive advertising campaigns to be executed across the companies' cable operations. The code-name Canoe is meant to emphasize that cable operators are working together in the same boat, so to speak.

For the past nine months, the partners' Canoe leads have been meeting weekly. Once a top secret initiative, Canoe's existence was leaked in a September, 2007 Wall Street Journal article. But since then there has been no new information, leading to speculation about how much progress has been made.

Yet Canoe remains a top priority throughout the industry, and for good reason. With big advertisers like GM and Intel shifting their once big-budgeted TV ad campaigns to the Internet in significant sums, it's key that the cable operators need to figure out a way to not only protect the $5 billion or so that they generate in spot-cable advertising today, but also to increase their piece of the $70 billion dollar TV ad spend or cut into other slices of the massive US total ad spend pie. The next 3-5 years will be critical as cable advertising, the Internet and broadband video jostle for advertisers' affections.

The buzz in New Orleans suggests advertisers and agencies are excited about Canoe, though its development seems slower than they prefer. Why the slow progress that's perceived? Several operators stated that integrating the infrastructure required to execute Canoe with cable's legacy systems is hard stuff. No doubt. Then of course there are other key priorities weighing on the industry resources, such as the February 2009 digital transition.

Meanwhile, the Internet and broadband video advertising continue steaming ahead, giving advertisers and their agencies the measurement and targetability that they yearn for on TV. Cable operators have been stymied in their ability to jointly offer advertisers easy access to a nationwide or near-nationwide footprint, especially critical for Video on Demand. Canoe addresses this and other opportunities, in part by creating a set of standards for all to follow.

The only Canoe "news" at this week's Cable Show came from Comcast's Steve Burke, who stated that a CEO would be announced on June 1. Comcast is a key player in Canoe, funding between $50-70 million of the $150 million initial investment. Rumors have swirled that David Verklin, who recently stepped down as CEO of Aegis North America (a large advertising services firm) will assume the position of CEO. If true, that could be the news to break on June 1.

For those of us who have been around the interactive advertising and TV mulberry bush for many years, Canoe's potential is exciting. But we're hoping that the Canoe gets it in gear. Paddle on, gang.

What do you think of Project Canoe's prospects? Post a comment now!

Categories: Advertising, Cable TV Operators

Topics: Aegis, Bright House Networks, Cablevision, Charter Communications, Comcast, Cox Communications, Project Canoe, Time Warner Cable

-

Watching the FCC Make Net Neutrality Policy

Yesterday I ignored the well-worn admonition that "there are two things you don't want to see made - sausage and legislation," by attending the FCC's open meeting on broadband network management at Harvard Law School. The hearing's purpose was to collect more information regarding "net neutrality" to

help the FCC develop policy and recommendations on the subject, with a particular focus on what role the FCC should play in determining what are "reasonable" network management practices. As I've said before, net neutrality is very much driven by the surge in broadband video usage.

help the FCC develop policy and recommendations on the subject, with a particular focus on what role the FCC should play in determining what are "reasonable" network management practices. As I've said before, net neutrality is very much driven by the surge in broadband video usage. I have written two posts on this recently, "Net Neutrality Rears Its Head Again" and "Net Neutrality in 2008? Let's Hope Not," and so my views on the subject are well-known. For today, I just want to offer some quick observations about the FCC's meeting and what this implies about how the fight over net neutrality is likely to play out.

The agenda for the day-long session is here. I stayed until the lunch break, so I got a pretty good flavor for the proceedings. On the policy panel I witnessed, all of the non-Comcast/Verizon panelists were in favor of greater government intervention. Despite their articulate views on the subject, one thing that was entirely absent from all of their remarks was any factual data about whether there is currently a market failure necessitating government intervention. Even Vuze CEO Gilles BianRosa, who prior to the panel provide a demo of his company's service, and said his company is playing a "cat and mouse" game trying to stay ahead of Comcast's management practices, did not offer any specific evidence or data of how his company is currently being harmed.

The law school professors were adamant about stricter government oversight of broadband ISPs seemingly because they just cannot be trusted. Unlike economists who rely on empirical data to formulate their viewpoints, the law school professors seem to rely more on a political philosophy regarding government's role to intervene as their primary guiding logic.

On the other hand, Comcast's EVP, David Cohen emphatically denied that Comcast blocks any kind of Internet traffic. He allowed that the company manages its networks, just like all other network providers and has six guidelines. Cohen said Comcast only manages traffic during limited periods, in limited geographies, only for upstream traffic, and then only when there's no simultaneous downstream traffic. It only delays

traffic, and only when there's real network congestion that needs to be alleviated. All of this would only impact a small number of customers, and only then imperceptibly, Comcast believes. Comcast's goal is "vigilant restraint," with an eye to helping the vast majority of its customers have a superior Internet experience.

traffic, and only when there's real network congestion that needs to be alleviated. All of this would only impact a small number of customers, and only then imperceptibly, Comcast believes. Comcast's goal is "vigilant restraint," with an eye to helping the vast majority of its customers have a superior Internet experience.All of this leads me to believe that while Comcast may have the facts on its side, this war will be waged on the PR battlefield. Proponents wrap themselves in the flag, emphasizing the Internet's free-flow of data is paramount to our country's free speech and commerce, while disregarding the fact that to date this has been accomplished with a laissez-faire regulatory policy. Meanwhile network operators like Comcast argue they're already abiding by current regulatory principles and are sufficiently motivated by profit motives to do the right thing. Picking sides, especially in an election year, will be a challenge for all.

What do you think? Post a comment and let us all know!

Categories: Broadband ISPs, Regulation

Topics: Comcast, FCC, Net Neutrality, Verizon, Vuze

-

Net Neutrality Rears Its Head Again

Last November, Jeff Richards, VP of VeriSign's Digital Content Services, suggested to me that "net neutrality" would be the hottest broadband video topic in 2008. I was skeptical, believing that this was a classic "solution in search of a problem" and that yet again this topic would fail to gain traction among regulators and policy-makers. Based on events of the past week, it looks like Jeff may be right and I may be wrong.

Before getting to what happened this week, let's quickly understand what net neutrality means, and why it's important to all of us. To date the Internet has functioned as a level playing field of sorts. Anyone putting up a web site could be confident in the knowledge that broadband ISPs would neither favor nor disadvantage one player's access to users over another's.

Big online content and technology companies now want to codify this tradition in legislation commonly referred to as net neutrality. Big broadband ISPs (i.e. cable operators and telcos) regard this as needless regulatory meddling that would insert the government in network and technical matters it can barely understand, let alone figure out how to regulate.

This week brought news that Congressmen Ed Markey and Chip Pickering have introduced the "Internet Freedom Preservation Act of 2008" which would make net neutrality the guiding U.S. broadband policy, give the FCC additional oversight powers to ensure broadband ISPs weren't discriminating against certain traffic, require the FCC to hold 8 public "broadband summits" to bring together parties to "assess competition, consumer protection and consumer choice issues related to broadband Internet access services" and finally to report all this to Congress along with any recommendations for how to "promote competition, safeguard free speech, and ensure robust consumer protections and consumer choice relating to broadband Internet access services."

Broadband ISPs have precipitated some of this renewed interest in net neutrality with the recent news that they're de-prioritizing or blocking illegal video file-sharing traffic from services like BitTorrent (all of which was already widely understood in the Internet community). Net neutrality proponents have publicly seized on these incidents as evidence that broadband ISPs have discriminatory tendencies in their DNA, and that we're on a slippery slope to a world where broadband ISPs willy-nilly block certain traffic (i.e. their competitors) while favoring other traffic (i.e. their own services).

Last November in "Net Neutrality in 2008? Let's Hope Not." I wrote that there is no substantive current evidence to support this concern and that preemptive net neutrality legislation is unwise and unwarranted. In fact, I believe it's a net positive that broadband ISPs are proactively trying to manage their networks to ensure that legal traffic, generated by paying subscribers, is not adversely affected by the few heavy video file-sharers who diminish the network's performance for everyone. Broadband ISPs' actions help them run more efficient networks and better manage their investments, to the benefit of paying users.

Unfortunately, like many things in Washington, net neutrality is boiling down to a PR battle about how to shape policy-makers' perceptions, regardless of the underlying facts. For its part, Google is unabashedly framing this debate in populist terms, saying "net neutrality is...about what's ultimately best for the people, in terms of economic growth as well as the social benefit of empowering individuals to speak, create, and engage one another online." Huh? How does all that patriotic-sounding babble address the reality that network operators are grappling with 15 year-old kids downloading pirated HD movies, causing real and serious network congestion for everyone?

To defeat net neutrality, broadband ISPs better sharpen up their PR efforts. Congress is notoriously IQ-challenged and politically-motivated. My cynical belief is that its knee-jerk reaction will always be to do what looks best, rather than what actually is best. Then there's the current FCC chairman Kevin Martin, who has a serious anti-cable bias and will likely welcome an opportunity to smack operators. Regrettably, when taken together, Jeff Richards may indeed be right. This might be the hottest broadband video topic of 2008 and the year when net neutrality legislation finally does succeed.

Categories: Broadband ISPs, Regulation

Topics: AT&T, Comcast, FCC, Net Neutrality, Time Warner

-

TiVo + Comcast: My Experience to Date

Yesterday TiVo and Comcast announced that their joint service offering, known as "Comcast DVR with TiVo" is now available to Greater Boston residents. The announcement comes almost 3 years since the

partnership was announced. Multichannel News recently reported that Comcast has funded $24 million of co-development work to date. I have had the service since late October as part of the beta test, but the companies had asked me to stay mum until its official launch.  The first thing to know about this new service is that it really is familiar, lovable TiVo inside a Motorola cable set-top box. I am a long-time TiVo Series 2 owner, and as best I can tell all of the core TiVo features are available (e.g. Season Pass, Wish List, Suggestions) along with the inimitable TiVo blooping sounds effects. The box has a dual tuner so you can record one show while watching another. The navigation also incorporates all of Comcast's VOD selections, so all linear and VOD programs are considered in your searches. It's an HD-capable box, which can hold 15-20 hours of HD video. The peanut-shaped remote control is virtually unchanged.

The first thing to know about this new service is that it really is familiar, lovable TiVo inside a Motorola cable set-top box. I am a long-time TiVo Series 2 owner, and as best I can tell all of the core TiVo features are available (e.g. Season Pass, Wish List, Suggestions) along with the inimitable TiVo blooping sounds effects. The box has a dual tuner so you can record one show while watching another. The navigation also incorporates all of Comcast's VOD selections, so all linear and VOD programs are considered in your searches. It's an HD-capable box, which can hold 15-20 hours of HD video. The peanut-shaped remote control is virtually unchanged.

What's not included are all the wonderful broadband features (e.g. TiVoCast, Amazon Unbox, Rhapsody, Music Choice, Photos, Home Movies, etc.) and network features (e.g. remote scheduling, whole house service). The absence of broadband content (CNET, The Onion, NY Times, etc.) in particular will be missed. TiVo has gradually been introducing this over the last couple years. I've written a lot about broadband-to-the-TV solutions recently, and TiVo's approach has been very solid. However, Comcast obviously wanted to retain strict control over what video gets pumped into the set-top box. I have discussed this "closed" vs. "open" mindset earlier - hopefully something that will change down the road.

The service itself has mostly worked well. There were some initial hiccups requiring the Comcast service techs to return to the house and for me to call in for service. There are a few small issues that have persisted. These include periodically getting a green screen which requires me to turn the box on and off. I can't continuously lower the volume or change channels by suppressing the appropriate button on the remote control (this is possibly a TV-specific issue). I also find the service just a little less responsive than my Series 2 box - my fingers have had to adjust their muscle memory somewhat when working the familiar remote control. None of these are deal-breakers, but I do intend to have Comcast come out a take a look one of these days.

Comcast has priced the service at $2.95/mo, on top of its plain vanilla DVR service fee of $12.95/mo. I continue to believe that for consumers this proposition makes a lot of sense when compared with buying a standalone Series 3 box. It's a $3 delta over paying the monthly service charge directly to TiVo, but you avoid buying the Series 3 box (about $600 street price around $400) and potential maintenance and obsolescence issues. And it means one less box in your rack. The downside is the missing TiVo features described above.

If Comcast markets the TiVo service aggressively and correctly I think they can shift a lot of current DVR subscribers over plus add plenty of new ones down the road. It's a meaningful competitive advantage for a company caught up in a brutal battle with satellite and telco competitors. For TiVo, which has also done a deal with Cox (and others in the future presumably), it's a great shot at migrating itself out of the hardware business, into software and solutions.

Categories: Cable TV Operators, Devices, Partnerships

-

"Comcastic" or "Comcastrophe"?

Last week brought reports of a blistering letter written from Chieftain Capital Management, which owns 60 million shares of Comcast, to the company's board, requesting among other things, the ouster of Brian Roberts, Comcast's CEO for his lackluster stewardship. Playing on the company's advertising tag line, "It's Comcastic", Chieftain called Mr. Roberts's management of the company a "Comcastrophe," reciting a litany of poor financial returns shareholders have endured during Mr. Roberts's tenure.

Although other Wall Street pros fairly yawned at Chieftain's radical proposals - in fact just last week selecting him, for the 2nd year in a row, as Institutional Investor magazine's best CEO in the cable and satellite industry - the letter does provide an opportunity to consider Comcast's stature in the highly

dynamic video marketplace. But rather than looking backwards at Comcast's performance, I'd suggest looking forward and asking: how healthy is Comcast's positioning for future success? Is it closer to "Comcastic" or to "Comcastrophe"?I'd argue that the most important factor determining Comcast's (and other cable operators') future financial success is how well they are embracing delivery of broadband video into their core business models. The adoption of broadband video by consumers, and the enthusiasm for it by content providers large and small are the most crucial fundamental marketplace changes that cable operators are now facing.

This is the case because, as I've said repeatedly over the years, broadband's open access undermines cable operators' traditional closed business model, in which only networks which have so-called "carriage deals" are available to subscribers. This closed approach contrasts with the broadband world, where all programming is accessible by everyone, all the time. Piggybacking on the Internet's own success in driving consumer choice, broadband's openness is poised to drive a stake into the heart of cable's traditional video packaging paradigm and revenue model.

Yet despite this gathering storm, Comcast and other cable operators have been woefully inattentive to explaining how they'll weave broadband video into their TV-based services. Instead, their broadband access businesses, now generating billions of dollars per year in revenues, remain almost entirely siloed from the core video side of the business.

While Comcast should be lauded for initiatives such as broadening Fancast's content, starting Ziddio, announcing an aggressive agenda for bringing more HD content to its VOD menu, and backing Tru2way, none of these directly answer the question of how Comcast will update its closed approach to content, facilitating its subscribers' access to broadband video through their set-top boxes. This would provide for a seamless and highly compelling viewing experience. Comcast's and others' silence is creating the void that is behind the frenzy of activity from technology vendors and consumers trying to kluge the broadband and TV worlds together.

Years since YouTube and others revolutionized consumers' video expectations, the answer as to how Comcast and other cable operators - who effectively "own" the living room video experience - will capitalize on these fundamental changes remains totally unaddressed. Though some investors believe they have already endured a "Comcastrophe", they'd be wise to further reset their expectations. Comcast's ongoing inability or unwillingness to chart a coherent broadband video delivery strategy suggests an even bigger "Comcastrophe" lies just ahead.

What do you think? Post a comment and let us all know!

Categories: Cable TV Operators

Topics: Comcast

-

CES 2008 Broadband Video-Related News Wrap-up

CES 2008 broadband video-related news wrap-up:

Panasonic and Comcast Announce Products With tru2way™ Technology

Panasonic And Comcast Debut AnyPlay™ Portable DVR

NETGEAR® Joins BitTorrent™ Device PartnersD-Link Joins BitTorrent™ Device Partners

Vudu Expand High Definition Content Available Through On-Demand Service

Sling Media Unveils Top-of-Line Slingbox PRO-HD

Open Internet Television: A Letter to the Consumer Electronics Industry

Paid downloads a thing of the past

Samsung, Vongo Partner To Offer Movie Downloads For P2 Portable Player

Comcast Interactive Media Launches Fancast.com

New Year Brings Hot New Shows and Longtime Favorites to FLO TV

P2Ps and ISPs team to tame file-sharing traffic

ClipBlast Releases OpenSocial API

Categories: Advertising, Aggregators, Broadband ISPs, Broadcasters, Cable Networks, Cable TV Operators, Devices, Downloads, FIlms, Games, HD, Mobile Video, P2P, Partnerships, Sports, Technology, UGC, Video Search, Video Sharing

Topics: ABC, BitTorrent, BT, Comcast, D-Link, Disney, Google, HP, Microsoft, NBC, Netgear, Panasonic, Samsung, Sony, TiVo, XBox, YouTube

-

Comcast Announces Moves at CES; Still Missing Key Strategic Piece

In his CES keynote today, Comcast CEO Brian Roberts will outline several Comcast's initiatives (under the umbrella "Project Infinity") to stay competitive in the fast-changing video arena.

These include:

"Wideband"- New "wideband" broadband technology which allows much faster downloads (this is impressive, though was previously displayed at '07 National Cable Show). Wideband is aimed at blunting criticism that telcos' fiber networks have more capacity and faster speeds.

HD expansion - Plans for a 10-fold increase in the number of HD movies available in its VOD library to 3,000, with at least 6,000 total titles, including SD programming, eventually available. This is all meant to offset the widely held view that satellite and telco have surpassed cable in current HD offerings, a key value prop to millions of Americans now bringing home shiny new HD TV sets.

Fancast - Comcast's video portal will include 3,000 hours of streaming TV content, from NBC, Fox, CBS and others. These moves will help bring Fancast to parity with other syndicated partners of the networks which are themselves trying to proliferate their programs everywhere. Fancast will also allows remote scheduling of DVRs (both Comcast's and TiVo's), a feature that has been widely available at sites like TiVo.com and Yahoo for years now.

All of these actions are intended to help restore Comcast's reputation as the leading provider of entertainment programming, amid the swirl of changes that have enveloped the company. Despite its formidable size, Comcast is fighting competitive fires on virtually every front: fierce multichannel competition from satellite and telcos, rising expectations of HD content, consumer behavior shifts to broadband video consumption (premium and UGC) and place-shifting/time-shifting/device-shifting. The list goes on. Amid these changes, and with a slowing of the American economy, Wall Street has punished Comcast's stock price, cutting it in half in the last year.

While I applaud today's announcements, there is still one big strategic piece missing which Comcast has yet to comprehensively address: what are its plans to allow subscribers using its digital set-top boxes to seamlessly watch broadband video content as they do broadcast and cable programs?

As many of you know, I have been on a "broadband-to-the-TV" jag recently (see here, here and here) analyzing different options and their potential, or lack thereof. I continue to maintain that incumbents with boxes already in the home - mainly cable, satellite, telcos - are best-positioned to bridge the current divide between broadband and TV.

A breakthrough value proposition for Comcast would be allowing its subscribers to gain easy access on their TVs to YouTube, Break.com, Metacafe, NYTimes.com and all the others broadband sites that have surged in popularity. In theory, Comcast and other cable operators have always been about providing more video choices to subscribers. But the caveat has been those choices are only offered when Comcast makes a deal to carry these new channels. With broadband it's a wide open world. Any video provider - deal or no deal would gain access. This "openness" is a fundamental paradigm change for Comcast and other "walled garden" loyalists.

Surmounting this change to its business and cultural model are in fact Comcast's #1 strategic challenge. How to effectively respond to customers' broadband desires, while maintaining a robust economic and competitive model? When Brian Roberts, and others in the cable industry are finally ready to address the question of how they'll integrate broadband into their TV-based user experience, that will be a keynote well worth watching.

Categories: Broadcasters, Cable Networks, HD, Portals, Telcos

Topics: Comcast

-

Clueing in FCC Chairman Kevin Martin

Somebody needs to seriously clue in Kevin Martin, the chairman of the Federal Communications Commission, who has somehow gotten it into his head that America's cable TV industry needs to be burdened by all kinds of new regulations, despite the fact that competition is coming at the industry from every direction imaginable.

On the probability that you don't think too much about the FCC's actions, nor what they might mean to you, I have a reminder for you: when America's top communications regulator seeks to drive the industry that is America's #1 provider of broadband Internet service into a regulatory ditch, that's a problem for anyone who works in the media, entertainment, telecommunications and technology industries. Mr. Martin's cockeyed plans threaten to do this.

First, a quick recap. In the last several weeks Mr. Martin has sought to use hand-selected (and highly questionable) data to resurrect an arcane FCC prerogative known as the "70/70" rule. It is not worth reviewing what this rule is or whether or not it applies. What is important to know is that Mr. Martin has sought to use this rule to introduce regulations forcing cable companies to submit to federal arbitration to resolve carriage disputes with cable networks and to reduce the prices of certain leased access channels by upwards of 75%. Lingering in the background are further regulations, such as forcing "a la carte" unbundling of cable channels for unfettered consumer choice.

Last week wiser heads prevailed with the other FCC commissioners, many members of Congress and the White House intervening to check-mate Mr. Martin's plans. In fact, so perturbed by Mr. Martin's recent actions is the House Energy and Commerce Committee chairman John Dingell that has opened an investigation into Mr. Martin's handling of the FCC's affairs.

Now, in retreat, Mr. Martin has come up with a new regulation capping any one cable operator's U.S. coverage at 30%. This is particularly targeted at Comcast, which, with 27% coverage, is just a whisker away from hitting the proposed cap.

In criticizing Mr. Martin, let me make clear that I'm no cable apologist nor am I a regulatory libertarian, against all forms of government intervention. I worked in the cable industry from 1990-1998 and know the good, the bad and the ugly of the industry quite well. The government has intervened in the past to correct legitimate market failures caused by clear industry bad actors. But those days are past. Now the cable industry is fighting for its life against the triple threat of satellite, telco and broadband "over the top" competition.

So how is it possible that Mr. Martin has so completely "missed the memo" that America's consumer communications services - video, broadband Internet access and voice - are more competitive today than ever, and that re-regulation is completely wrong-headed? And that technology is enabling a wealth of new services that are causing traditionally distinct industries to compete against one another, with the ultimate winner being consumers? And that real, skilled, high-paying, American jobs which are tied to the innovative media, entertainment, technology and communications markets he oversees will certainly be adversely affected by these onerous new regulations he is proposing?

Of course, I cannot get inside Mr. Martin's head to explain his actions. All I can guess is that somehow he arrogantly believes that Washington's bureaucracy is better suited to sort out the hyper-competition and innovation sweeping these industries than are the free markets and myriad technologies being introduced. How profoundly incorrect that belief is. Last time I checked Mr. Martin's bio, he personally has exactly ZERO day-to-day business operating experience, so maybe someone can remind me what his particular expertise is in these matters? As if all this isn't enough, don't forget about how reckless it is for a regulator to mess around with one of the few remaining vibrant pockets of the American economy.

Mr. Martin's recent actions have shown him to be just another in a long line of seemingly intelligent, but ultimately clueless presidential appointees. Particularly in these tenuous economic times, America can ill-afford to have poor judgment in its chief policy-makers. For all of us who work in the media, entertainment, technology and telecom industries, let's hope the checks-and-balances system continues to work and Mr. Martin's misguided re-regulatory policies don't gain any traction.

Categories: Broadband ISPs, Cable Networks, Cable TV Operators, Regulation

Topics: Comcast, FCC, Kevin Martin

-

Net Neutrality in 2008? Let's Hope Not.

Network or "net" neutrality, a confusing legislative concept being promoted by large online and content players, may be the hottest broadband video topic in 2008, at least according to Jeff Richards, VP of VeriSign's Digital Content Services, who makes his case at his blog Demand Insights.

I had the pleasure of informally debating net neutrality's merits with Jeff (who's officially neutral on the subject by the way) over cocktails at a VeriSign customer event I just spoke at. Jeff is persuasive about why net neutrality is such a hot button issue, and that its resolution - one way or another - has broad repercussions across the technology, content and Internet industries.

First, a primer for those not familiar with net neutrality. To date the Internet has functioned as a level playing field of sorts. Anyone putting up a web site could be confident in the knowledge that broadband ISPs would neither favor nor disadvantage one player's access to users over another's.

Big online content and technology companies now want to codify this tradition in legislation commonly referred to as net neutrality. Big broadband ISPs (i.e. cable operators and telcos) regard this as needless regulatory meddling, a classic "solution in search of a problem" that would unnecessarily limit their future business dealings and influence their investment decisions.

Interest in net neutrality legislation has waxed and waned, as lobbyists for the pro-net neutrality side (content and technology firms) try to convince legislators that this really is an important issue for constituents and that this isn't just a "rich vs. richer" debate that should be left to the industry's participants to figure out, while anti-net neutrality lobbyists (cable and telco firms) argue the opposite point of view.

So what might precipitate the resurgence of interest in passing net neutrality legislation? In two words, broadband video.

As Jeff points out, the massive adoption of broadband video, which still disproportionately comes from illegal video file-sharing networks, is motivating ISPs to reevaluate current policies. Stoking this reevaluation is the awakening that the really big money is now being made by legitimate companies like Google (current market cap $200+ billion) which ride freely over ISPs' networks. As such, ISPs are wondering whether the balance of economics has gotten out of whack and if they can get a bigger share of the pie.

Some ISPs are now blocking or "shaping" certain types of traffic. The most recent example that came to light was Comcast, who the AP recently found is blocking BitTorrent's traffic in the Bay Area. Comcast's vague response, coupled with ill-thought out earlier remarks from telco executives about their own business intentions, have inflamed conspiracy theorists' worst fears about what kind of world could result absent immediate net neutrality action.

Yet for me, preemptive net neutrality legislation can only be justified if you buy into one or both of the following two assumptions.

First, that any new premium tier of service ISPs may want to sell to certain preferred providers (e.g. Google is search engine of choice, so its results somehow load faster) must, by definition, mean that some other provider is disadvantaged as a result. But this presupposes a zero-sum ISP network, which is not true. To enable a high quality-of-service ("QOS") tier for preferred partners does not technically necessitate a degrading other non-preferred services. Not to mention degrading other services would be a foolish, provocative thing for ISPs to do.

The second assumption is that regardless of whether ISPs create QOS-enabled premium tiers, they cannot be trusted not to block or harmfully shape traffic, whether it's legitimate or not. While there have been random acts of blocking by smaller ISPs, this does not seem to be a rampant problem right now. And it's important to distinguish between blocking legitimate vs. illegitimate traffic. For instance, when Comcast blocks illegitimate P2P file-sharing traffic then to me that's a good thing. It frees up network resources for the rest of us who are paying to use the network for legitimate purposes. I'm not going to cry for some 15 year-old kid who can't speedily download a pirated copy of the latest Hollywood thriller, nor should you.

While the pro-net neutrality folks obviously believe ISPs will be bad actors, to my mind, even if you make the above assumptions, this does not form the basis for preemptive net neutrality action now. Sure it's tempting to believe that cable and telco companies, still with plenty of monopolistic DNA flowing through their corporate veins, would indeed act unfairly, for now it is most appropriate to give them the benefit of the doubt.

Washington's laissez-faire attitude toward Internet regulation has been one of the key reasons for the Internet's continued innovation and growth. Attacking broadband video and the Internet, which are among the last few bastions of economic growth left in America is unwise, particularly given the fact that the "law of unintended consequences" is virtually synonymous with all recent telecommunications regulation. Preemptively impose network neutrality and who knows what the actual result will be.

So for now net neutrality regulation should stay on the backburner. When and if it's appropriate, it can be re-prioritized. Instead, I'd prefer keeping Washington's focus on cleaning up a separate, larger and far more pressing problem caused by another rush to preemptive government action (hint, it starts with an "I" and ends with a "Q").

Categories: Broadband ISPs, P2P, Regulation

Topics: BitTorrent, Comcast, VeriSign

-

Hulu Launches Private Beta

Not breaking news now, but Hulu lifted the veil of secrecy a bit today, releasing some screen shots and setting up a private beta (I'm trying to yank some strings to get access), in advance of a planned public launch early next year.

Hulu's been surrounded by a bunch of naysayers from the beginning, though much of the nay-ing has been based on little else than cheap shots about the name, delayed launch, etc. Things that in the grand scheme of things mean virtually nothing in my opinion and only serve to distract attention from the real question at hand: can Hulu become NBC and Fox's (for now) formula for success in the broadband video era?

Now it's time for Hulu to silence the rabble. Until I get my own hands on it, I'm going to reserve in-depth commentary. But at least several things that look intriguing:

- Shorter commercial breaks and overlays - Looks like the tension between user focus vs. advertiser focus is skewing toward users. A welcome change from traditional media thinking.

- Widespread distribution - I've been a big fan of this from the start. Deals with AOL, Yahoo, MySpace, Comcast, etc. ensures that Hulu content is widely available where users already are.

- More content deals - One of the knocks on Hulu was that neither CBS nor ABC joined up front. However, recent deals with Sony and MGM show Hulu continues to gain traction with other premium providers.

- Features - Beyond the standard range of embed, full-screen, send-to-friend features, it looks like there's an interesting "custom clip" capability to let users crop out scenes from favorite shows to pass along. This user control could enable massive new short form video inventory and could be a precursor to more interesting and creative user-generated mashups. All of this is highly monetizable.

More thoughts on Hulu to come.

Categories: Aggregators, Broadcasters, Strategy

Topics: ABC, AOL, Comcast, Disney, FOX, Hulu, Microsoft, MySpace, NBC, News Corp, Yahoo

-

Black Arrow Shoots for Multiplatform Ad Success

Black Arrow has an ambitious goal of managing and serving ads across broadband video, DVR and VOD platforms. With audience fragmentation causing chaos in the advertising world, such a solution, when fully implemented, would have enormous value to content companies and service providers (cable, satellite, telco).

Black Arrow has an ambitious goal of managing and serving ads across broadband video, DVR and VOD platforms. With audience fragmentation causing chaos in the advertising world, such a solution, when fully implemented, would have enormous value to content companies and service providers (cable, satellite, telco).Black Arrow has been around for a while but went under the radar for the past few months. Now it's re-emerging, with new CEO Dean Denhart installed about 6 months ago.

Dean briefed me last week on news the company announced today, which included closing a $12M B round from existing investors Comcast, Cisco, Intel, Mayfield and Polaris and officially launching their ad platform.

The company is trying to differentiate itself from many others serving ads in the broadband video space by tackling the thorny problem of also inserting in both the DVR and VOD environments. DVR insertion today is non-existent and for VOD it's not scalable. To succeed, the company will need to integrate its servers with the service providers, which is no easy feat. As many of you know, the rap on cable operators - and I've experienced this first-hand - is that selling into them wears out early-stage companies, using up precious time and capital in long drawn-out testing, selling and negotiation cycles.

If Black Arrow survives this process and proliferates its gear into headends, it will have a formidable competitive advantage against competitors. And on the encouraging side, in the cable world at least, a nascent set of standards dubbed "DVS 629" governing digital ad insertion is now being worked on. Black Arrow is following these closely. Dean explained that the company has proven in its technology and in 2008 it will be pursuing field trials and initial rollouts with major operators. Certainly having Comcast as a lead investor can't hurt its chances.

Black Arrow's real appeal to content companies will only begin when it has significant deployments. Dean explained that while the cable sell-in process continues to unfold, it will follow a parallel track of managing ads for broadband, with the longer-term value prop of multi-platform support. And it's taking a wait-and-see approach on which business model to use to fund the capex for proliferating its servers. An analogous and interesting approach is the one Akamai has mastered - i.e. not charging ISPs. Instead it positions its gear contributing to top-line growth and opex reductions. This strategy has been a massive success for Akamai, helping it achieve widespread deployments and a huge entry barrier for competitors.

I really like this company's vision; however achieving it in full is going to take tenacity, patient and deep-pocketed investors and a few good breaks.

Categories: Advertising, Cable TV Operators, Deals & Financings, Startups

Topics: Black Arrow, Cisco, Comcast, Intel, Mayfield, Polaris

-

I Got My Official Comcast-TiVo Beta Trial Invite This Week

This week I heard from the folks at Comcast who are running the upcoming beta trial with TiVo. I'm officially on the list and should be getting a box soon. Hooray.

This week I heard from the folks at Comcast who are running the upcoming beta trial with TiVo. I'm officially on the list and should be getting a box soon. Hooray.As many of you are aware, Comcast has been on the cusp of kicking off this trial for some time now, which will let real users experience the joys of TiVo software running inside a Comcast digital set-top box. This will mark a milestone for Comcast in delivering a better user experience than the generic DVR feature that it and other cable operators rolled out a couple of years ago.

After hosting Jeff Klugman, TiVo's Senior VP, GM of its Service Provider and Advertising Engineering Division for a "fireside chat" at a cable industry conference last July, I became very bullish on the opportunity for TiVo to transform itself through these cable deals into a software and services powerhouse. In other words, long-term getting out of the high-cost, low-margin consumer device business.

Running a successful trial with Comcast is all-important to TiVo and they've been working for 2 years on this integration. Success will likely mean wide rollouts with Comcast, followed by #3 operator Cox (with whom TiVo already has a deal), and then others no doubt to follow. I'll be keeping you posted on my experience when I get the box. If it works as advertised it's going to be a killer device.

Categories: Cable TV Operators, Devices, Partnerships

-

TiVo: The Comeback Kid

If some kind of ratio could be calculated to measure consumers’ love for a product in relation to that product’s actual market success, TiVo’s score would undoubtedly top the list. Few products have ever achieved such undying fervor from their owners as have TiVo’s. Yet at the same time, few companies have underachieved their market potential as dramatically as has TiVo since its inception ten years ago.Despite my own love for my TiVo Series 2 box, not that long ago when I was asked by a friend what the future held in store for TiVo, I responded that with deep regret, I was hard-pressed to envision a happy ending for this plucky little company.

However, that was before last week when I had the opportunity to spend an evening with Jeff Klugman, TiVo’s Senior VP, General Manager of its Service Provider and Advertising Engineering Division and David Sandford, TiVo’s Vice President, Marketing & Product Management, Service Provider and Media & Advertising Divisions.

In addition to this time together, I also saw a presentation and demo of TiVo’s new integrated cable TV digital set-top box offering and also hosted them for a "fireside chat." All of this happened at a CTAM of New England-organized session at a cable TV industry conference in Newport, R.I.

Much as I thought I’d never say this, hear me now: TiVo is going to be the Comeback Kid. And it’s completely clear why. Read on to understand my logic.

The Old TiVo: Making Buyers "Crawl Across Broken Glass" to Enjoy the ProductAn immutable law of TiVo ownership has always existed: once you get one set up, you will fall in love with it. With its simple program recording process, tantalizing ad-skipping capability, intuitive user interface and more recently, its endless series of innovations (home networking readiness, remote scheduling, TiVoToGo portability, WishLists, Amazon Unbox downloads, Universal Swivel Search, TiVoCast broadband video channels, etc. etc.) TiVo is a blockbuster consumer value proposition.Despite all this, TiVo has always suffered from a problem that Jeff Klugman astutely describes: the company has essentially made prospective buyers "crawl across broken glass" to get from purchase decision to completed setup. Such a harsh assessment is well-earned. Consider: first TiVo required the user to find their way to a retail store (or go online) to buy the TiVo box, further cluttering the precious shelf space beneath the TV set. Then it required the buyer to select a monthly service plan that was on top of what the consumer already paid for cable TV or satellite service (to add insult to injury, TiVo did away with its $300 "Lifetime"plan a while ago). This change meant that a consumer’s choice to have a one-time bloodletting was replaced with a requirement that TiVo stick its probe into your credit card for as long as you wished to continue getting the service.

But that wasn’t all. Get the TiVo box home and you faced the oh-so-pleasurable task of contorting your body to access the back of your TV, while fending off that embarrassing swarm of dust bunnies lurking back there, all the while juggling a flashlight to figure out how TiVo’s gaggle of wires should marry up to your existing gaggle of wires. Your persistent fear was that not only might you end up not actually getting TiVo to work, you might find that you irreversibly tampered with your existing set-up, reducing your TV to a snow-and-static haze. Factor in your family members glowering at you while you puzzled through this process and it’s a pretty daunting and ugly picture.

This picture became even uglier when cable and satellite operators introduced a viable alternative to TiVo several years ago: simply pay a few extra bucks to them and you can have DVR features (ok, a sucky imitation of TiVo to be sure) built right into your new digital set-top box. So no contorting, fretting, glowering and of course, no extra box to buy and install.

TiVo’s Picture Darkens FurtherGiven this rigmarole, it’s no surprise that, despite the love fest people have for TiVo, it has only managed to sell a few million standalone boxes over the years, a relatively minor market impact. In fact, by far the majority of its market presence is through a deal with DirectTV, which contributes several million TiVo-enabled set-top boxes deployed. However, growth with DirectTV is over, with the company instead choosing to use technology from former sister company NDS instead.The sudden popularity of high definition TV brought yet another huge challenge for TiVo. Eventually, as consumers fully understand HD, they will all want an HD set-top box, capable of delivering real HD programming. Right on the heals of HD, people will want DVR features - of course HD-capable. Cable and satellite operators figured this out a few years ago and stepped up by offering their HD-DVR integrated set-top boxes for just a few extra dollars per month.

But TiVo only recently managed to release its own standalone HD-capable box, the "Series 3." And while the box is a marvel of product design, it weighed in with an $800 price tag, a price completely discordant for consumers whose expectations have been set by the fact that DVD players can now be had for as little as $13 at their local Wal-Mart. Coincidentally, it’s worth noting that just today TiVo announced a $300 version of the Series 3, which, while helping relieve upfront sticker shock, still requires the additional monthly service fees. And also the contorting, puzzling and glowering aspects of the installation process.

And Now for the Silver Lining in this StoryBy now you’re probably wondering how all of this doom-and-gloom is going to give way to the "Comeback Kid" scenario.In fact, the secret to TiVo’s success is, and has always been, jettisoning its hardware business model and becoming a software company. In other words, stop making boxes and instead just license the TiVo software to others whose boxes stand a better chance of being accepted by consumers (i.e. video providers). This was the vision from the start. I recalled reading a trenchant New York Times magazine piece that Michael Lewis (of Liar’s Poker and Moneyball fame) wrote 7 summers ago in August, 2000 on TiVo and Replay, its competitor at the time. I was able to dredge it up (thanks, Google) and in it, Jim Barton, TiVo’s co-founder, and current CTO plainly put it, "We’ll know we’ve succeeded when the TiVo box vanishes."

With TiVo’s promising, but ultimately unfulfilling deal with DirectTV unraveling, the company’s real potential to deliver on its vision lay with making deals with the cable industry. For a variety of reasons not worth recounting here, those deals proved elusive until early 2005 when TiVo struck a deal with Comcast. Things started looking even better for this game plan when the TiVo appointed Tom Rogers, who has significant cable bona fides, as CEO in mid-2005.

Flash forward 2 years later and it is looking increasingly likely that TiVo is on the cusp of executing its original strategy, positioning itself, at long last, for its moment in the sun.

TiVo + the Cable Industry, A Match Made in ARPU HeavenAs summer turns to fall, Comcast, by far the largest cable operator in the US and Cox, the third largest, are planning their initial rollouts of TiVo-enabled HD set-top boxes.After all these years, a more perfect time for TiVo and the cable industry to get together can scarcely be imagined. The incentives for these deals to succeed are very strong all around.

The cable industry is fighting hard to convince consumers to resist switching to Verizon and AT&T in the communities in which these telcos have rolled out their wizzy new video services. With telcos offering stiff price competition, ARPU (average revenue per unit) growth can only happen through new services, not price increases. Further, Comcast in particular has been working overtime to convince Wall Street that Video-on-Demand is its killer competitive advantage to satellite even while it struggles with its poorly-designed user interfaces which serve to impede, not assist, its subscribers’ discovery of valuable VOD programming.

Enter TiVo. TiVo offers Comcast/Cox/the cable industry one of the best-known and best-loved consumer brands with which to align itself on a de-facto exclusive basis. As mentioned, DirectTV’s deal is over. EchoStar’s relationship with TiVo is toxic due to mammoth patent litigation between the two companies. Verizon and AT&T barely have the resources to get their networks up and running much less take on the challenge of how to integrate their set-top boxes with TiVo software.

Meanwhile, the cable industry continues to grapple with how to get more consumers to sign on for digital cable service. Years after its introduction, digital still remains a sketchy value proposition for many. But TiVo gives cable operators a powerful feature to goose demand. Further, since Jeff showed how elegantly TiVo has incorporated VOD navigation and recording into its UI, integrated TiVo service also offers the promise of addressing that cable operators’ challenge in that area.

Last, but not least, on the assumption that TiVo service will carry an upsell charge of around $3-4 per month to the consumer (which are completely my estimates, with nothing having been disclosed by TiVo or its partners at this point), and assuming 2/3 of that goes to the cable operator, TiVo provides tantalizingly high-margin new ARPU growth for cable operators. Those high margins are made possible through the magic of OCAP, the cable industry’s new standard for remotely downloading applications like TiVo to tens of millions of currently-deployed set-tops (i.e. no expensive truck rolls).

That Sweet Sound of Ka-Ching, Ka-ChingTo help understand the revenue and margin potential of the cable deals for TiVo, consider the following:Pick your favorite analyst’s forecast for DVR growth. Forrester, for example believes that by 2011 there will be 65 million DVR homes, up from somewhere around 15-17 million today. So net adds of around 50 million homes. Comcast and Cox together pass about 58 million or 53% of all American homes. So their proportionate share of those 50 million DVR net adds should be at least 26 million. If they market the service right, it’s probably fair to assume that over time, at least 80% of DVR users are going to prefer the TiVo solution to cable’s crummy homegrown DVR alternative (if this option even survives). If so, then these deals’ potential is about 21 million homes taking the TiVo cable service by 2011.

Again, say the TiVo service costs an incremental $3 per month and then assume TiVo keeps a $1 of that, which is my approximation for the combination of its per sub and technology licensing fees. So, eventually 21 million new TiVo homes x $1 month x 12 months. Just from Comcast and Cox that would eventually total $252 million of annual revenue for TiVo. Now factor in when all the other cable operators smell the coffee and abandon their homegrown DVR solutions in favor of TiVo. And then of course it’s inevitable that TiVo will sign up Verizon and AT&T. However in those deals TiVo should be able to negotiate to keep maybe half the monthly fee instead of just a third as they did with the cable crowd (hey, it’ll be a proven service, plus the telcos will be playing catch-up, as usual).

To put all of this in context, for the fiscal year ending 1/31/07, TiVo’s revenues were $259 million, so if the Comcast and Cox deals alone succeed to even a fraction of their fullest potential, they should still have a major impact on the company’s financials. And bear in mind that if the cable strategy succeeds, then along the way TiVo’s retail hardware business would have been euthanized, erasing all that low margin box revenue. What would be left is a high-margin software licensing and services powerhouse, ready to go international, add portable applications and generate all kinds of new features, such ramping up its already solid broadband programming lineup.

But perhaps most important, with TiVo able to track the viewing behavior of all of those millions of homes, its long-held vision of building out an ad-based revenue business based on precise user viewing suddenly seems attainable. Of course it’ll be a little cheeky of TiVo to be pitching agencies and advertisers on these ad services after TiVo all but wrecked their traditional model with its ad-skipping features. But what choice will these folks really have if they want to succeed? And these meetings are already happening, and according to Jeff, who oversees all this, it sounds like all is forgiven and good progress is already being made.

What’s the Catch?The catch here is that initially TiVo is almost entirely dependent on Comcast and Cox putting enough marketing muscle behind this new service and executing it properly. So will Comcast and Cox do this? Though it’s way too early to tell, given all of the aforementioned incentives, there’s ample reason to believe that both will. For Comcast alone, which has borne the brunt of two years of arduous technical integration work with TiVo, failure to follow through with strong marketing would be a huge and embarrassing blunder. So I’m betting these savvy cable guys will get the marketing part right (if you’re really interested in how, keep scrolling to see the below Addendum for a couple of sample marketing scenarios).And if they do, then you heard it here first— TiVo is well-poised to become The Comeback Kid.

ADDENDUM: 2 MARKETING SCENARIOS FOR COMCAST

To make TiVo’s potential more tangible, consider the following 2 scenarios. In both cases you just bought a 42 inch LCD or plasma TV. Of course you now need an HD-capable set-top box. You call Comcast to order one and here’s what should happen:

Scenario 1: You own or have owned a TiVo Series 1 or 2 box

You’re told that an HD set-top will run you $5.00 more per month than your current box. Then you say you’re interested in DVR capability. "Ah," the Comcast rep says, "have you ever owned a TiVo?". You say "Yes." "Well", she continues, "did you know that you can now get the same (mostly) awesome TiVo service - including the familiar user interface, remote control and blooping sounds as you program the box AND have all Video-on-Demand programming expertly integrated into the service, only from Comcast? It is one of our most popular services, and I can offer it to you today for just another $8 more per month than the HD set-top box you want." You say, "let me get this straight, I’m already used to paying $13/month for my TiVo Series 2 service, so instead of paying that, I would pay $8 per month and get virtually all the same benefits of TiVo, but don’t have to go out and buy another TiVo box? And this isn’t the crummy DVR service I saw at my neighbor’s house that I know you also offer, right?" "No sir, it’s TiVo." "Any other sneaky upfront charges?" "No." "Any disconnect charges if I want to drop it?" "No." "Am I missing something here?" "No." "WOW, sign me up - what a great offer. Thanks Comcast."

Scenario 2: You’ve never owned a TiVo box, but you have some familiarity with the product because any number of friends, neighbors, relatives and co-workers have been bragging to you for years that it’s the greatest thing since sliced bread.

You’re told that an HD set-top will run you $5.00 more per month than your current box. Then you say, "I’m kind of interested in this whole DVR thing everyone keeps talking about." After the Comcast rep verifies you’ve never actually owned a TiVo, but that you’re sort of familiar with what it does, she says, "Well, Comcast has a very special offer for you. TiVo DVR service has become one of our most popular services and we think if you experience it for yourself, you’ll see why. So I’d like to offer you 90 days of free TiVo service. If you don’t like it, simply call us at any time and we’ll remotely remove it from your box. That means you don’t need to wait at home for a technician to disable TiVo service for you." You ask what it will cost per month and upon hearing the answer ($8 more per month than the HD box base rate) you make a mental note to ask your friends, neighbors, relatives how much they pay, to see what kind of deal you’re getting (later they’ll confirm it’s the same as they’re currently paying for their Series 1 or 2 monthly plans). You see no downside to trying it, so you do. After you and your family use TiVo for approximately 3 days, you all fall in love with it and wonder how you could have ever lived without it. You call Comcast to say thanks.

Categories: Cable TV Operators, Devices, Partnerships

-

Broadband Video Isn't Competition for Cable Says My CTAM Panel

Today I moderated a spirited discussion panel at CTAM NY’s annual Blue Ribbon Breakfast at Gotham Hall in NYC. The title was "Over the Top TV....Can Broadband Video Be Cable's Newest Opportunity?" We had an amazing group of panelists (click here to see list and listen to podcast) and with 450+ attendees a packed house as well.

A key question we dug into was whether and to what extent cable’s traditional (and highly successful) paid subscription model will be impaired by the rise of broadband video usage. Try as I did to see if any of the panelists believe that it will, none would admit to it. The reasons given included, "some form of a paid model will always exist but will never succumb entirely to a free, ad-supported model" to "cable networks won’t push broadband video distribution of their programs so hard as to upset the current model of receiving affiliate fees from cable operators", to "the low probability that inexpensive PC-to-TV bridge devices will proliferate any time soon" to "viewers have shown that they want a selection of channels to browse."

While I think each of these answers is quite legitimate, my point of view is that we are in the early days of an fundamental transformation in the video (and indeed the media more generally) business that will eventually (though of course who knows when and to what eventual degree) see most, if not all programming get unbundled into a fully on-demand paradigm.

I believe the ultimate answer to how cannibalistic broadband is toward cable ultimately turns on whether consumers believe it’s a "zero sum" game, meaning they choose between EITHER accessing programs via a VOD or DVR offering only available if they’ve bought into a monthly multi-channel video subscription (that’s to say the way the world works today) OR if they opt out of that subscription offering and INSTEAD choose to buy these programs a la carte, or receive them free, courtesy of a highly targeted ad model. The opt out option would of course be available through open broadband video distribution.

All trends point to the latter ultimately prevailing. While cable operators are well-positioned to shift their models to exploit this behavior if they act aggressively, they are also vulnerable to it if they don’t. The most important driver of the "opt out" scenario is that for an increasingly larger portion of our society, their behavior and expectations are formed by the Internet. And the ‘net is a completely personalizable and on demand medium. Especially for most online media, it is also mainly free, or paid on a fully a la carte basis (e.g. iTunes). Users’ expectations are through the roof and only getting higher. As broadband proliferates they will bring these same expectations to their decision-making.

Is it really realistic to believe that in 5 years when today’s MySpace/Facebook/YouTube/iTunes crazed 16 year old kid goes to set up his/her first apartment, s/he is going to embrace the notion of subscribing to a hundred channel package just so s/he can watch a handful of programs on demand? And of course, the ‘net’s behavior change isn’t confined to kids, it’s pervasive across all age groups.

Cable operators have an outstanding opportunity to capitalize on these macro behavioral trends. But doing so will require cable operators to make a significant and risky departure from their traditional subscription-based business models. It’s a classic incumbent’s dilemma. It will be interesting to see if they can do so.

Categories: Aggregators, Cable Networks, Cable TV Operators, Events, Indie Video

Topics: Comcast, Cox, CTAM NY, Discovery, Google, Next New Networks

-

CTAM NY Blue Ribbon Breakfast is On Tap

I'm really looking forward to moderating the CTAM NY chapter's annual Blue Ribbon Breakfast on Wednesday morning at Gotham Hall. The session is entitled, Over the Top TV....Can Broadband Video Be Cable's Newest Opportunity?"

I'm really looking forward to moderating the CTAM NY chapter's annual Blue Ribbon Breakfast on Wednesday morning at Gotham Hall. The session is entitled, Over the Top TV....Can Broadband Video Be Cable's Newest Opportunity?"We have a world-class group of panelists:

- Bruce Campbell, President, Digital Media and Business Development, Discovery Communications

- Dallas Clement, Senior Vice President, Strategy & Development, Cox Communications

- David Eun, Vice President, Content Partnerships, Google

- Herb Scannell, CEO & Co-Founder, Next New Networks

- Matt Strauss, Senior Vice President, New Media, Comcast

The event has been sold out for 2 weeks and CTAM just figured out a way to shoehorn in another 25 people from the waitlist, bringing the overall attendance to 460+.

It's going to be an amazing event. The cable industry – both operators and programmers – are right in the middle of the whole broadband video revolution. Their actions will have a big impact on the course and pace of the industry's future.

CTAM is recording the event to podcast it, and I'll be sharing my observations in this space as well.

Categories: Events

Topics: Comcast, Cox, CTAM NY, Discovery, Events, Google, Next New Networks

-

5 Reasons Why Comcast Should Take Out Yahoo. Now.

Terry Semel's departure as CEO of Yahoo has again raised speculation that Yahoo is acquisition bait. Of course this rumor's been flying for ages. So here's my point of view: Comcast should acquire Yahoo. And they should do it now.