-

April '09 Recap - Innovation is Alive and Well in the Broadband Video Space

Looking over last month's posts with an eye for 2-3 themes to extract for my recap post today, I was instead struck by one overarching theme: innovation is alive and well in the broadband video space. Other sectors of the economy may have ground to a halt in the current recession, but whether it's new technologies, new service models or new approaches by traditional media companies, the pace of innovation in all things related to broadband video seems only to be accelerating.

Here are some of the examples from last month's posts:

New technologies

- SundaySky - a new approach to dynamically generate videos out of web site content

- HD Cloud - cloud-based encoding and transcoding plus 3rd party syndication

- Market7 - web-based platform for collaboratively creating and producing video

- FreeWheel - ad management/distribution company raises another $12M

New service models

- Sezmi - next-gen video service provider aiming to replace cable/satellite/telco

- TurnHere - distributed video production services for the corporate market

- Babelgum - premium-quality content destination for independent producers

- YuMe Mindshare iGRP - new measurement unit to compare on-air and online ad performance

- YouTube-Disney - short-form promotional deal

New approaches by traditional media companies

- Disney-Hulu - Exclusive 3rd party online distribution for established broadcast network

- Cable networks launching webisodes - online initiatives to attract and retain new online audiences

- New York magazine video re-launch - emphasis on curating best-of-the web videos with brand

- WWE Smashup - fan-submitted video mashup content driving awareness of on-air special

Now granted I have an eye out for broadband innovations so this list is somewhat self-serving. But remember that for every item above I was probably pitched on 2-3 others that I didn't write about due to time limitations. Some of these other items may have been picked up by other news outlets and captured in the news aggregation side of VideoNuze, while plenty of them likely received little attention.

My point is that throughout the whole broadband video ecosystem there is a vibrant sense of entrepreneurialism that is slowly but surely remaking the traditional video landscape. To be sure, not all of this stuff is going to work out; either business models will be faulty, technologies won't deliver as promised or consumers will reject what they're being offered. Nonetheless, from my vantage point, the wheels of innovation continue to spin faster. That makes it a very exciting time to be part of the industry.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Technology

Topics: Babelgum, Disney, FreeWheel, HD Cloud, Hulu, Market7, New York, SezMi, SundaySky, TurnHere, WWE, YouTube, YuMe

-

YouTube Continues Its March Up the Content Quality Ladder

Late yesterday YouTube announced "a new destination for TV shows and an improved destination for movies," moves that continue the site's evolution from its UGC/video sharing roots to an aggregator of premium-quality video.

The reality is that this evolution has been underway for some time now, and I expect it will only continue. Two weeks ago in "6 Reasons Why the Disney-YouTube Deal Matters" I explained again why, as the 8,000 pound gorilla of the online video market, YouTube is in an excellent position to partner with premium content providers. In a media landscape marked by massive audience fragmentation, the online destination (YouTube) that accounts for 40-50% of all streams and is 15 times as big as the #2 destination (Hulu) is quite simply a must-have promotion and distribution partner.

The new destinations address what has been an ongoing Achilles' heel for the site - enabling users to easily find premium video "needles" in YouTube's user-generated "haystack." YouTube's UI weaknesses for

premium video have been highlighted by the gold-plated user experience Hulu - and more recently TV.com and Sling.com - have brought to market. The sites have quickly gained passionate fans, and at least in the case of Hulu, significant viewership.

premium video have been highlighted by the gold-plated user experience Hulu - and more recently TV.com and Sling.com - have brought to market. The sites have quickly gained passionate fans, and at least in the case of Hulu, significant viewership. From a design perspective, while there's nothing I would call truly breakthrough about YouTube's premium destinations, they are still a step forward and a solid start. For users solely interested in premium content, they help organize things nicely. There's a decent selection of content, including titles from deals with MGM, BBC, CBS, Crackle and Lionsgate and lots of other partners, which will no doubt continue to grow.

Possibly more important though, is that for content providers they show how YouTube is serious about addressing their needs for clean, well-lit spaces. Premium content providers want the benefits of being in the massive YouTube site, but without the risk of their brands showing up too close to scruffy UGC material. Being clustered with other premium content is a must.

YouTube's concurrent beta launch of Google TV Ads Online, which allows targeted instream ads, is another positive for premium content providers. Beyond YouTube's massive traffic, Google's potent monetization capabilities are the other reason I've been so bullish on YouTube's prospects for premium content. As I wrote on Monday, with increased DVR penetration driving rampant ad-skipping, broadcast and cable's traditional ad model is looking more and more defunct. Online video ads offer a lot of promise as an even higher value ad medium, but much of it is still unproven. Having large players like Google and YouTube involved is significant for showing online video advertising's true upside.

One last take on this is how YouTube continues to position itself in the "over-the-top" sweepstakes, where multiple competitors are vying to be viewed as bona fide substitutes for cable/satellite/telco subscribers itching to cut the cord. I remain skeptical that the trickle of cord-cutters is going to turn into a gusher any time soon, but I will say that with its move up the content ladder, YouTube continues to burnish its standing as a must-have partner for any convergence device-maker looking to make over-the-top inroads (e.g. Roku, Vudu, AppleTV, etc.). YouTube is the most-recognized online video brand, the most-heavily trafficked, and increasingly a credible alternative to premium aggregators like Hulu and others.

For everyone in the online video ecosystem, YouTube continues to be a key player to watch.

What do you think? Post a comment now.

Categories: Aggregators, Broadcasters, Cable Networks, FIlms

Topics: Disney, Google, Hulu, Sling, TV.com, YouTube

-

VideoNuze Report Podcast #12 - April 3, 2009

Below is the 12th edition of the VideoNuze Report podcast, for April 3, 2009.

After a week off, Daisy Whitney and I are back. This week we discuss new comScore data Daisy learned about while attending the OMMA Video conference, which supports the idea of TV ad spending shifting from TV to broadband video. Then we dig deeper into the significance of Disney's deal to bring promotional clips to YouTube, which the companies announced earlier this week. More detail on the deal is also in this post I wrote on Tuesday.

Click the play button to listen to the podcast (13 minutes, 49 seconds):

Click here for previous podcasts

The VideoNuze Report is available in iTunes...subscribe today!

Categories: Podcasts

Topics: comScore, Disney, Podcast, YouTube

-

YouTube to Merge with Hulu, Entity to be Renamed Either "YouLu" or "HuTube"

In a surprising turn-of-events, VideoNuze has learned that Google will acquire Hulu and merge it with YouTube. The resulting entity will be named either 'YouLu' or 'HuTube.' The merger brings together the two most-trafficked video sites into a powerful new player.

In an interesting twist, the final acquisition price has not yet been determined. Instead, the price will be based on a new algorithm Google is creating to accurately measure just how effective Hulu is at turning its

users' brains into 'creamy giggity-goo' as Seth MacFarlane asserts it will in the latest of Hulu's alien-inspired ads. The algorithm will actually be able to count how many more of users' brain cells die as a result of watching shows on Hulu beyond the cells that already died due to regular on-air network TV viewership.

users' brains into 'creamy giggity-goo' as Seth MacFarlane asserts it will in the latest of Hulu's alien-inspired ads. The algorithm will actually be able to count how many more of users' brain cells die as a result of watching shows on Hulu beyond the cells that already died due to regular on-air network TV viewership. It turns out that Hulu's positioning as an 'evil plot to destroy the world' was considered highly synergistic with Google's longstanding mantra to 'do no evil.' Google CEO Eric Schmidt revealed that the company decided some time ago to move beyond its good-guy image, saying, "Look, we got a lot of mileage out of that 'doing no evil' malarkey, but it's time to get real. We're an avaricious multi-billion company now, and all these wacky tree-hugging green initiatives our engineers keep dreaming up can't hide that." He added, "We really admire the traction Hulu is getting by turning 'evil' into a virtue and want to tap into that concept further. Those Hollywood guys beat us hands-down when it comes to creativity."

For its part, Hulu's owners' decision to merge with YouTube, for a price not yet quantifiable, can only be seen as waiving the white flag of surrender. In an email exchange between Jeff Zucker, NBCU's CEO and Peter Chernin, Fox's former CEO (who made the original Hulu deal), obtained by VideoNuze, Zucker's frustration with Hulu's distant second place status is palpable. Among other things he says, "I thought we had dumbed down our shows as much as possible, but YouTube has clearly tapped into audiences' insatiable appetite for the inane. Who would have thought that skateboard-riding cats crashing into walls would have more audience appeal than our $2 million/episode scripted dramas. There really is no accounting for taste."

In response Chernin is quoted as saying, "Rupert always thought Hulu was a small potatoes deal, not really

capable of losing a large, exciting amount of money. On the other hand, YouTube has been a gigantic black hole for Google, so the opportunity to join forces and achieve scale at losing money together was just incredibly compelling." He added, "Plus, you have to remember, Rupert's heart is really in newspapers. He continues to think this whole Internet thing is a fad that will eventually blow over, with people returning to newspapers as their trusted source of news and propaganda. So the company is logically positioning itself to have sizable video losses to offset expected massive gains in newspaper profitability."

capable of losing a large, exciting amount of money. On the other hand, YouTube has been a gigantic black hole for Google, so the opportunity to join forces and achieve scale at losing money together was just incredibly compelling." He added, "Plus, you have to remember, Rupert's heart is really in newspapers. He continues to think this whole Internet thing is a fad that will eventually blow over, with people returning to newspapers as their trusted source of news and propaganda. So the company is logically positioning itself to have sizable video losses to offset expected massive gains in newspaper profitability."Meanwhile, in a meeting with employees, Hulu CEO Jason Kilar reportedly sought to put a positive spin on the merger. Employees who have Twittered the meeting say that to pump up employee enthusiasm he re-told stories of how much fun it was to originally come up with the name 'Hulu,' reportedly saying, "Look how much mileage we got of one ridiculous-sounding made-up name, just imagine the branding possibilities of the even more-ridiculous sounding names YouLu or HuTube..." Negotiations are already underway with the Chinese portal and domain parking company that own the respective URLs.

The merger left many industry analysts scratching their heads. Representative of their reaction, VideoNuze's Will Richmond said, "Geez, I never thought we'd see a more nonsensical media merger than the one between Time Warner and AOL, but I think this YouLu/HuTube thing might just be it. Let's hope it's not for real, and is just some kind of April Fool's Day joke cooked up by an industry analyst to provide some once-per-year, cheap laughs."

Categories: Aggregators, Deals & Financings

Topics: FOX, Hulu, NBCU, YouTube

-

6 Reasons Why the Disney-YouTube Deal Matters

Late yesterday's announcement that Disney-ABC and ESPN would launch a number of ad-supported channels focused on short-form content was yet another meaningful step in broadband video's maturation process. Here are 6 reasons why I think the deal matters:

1. It validates YouTube as a must-have promotional and distribution partner

For many content providers it's long since become standard practice to distribute clips, and often full-length content, on YouTube. Yet aside from CBS, no broadcast TV network has seriously leveraged YouTube.

That's been a key missed opportunity, as YouTube is simply too big to ignore. It's not just that YouTube notched 100M unique viewers in Feb. '09 according to comScore, it's that the site has achieved dramatically more market share momentum over the past 2 years than anyone else, increasing from 16.2% of all streams to 41% of all streams.

That's been a key missed opportunity, as YouTube is simply too big to ignore. It's not just that YouTube notched 100M unique viewers in Feb. '09 according to comScore, it's that the site has achieved dramatically more market share momentum over the past 2 years than anyone else, increasing from 16.2% of all streams to 41% of all streams. Increasingly, YouTube is not the 800 pound gorilla of the broadband video market; it's the 8,000 pound gorilla. Disney has acknowledged what has long been tacitly understood - as a video content provider, it's impossible to succeed fully without a YouTube relationship.

2. It creates a path for full-length Disney-ABC programming to appear on YouTube and elsewhere

While this deal only contemplates short-form video, and more than likely, mostly promotional clips, it almost certainly creates a path for full-length episodes to appear as well, as the partners build trust in each other and learn how to monetize. Full-length content is most likely to come from ABC, not ESPN (the release

pointedly states no long-form content from ESPN's linear networks is included) as part of a newly expanded distribution approach.

pointedly states no long-form content from ESPN's linear networks is included) as part of a newly expanded distribution approach.For YouTube, which has been aggressively evolving from its UGC roots in its quest to generate revenues, the current clip deal alone is a big win; gaining distribution rights to full-length programs would be an even more significant step. Underscoring YouTube's flexibility, the current deal allows ESPN's player to be embedded, and for Disney-ABC to retain ad sales. YouTube's reported redesign, which places more emphasis on premium content, is yet another way it is getting its house in order for premium content deals.

3. It opens up a new opportunity for original short-form video to flourish

When you think about broadcast TV networks and studios, you immediately think of conventional long-form content. Yet all of these companies have been producing short-form content that either augments their broadcast programs, or is originally produced for broadband, as Disney's own Stage 9 is pursuing. The levels of success of this content have been all over the board.

With YouTube as a formal partner, Disney can aggressively leverage it as its primary distribution platform, gaining more direct access to this vast audience. Facing unremitting market pressures on many fronts, broadcast TV networks themselves need to reinvent their business models. Short-form original content married to strong distribution from YouTube would be a whole new strategic opportunity.

4. It puts pressure on Hulu and other aggregators

It's hard not to see YouTube's gain as Hulu's - and other aggregators' - loss. For sure nothing's exclusive here, and as PaidContent has reported, discussions about Disney distributing full-length programs on Hulu (as well as YouTube) are also underway. But the Disney deal underscores something important that differentiates YouTube from Hulu: YouTube is both a massive promotional vehicle and a potential long-form distributor, while Hulu is really only the latter.

YouTube's benefit derives from its first-mover status. Hulu has done a tremendous job building traffic and credibility in its short life, but it is still distant to YouTube in terms of reach. I continue to believe it is far easier for YouTube to evolve from its UGC roots to become also become a premium outlet than it is for Hulu - or anyone else - to ever compete with YouTube's reach.

5. It raises threat warning to incumbent service providers by another notch

It's also hard not to see the Disney deal moving YouTube's threat level to incumbent video service providers (cable/satellite/telco) up another notch. We discussed YouTube's importance to these companies at the Broadband Video Leadership Evening 2 weeks ago (video here), and I thought the panelists generally did not give YouTube much credit as it deserves.

I continue to believe that of all the various "over-the-top" threats to the current world-order, YouTube is the most meaningful ad-supported one. It has massive audience, a potent monetization engine in Google's AdWords, and with the Disney deal, increased credibility with premium content providers. Especially for younger audiences, the YouTube brand means a lot more than any incumbent service provider's. If I were at Comcast, Verizon or DirecTV, I'd be keeping very close tabs on YouTube's evolution.

6. It exposes the absurdity of the ongoing Viacom-Google litigation

Two weeks ago at the Media Summit I listened to Viacom CEO Philippe Dauman describe the status of his company's $1 billion lawsuit against Google and YouTube. As he talked of mounds of data and reams of documentation being collected and reviewed, I found myself slumping in my chair, thinking about how well all the lawyers involved in the case must be doing, and yet how pointless it all seems.

The old adage "2 wrongs don't make a right" fits this situation perfectly. There is no question that in the past YouTube was lax about enforcing copyright protection on its site and cavalier about how it responded publicly to the concerns of rights-holders. But it has made much progress with its Content ID system and a good faith effort to become a trusted partner. All of this is evidenced by the fact that Disney wouldn't even be talking to YouTube, much less cutting a deal, if it didn't view YouTube as reformed. While the media world is moving on, adapting itself to the new rules of video creation, promotion and distribution, Viacom continues to waste resources and executive attention pursuing this case. To be sure, Viacom has been plenty active on the digital front, but it is long overdue that these companies figure out how to resolve their differences and instead focus on how to work together to generate profits for themselves, not their lawyers.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Broadcasters, Cable Networks, Partnerships, UGC

Topics: Disney, ESPN, Google, Viacom, YouTube

-

Clarifying Comcast's and Time Warner's Plans to Deliver Cable Programming Via Broadband to Their Subscribers

Summary:

What: Major cable operators Comcast and Time Warner intend to offer broadband access to cable programs for the first time, but they have provided few specifics to date, thereby creating a swirl of confusing interpretations. This post seeks to clarify their plans.

Important for whom: Cable networks, other content providers, cable operators, consumers

Potential benefits: Flexible access and first-time online availability of popular cable programs.

Background

Since the WSJ reported two weeks ago today that Comcast and Time Warner Cable plan to offer online access to cable TV programming to their subscribers, there has been a significant amount of confusion and misinterpretation about what these companies are actually planning to do. Absent official statements from either company, there has been an ongoing debate about whether cable operators, who want to defend their traditional model, were moving to choke off the largely open access to broadband video that users have grown accustomed to.

Things got more confusing this past Monday when AdAge ran an interview ("TV Everywhere -- As Long As You Pay For It") with Jeff Bewkes, CEO of Time Warner Inc. in which he elaborated on a company initiative dubbed "TV Everywhere" that major cable network owners such as Time Warner Inc. Viacom, NBCU, Discovery and others are said to be collaborating on. Bewkes outlined a broad online vision including the idea that cable programming could also be available on sites like Hulu, MySpace, Yahoo and YouTube as well, provided that users were paying a fee to some underlying service provider (cable/satellite/telco).

A wrinkle in the interview was exactly whom Bewkes was speaking for, since Time Warner Inc. (or "TWI" which owns the cable networks CNN, TNT, TBS, etc.) plans to spin off as an independent entity Time Warner Cable ("TWC"), which operates cable systems serving 14 million subscribers. After the split, set for next week, which of these companies would actually be sponsoring the "TV Everywhere" vision?

The NYTimes' technology reporter Saul Hansell then picked up on the interview and wrote a piece on the paper's widely-read "Bits" blog entitled "Time Warner Goes Over the Top," which provocatively began, "Just as soon as Time Warner has divested itself from the cable business, Jeff Bewkes, its chief executive, is preparing to stab the cable industry in the back. That's what I read in an interview with Mr. Bewkes in Advertising Age..."

Saul went on to describe his interpretation of one particular Bewkes comment as implying that Time Warner Inc. would offer its networks directly to consumers (or "over the top" of cable operators), thereby setting off a domino effect in which others' networks did the same, all of which would ultimately lead to the destruction of the cable industry business model.

The attention all of this received, particularly in the blogosphere, prompted a fair number of people to contact me and ask what's really going on here.

Time Warner's Plans

Yesterday I spoke with Keith Cocozza, TWI's spokesman, who said that Bewkes's comments do represent both TWI and TWC. Their mutual vision is to have cable programming offered not just at TWC's

RoadRunner portal, but also at various third-party aggregators (Hulu, etc.) so long as they subscribe to any multichannel video service (whether from TWC, Verizon, DirectTV, etc.). They do envision offering a streaming-only service for those that don't want the traditional cable subscription, but it would only be available in their geographical footprint. All of that means that there's in fact no over-the-top threat involved here at all. TWI and TWC are "agnostic" about third-party aggregator access to the cable programs, because they recognize that people want to go to whatever sites make them most comfortable. And they do not plan to charge subscribers extra for online access.

RoadRunner portal, but also at various third-party aggregators (Hulu, etc.) so long as they subscribe to any multichannel video service (whether from TWC, Verizon, DirectTV, etc.). They do envision offering a streaming-only service for those that don't want the traditional cable subscription, but it would only be available in their geographical footprint. All of that means that there's in fact no over-the-top threat involved here at all. TWI and TWC are "agnostic" about third-party aggregator access to the cable programs, because they recognize that people want to go to whatever sites make them most comfortable. And they do not plan to charge subscribers extra for online access. From a consumer standpoint, all of this is quite enlightened. But from an operational standpoint, it feels incredibly complex. For example, I asked Keith about how a remote user, seeking to watch programs at a third party aggregator's site like Hulu, would be authenticated as an actual customer of a video service provider? While acknowledging it's too early to have all the answers, he said a test TWC has conducted in Wisconsin with HBO has shown this not to be a big technical problem. I don't agree. It's hard enough for companies to do a bilateral account integration (e.g. tying a user's Amazon account to a user's TiVo account); the idea of doing multilateral account integration (the numerous combinations of potential aggregators and service providers) is fraught with complexity and seems highly daunting.

Then there are financial issues to address. With no incremental subscriber payments, online program delivery needs to be sustained through ads alone. This would be quite workable if it were just cable operators and networks involved (they could split the ad avails proportionately as they've traditionally done with linear delivery), but by allowing third-party aggregators in too, a third mouth now needs to be fed. That will trigger a whole new negotiating dynamic, as each aggregator lobbies for a different share. And it's questionable whether there's even enough ad revenue for three parties to begin with, though Keith believes there is.

Comcast's Plans

Conversely, Kate Noel, Comcast's spokeswoman, told me yesterday that while it's still early to say anything definitive about Comcast's plans for distribution through third-party aggregators, their first priority is distribution of

cable programs on their own sites (e.g. Fancast, Comcast.net) and the networks' own sites. Comcast seems to have more of a "walk, before you run" approach. It recognizes that protecting subscribers' privacy in any account integration is crucial so it plans to proceed carefully. I tried to pin Kate down on whether Comcast intends to charge for online access. Again she felt it was too early to be definitive, but it sounds like they're leaning toward a no-charge model as well. The timeline is to begin rolling out access in the 2nd half of '09.

cable programs on their own sites (e.g. Fancast, Comcast.net) and the networks' own sites. Comcast seems to have more of a "walk, before you run" approach. It recognizes that protecting subscribers' privacy in any account integration is crucial so it plans to proceed carefully. I tried to pin Kate down on whether Comcast intends to charge for online access. Again she felt it was too early to be definitive, but it sounds like they're leaning toward a no-charge model as well. The timeline is to begin rolling out access in the 2nd half of '09.Clearly there are a lot of moving pieces involved with these companies' plans. In general Time Warner has a more aggressive, yet I believe far less pragmatic, plan. They're trying to get all the way to the end zone right away, when just advancing the ball further downfield would be real progress for today's broadband users seeking improved access to premium content. Time Warner's "TV Everywhere" seems like a great vision, but it would take years to fully implement. Comcast's plan is probably achievable in a year or less. Either way, major cable operators finally seem to have the ball rolling toward broadband distribution of cable programming. As I pointed out last week, this can only be viewed as a positive.

What do you think? Post a comment now.

(btw, if you want to learn more about all this, come to the Broadband Video Leadership Evening on March 17th in NYC, where we'll dig deeply into these issues with our top-notch panel)

Categories: Cable Networks, Cable TV Operators

Topics: Comcast, Hulu, MySpace, Time Warner Cable, Yahoo, YouTube

-

Inside Demand Media's "Content Factory"

Here's a question: without checking, who do you think is the largest supplier of videos to YouTube, by a factor of almost 10? If you said Demand Media, which has over 150K individual videos on YouTube that have generated a total of 442 million views to date, you'd be right. Most of the videos are supplied by Demand Media's knowledge-based Expert Village site, and are produced by Demand Studios, the company's content production arm. (For the record, CBS is a distant second supplier to YouTube with almost 16K videos and approximately 327 million total views.)

I learned this and a lot more in a recent and incredibly interesting discussion I had with Steven Kydd, EVP of Demand Studios. In case you've never heard of Demand Media, it's the latest act of former Intermix CEO and

MySpace chairman Richard Rosenblatt (who conceived it as a "thinking person's MySpace" as Steven put it). Since its inception in 2006, the company has raised $355 million, made a string of acquisitions and dramatically built up traffic at its portfolio of web sites.

MySpace chairman Richard Rosenblatt (who conceived it as a "thinking person's MySpace" as Steven put it). Since its inception in 2006, the company has raised $355 million, made a string of acquisitions and dramatically built up traffic at its portfolio of web sites. Most interesting for me though, is how Demand Studios has become a veritable "content factory" (my term), churning out 150K individual videos and 350K articles in 2 1/2 years. How it's done that, and better still, how it is monetizing this mountain of content, is the best example I've seen yet of how to effectively build scale at the intersection of social media, search and broadband video.

At the core of Demand Studios is a network of 10,000 freelance content creators that have passed through a rigorous screening process. Specific content is green-lighted through Demand's analysis of internal data. The potential value of a given piece of content is measured by internal algorithms estimating audience interest, advertiser interest and ability to generate traffic.

Once Demand has decided to produce a piece of content its editors tap into specific producers based on a match of their expertise. The producer follows Demand's guidelines, such as shooting exclusively in HD. But in general, the producer has a relatively free creative hand. If for example, the video involves children's nutrition, the producer can call upon a local health expert to appear (which as Steven notes, experts are often happy to do because the videos help raise their own profiles). Once the video is complete, it is edited for quality and has SEO-optimized metadata created and added.

This process is now refined to the point that 1,000 pieces of content are being created per day (30% video, 70% text), with plans to scale even further. Steven said Demand has paid out over $12M to its producers to date. Each producer's content is tracked over time to see how well it performs and is also peer-rated, allowing the cream of the producer network to rise to the top.

Once complete the content is posted on Demand's sites (e.g. Expert Village, eHow, LiveStrong.com, GolfLink, Trails.com, etc.) and in the case of video, on YouTube as well. As Steven notes, since YouTube has now surpassed Yahoo to be the 2nd largest search site, Demand's knowledge-based videos are a perfect fit for how many people increasingly use YouTube.

The two companies have developed a mutually beneficial relationship. YouTube now drives the majority of Demand's video traffic, and Steven says it is being monetized well through AdSense, overlays and companion ads. Conversely, with Demand now generating 2 million YouTube views per day, it has become an important supplier of quality video to YouTube, helping it bolster its value beyond its UGC roots and build its revenues. As well, YouTube has become a testing ground for new Demand sites, such as a Spanish language version of Expert Village.

Syndication beyond YouTube is a key part of Demand's ongoing success. Through its acquisition of Pluck, a white-label social media platform used by many media brands like USAToday.com, NPR, McGraw-Hill and others, Demand now has an opportunity to also syndicate its content to these publishers, who are increasingly resource-constrained and in need of high-quality third-party suppliers. In short, while Demand's "content factory" has already become a major supplier to YouTube, the world's largest video portal, it is now poised to do the same for lots of other sites as well, further growing its traffic.

There's no question that Demand's strict focus on knowledge-based, Long Tail videos has enabled it to create a unique formula that works well at the intersection of social media, search and broadband video. It's doubtful that all of this could be fully replicated in more creative genres like entertainment. Yet there are elements of Demand's content factory, such as leveraging YouTube's audience base, consistently creating high-quality metadata for SEO and applying rigorous criteria to what content gets produced, that are applicable to all video providers. Given Demand's ambitious plans, I suspect their factory will continue to evolve, providing still further lessons for how to create and monetize content in the broadband era.

What do you think? Post a comment now.

(Note: Steven Kydd will be on a panel I'm moderating at the NABShow on Wed, April 22nd, "How Syndication is Powering the Broadband Video Era." VideoNuze readers can register for complimentary access by using code X104)

Categories: Indie Video

Topics: Demand Media, eHow, GolfLink, LiveStrong.com, MySpace, Trails.com, YouTube

-

The Cable Industry Closes Ranks - Part 2

An article in Friday's WSJ "Cable Firms Look to Offer TV Programs Online" outlined a plan under which Comcast and Time Warner Cable, the nation's 2 largest cable operators, would give just their subscribers online access to cable networks' programming.

A Comcast spokesperson contacted me later Friday morning to explain that the plan, dubbed "OnDemand Online" is indeed in the works, though a release timeline is not yet set. The move is part of the company's

"Project Infinity" a wide-ranging on-demand programming vision that was unveiled at CES '08, but oddly has not been messaged much since. Meanwhile, thePlatform, Comcast's broadband video management/publishing subsidiary also called me on Friday to confirm that - unsurprisingly - it would be powering the OnDemand Online initiative (thePlatform's CEO Ian Blaine explains more in this post).The idea of cable operators setting up online walled gardens for their subscribers alone was first signaled by Peter Stern, Time Warner's EVP/Chief Strategy Officer on the panel I moderated at VideoNuze's Broadband Leadership Breakfast last November. As I wrote subsequently in "The Cable Industry Closes Ranks" my takeaway from his and other cable executives' recent comments was that the industry was poised to collaborate in order to defend cable's traditional - and highly profitable - business model. Under that model, cable operators currently pay somewhere between $20-25 billion per year in monthly "affiliate fees" to programmers whose networks are then packaged by operators into various consumer subscription tiers.

It should come as a surprise to nobody that both cable networks and operators are mightily incented to defend their model against the incursions of free "over the top" distribution alternatives. Indeed what's surprising to me is why it has taken the industry so long to act forcefully when the stakes are so high and the market's moving so fast? I mean cable operators themselves are the largest broadband Internet access providers in the country, and they have watched for years as their networks have been engorged by surging online viewing, courtesy of YouTube, Hulu, Netflix and others. While they've made some tepid moves to push programming online (though to be fair Comcast's Fancast portal has evolved quite a bit recently), overall their broadband video distribution activities have been underwhelming, evidence of broadband distribution's lower priority status vis-a-vis TV-based video-on-demand.

Meanwhile Friday's article triggered plenty of hackles from the blogosphere that those evil cable operators were up to their old monopolistic tricks, this time moving to control the broadband delivery market and choke off open access to premium video. While it's indeed tempting to see these plans that way, I think that would be the wrong conclusion.

Rather, I look at the Comcast/TWC moves as both welcome and likely to spur more, not less, consumer

access to broadband-delivered programming. That's because, if the cable networks are smart in their negotiations, they will gain from operators the approval to push more of their programs onto both their own web sites, and even to distribute some through others' sites. With net neutrality agitators hopeful in the wake of Barack Obama's election, Comcast and TWC need to tread carefully in these negotiations. Yet another part of the model I foresee is archived programs, which have been locked up in vaults due to programmers' concerns over operator reprisals if they leaked out online, becoming much more openly accessible. The Comcast/TWC hecklers need to remember one simple fact: to make quality programming requires solid business models. And in this economic climate, solid business models are far and few between. Despite having lost a total of over 500,000 video subscribers during the last 6 consecutive quarters, Comcast still owns one of those few sold models. And don't forget it is now investing to increase its broadband speeds, pledging 30 million, or 65% of its homes, will have 50 Mbps access by the end of '09 (a rollout which incidentally is all privately financed, without a dime of federal bailout money or other assistance).

In the utopian fantasy of some, all premium content flows freely, supported by a skimpy diet of ads alone. For some that works. Yet for cable networks accustomed to monthly affiliate fees this is completely unrealistic and uneconomic. One needs look no further than the wreakage of the American newspaper industry (including bankruptcy filings recently by the Chicago Tribune and today by the Philadelphia Inquirer) to understand the damage that occurs when business model disruption occurs in the absence of coherent, evolutionary planning.

Someday, when broadband video business models mature (as indeed they ultimately will), there will be lots of cable and other programming available for free online. For now though, getting Comcast and TWC to finally pursue an aggressive broadband distribution path is a welcome evolutionary step in unlocking this exciting new medium's ultimate potential.

What do you think? Post a comment now.

(Note: we'll be diving deep into this topic, and others, at VideoNuze's Broadband Video Leadership Evening on March 17th in NYC. More information and registration is here.)

Categories: Aggregators, Broadband ISPs, Cable Networks, Cable TV Operators

Topics: Comcast, Hulu, Netflix, Time Warner Cable, YouTube

-

Crunching comScore's Video Data Yields Market Insights

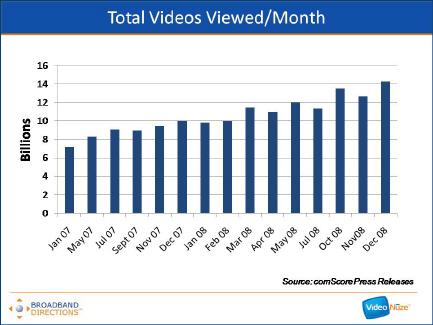

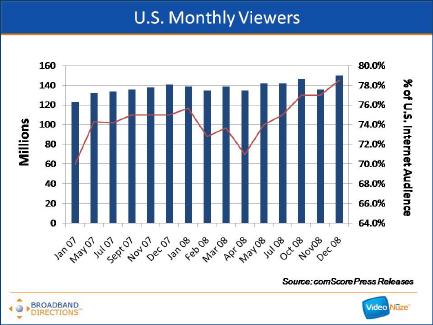

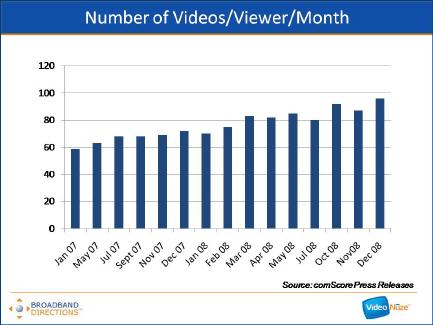

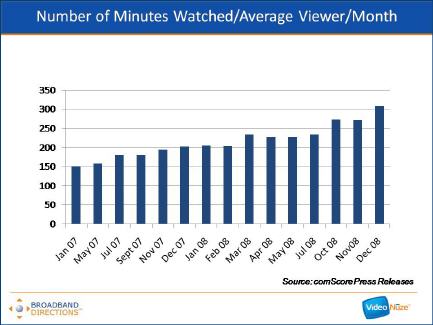

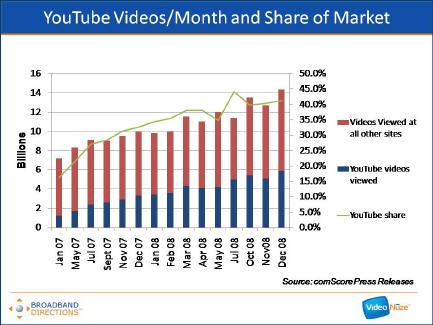

Last week when comScore announced data from its Video Metrix service for December '08, I made a note to myself to go back and look at all the video usage data comScore has released and see what it reveals. Below are 5 charts that I've compiled from comScore's press releases covering January 2007 - December 2008 (note comScore didn't report on every single month during this 24 month period so there are some holes in the graphs).

The first graph shows the growth in total videos viewed per month, roughly doubling from 7.2 billion views in Jan. '07 to 14.3 billion views in Dec. '08.

That growth is driven by a number of factors including an increase in the number of monthly viewers from 123 million in Jan. '07 (70% of U.S. Internet users) to 150 million in Dec. '08 (78.5% of U.S. Internet users).

It also reflects an increase in the number of videos viewed per viewer from 59 in Jan. '07 to 96 in Dec. '08.

Which further translates into the growth of total number of minutes the average viewer watched per month from 151 minutes per month in Jan. '07 to 309 minutes per month in Dec. '08.

Aside from the sheer growth of the market over the last two years, the most striking thing about the comScore data is the growth in usage and market share by YouTube. Back in Jan. '07, YouTube generated approximately 1.2 billion video views per month for a 16.2% share of all videos viewed. Two years later in Dec. '08 YouTube generated approximately 5.9 billion video views per month for a 41.2% market share. YouTube's share growth is staggering: in every month but 1 during this period YouTube increased its sequential monthly views and in all but 3 months it increased its sequential monthly market share.

Aside from the sheer growth of the market over the last two years, the most striking thing about the comScore data is the growth in usage and market share by YouTube. Back in Jan. '07, YouTube generated approximately 1.2 billion video views per month for a 16.2% share of all videos viewed. Two years later in Dec. '08 YouTube generated approximately 5.9 billion video views per month for a 41.2% market share. YouTube's share growth is staggering: in every month but 1 during this period YouTube increased its sequential monthly views and in all but 3 months it increased its sequential monthly market share.

Recall that Google closed on the YouTube acquisition in Nov. '06 and at $1.65 billion, many thought Google had grossly overpaid. Some may still believe this as YouTube is still very much a work in progress in terms of how it generates revenue. But there's no questioning the phenomenal two-year run it has had in terms of its usage and market share growth. This is one of the reasons why I continue to believe YouTube is one of the most powerful platforms for eventually disrupting the traditional video distribution value chain.

If these slides are hard to view, I've uploaded them all to SlideShare.

What do you think? Post a comment now.

Categories: Aggregators

Topics: comScore, Google, YouTube

-

For YouTube, A William Morris Deal Would Create Issues

The NY Times reported this week that YouTube is in talks with the William Morris talent agency about a possible deal to have some of its clients create videos especially for YouTube.

Nothing's confirmed at this point and who knows if an actual deal will result. However, if one does it would

be a major strategy change for YouTube and I believe would create lots of new issues for the company to deal with. YouTube has always insisted that it is not a content creator; rather its goal has been to be a platform partner for premium video providers seeking to get the most out of the broadband medium. The company has made significant progress on this front while recognizing that its vast collection of user-generated video will always be valued by its users but will be largely unmonetizable. Still, YouTube has been viewed cautiously by large media companies wary of its reach and disruptive potential. There's still lingering concern about why it took so long to get its Content ID system in place to protect its partners' copyrights (lest we forget the residual of that delay is the Viacom lawsuit that still looms).

From my perspective YouTube risks its credibility with its premium partners if the Morris deal happens. It is going to reopen the debate about what YouTube wants to be when it grows up: distribution partner or content creator. Other questions abound: Will the YouTube-Morris content compete directly with certain premium partners? Will the Morris content receive preferential promotional treatment? And how about the risk that data YouTube keeps about its premium partners' channels could be shared with Morris to help guide its content strategy? The questions go on. YouTube may feel it can finesse these questions and/or that its 40% video market share gives it leeway to push the envelope.

I've long thought that YouTube would find it irresistible to eventually get into the content business itself. The logic flows from precedent. For example, in the cable TV world, TCI was once the largest cable operator. It recognized the enormous financial leverage it enjoyed if it evolved beyond simply being packager of others' channels. As partner in channels in which it owned equity, it guaranteed them distribution, which in turn created viewership, ad and affiliate revenues and big-time value. In fact, TCI's content activities were so successful that it ultimately spawned a whole new company, Liberty Media, to manage its programming investments.

Similarly for YouTube, its access to millions of eyeballs creates a lot of temptation to have its own content properties, all the more so as broadband finds its way to the TV. No doubt YouTube has been pitched on this idea repeatedly over the years. But if it chooses to proceed this time it will no doubt hear concerns raised from its partners. Can it be a neutral, committed distribution partner while it also tries to build up its own content portfolio?

Further, there's the specter of Google and its potent monetization engine backing YouTube's content properties, which could also be viewed as competitive with its partners' ad sales efforts. Put all of this together and the potential Morris deal creates lots of new issues. If it comes to fruition it will be interesting to see how YouTube navigates them.

What do you think? Post a comment now.(Update 2/3/09 - Since I posted this piece, sources close to the YouTube-Morris deal have reached out to me and explained that the deal will be similar to the Seth MacFarlane-Media Rights Capital deal previously unveiled on Google Content Network. They have also clarified the point I discussed above, saying that YouTube and Google will remain a platform for distributing content, but will not be involved in producing or taking an equity stake in it.The deal suggests that the Hollywood community continues to think innovatively about how top tier talent can get involved with broadband video. In this case, Morris has a roster of big-name clients and relationships that could be married to the Google Content Network for widespread distribution. No doubt further deals will follow as the model gets further baked. More on this deal and its implications coming soon.)

Categories: Aggregators, Partnerships, UGC

Topics: William Morris Agency, YouTube

-

Adconion.TV: Trying to Do Google Content Network One Better

I've been very intrigued by two recent announcements from Adconion, which bills itself as the largest independent online advertising network.

First, in early October, it announced "AMG-TV," a video content syndication network now called "Adconion.TV" as well as its first deal, to distribute Vuguru's "Back on Topps." Then last week it acquired KTV Digital Media, a production studio and syndicator, to become a wholly-owned subsidiary called RedLever. Late last week I got a briefing from Adconion CEO/founder Tyler Moebius and Reeve Collins, CEO RedLever to learn more.

My take is that Adconion.TV/RedLever is emulating the same model as Google Content Network, except with a couple of interesting twists (for more on GCN, see "Google Content Network Has Lots of Potential, Implications"). Nevertheless, both are classic Syndicated Video Economy plays, which could have a huge impact on the fundamentals of broadband video's future business model.

For those not familiar with Adconion, it says it reaches 260M unique visitors/month, second only to Google.

Traffic is about evenly split between the U.S. and the rest of the world. It has 800+ publishers in its network, including 60-70 that it represents exclusively, primarily for international sales. The company made a big splash earlier this year when it raised a monster $80M round led by Index Ventures (the lead investor in Skype among others). It has grown from 30 employees in '06 to 285 in '08.

Traffic is about evenly split between the U.S. and the rest of the world. It has 800+ publishers in its network, including 60-70 that it represents exclusively, primarily for international sales. The company made a big splash earlier this year when it raised a monster $80M round led by Index Ventures (the lead investor in Skype among others). It has grown from 30 employees in '06 to 285 in '08. The similarities between Adconion.TV and GCN are as follows: both believe their vast network of publisher web sites - which were initially built to serve ads - can now be modified to also accept high-quality syndicated video content. Each leverages the same algorithms it used to optimize which ads to insert, so that video too will only be served to the most appropriate sites. One might think of both these companies as being in the real estate business. Each has colonized vast tracts of web property and is now trying to identify, as real estate pros would say, the "highest and best use" of its inventory: ads, video or some combination of the two.

At the core of both Adconion.TV and GCN is the conviction that content should be brought to users wherever they may live, as opposed to attempting to drive them to a destination site, a la the "must-see TV" model of old. This has been a key tenet of the Syndicated Video Economy concept I've been fleshing out in '08. With the fragmentation of users over the web, social networks, mobile devices, gaming consoles, etc. the way to build a franchise is to propagate video into all of the web's nooks and crannies. Note others like Grab Networks, Syndicaster, 1Cast, Jambo and others are also heavily pursuing the syndication opportunity, each with their own competitive angle.

In both initiatives content-distribution-brand advertising are the three legs of the business model stool. Consider: in Adconion.TV's launch deal it was a package of Vuguru/Back On Topps (content) - Adconion.TV (distribution) and Skype (brand), while GCN's was Seth MacFarlane/Cavalcade of Comedy (content) - GCN (distribution) - Burger King (brand). I asked Tyler whether this three-legged stool is the model for independent broadband content (whose nascent studios have been slammed by the down economy) to be funded in the future, he emphatically replied "yes."

This highlights one key difference between GCN and Adconion.TV. Google of course has been very clear in steering away from content creation, consistently declaring it's "not a content company." Adconion, on the other hand, specifically intends to custom produce brand-infused broadband video programming. That's where the KTV acquisition comes in. Tyler explained that it is deep into talks with numerous agencies and brands about creating programs that showcase the brand sponsors. Two deals are expected to be announced soon.

Another difference is that GCN tried to drive traffic back to YouTube to incent users to subscribe to ongoing program updates and get exposed to other related programs. In my GCN post, I wrote enthusiastically that the marriage of AdSense-powered video distribution as the "spokes" with YouTube as the "hub" was formidable because it gives GCN a mechanism to build ongoing viewership beyond the first exposure at the publisher site.

Today Adconion lacks a comparable destination site. Tyler doesn't think that's important since it offers ways to subscribe, get email alerts and share within the player itself. Plus he's not hearing demand for it from brands. Still I think as this story unfolds and Adconion.TV finds itself competing with GCN for the highest-potential content, a destination site compliment will become essential. Should it agree, an acquisition would make sense to fill this hole (Metacafe? DailyMotion?).

For now though, Adconion has an aggressive plan to build Adconion.TV as an exciting new entry on the Syndicated Video Economy landscape. With its resources, reach and new production capabilities, this is clearly one to keep an eye on.

What do you think? Post a comment now.

Categories: Advertising, Aggregators, Syndicated Video Economy

Topics: 1Cast, Adconion, Google, Google Content Network, Grab Networks, KTV Digital Media, Syndicaster, YouTube

-

Here Comes Sling.com

Does the world need another broadband video aggregation site for premium quality video content?

The answer to that question will start to come early next week when Sling.com, the latest entrant in this already crowded space, officially launches. Recently Jason Hirschhorn, president of Sling Media's entertainment group and Brian Jaquet, Sling's Director of Public Relations came through Boston and caught me up on their plans to launch commercially on Nov. 24th.

Many of you know that Sling is the maker of the Slingbox, which connects to your TV or DVR, allowing you

to remotely watch programs on your computer. It's a very clever product, though I have to admit its use case has always been a little confounding to me. Nonetheless, just over a year ago, Sling was acquired by EchoStar in a $380 million deal. Shortly thereafter, EchoStar split itself into two parts, Dish Network, the satellite-delivered programming company, and EchoStar Corporation, which includes Sling and other technology-based businesses.

to remotely watch programs on your computer. It's a very clever product, though I have to admit its use case has always been a little confounding to me. Nonetheless, just over a year ago, Sling was acquired by EchoStar in a $380 million deal. Shortly thereafter, EchoStar split itself into two parts, Dish Network, the satellite-delivered programming company, and EchoStar Corporation, which includes Sling and other technology-based businesses.Sling.com, developed by Jason's entertainment group, is the first Sling offering not tethered to any of its devices and therefore open to all users. Acknowledging that Hulu has set a high bar on user experience, Jason explained that Sling.com is attempting to go one step further on usability, and will also differentiate itself with updated social networking capabilities and highly focused editorial content.

In particular, Sling.com offers a slew of Facebook-like features that allow users to subscribe to and favorite programs and networks, with users in turn able to follow these activities. As Jason aptly put it, the goal is to "digitize the water cooler conversation." The whole experience is geared toward engaging the user at a far deeper level than we're accustomed to in passive linear viewing, or even typical at other aggregators' sites.

The real differentiator for Sling long-term though is the integration of Sling.com with the remote viewing offered by Slingbox. Enabled by a new web-based player (instead of the prior downloadable client), users are able to seamlessly browse back and forth between watching live TV and cataloged programs, as shown below.

Taking this one step further, Sling's goal is to get its remote viewing technology embedded in others' set-top boxes as well. So for example, a Comcast STB with Sling inside would allow you to have live TV integrated into your Sling.com, without having to go buy another box.

That's an enticing prospect, but making it happen will be no small feat; the STB giants like Motorola and SA (now part of Cisco) will get on board only when their biggest customers - America's cable operators - ask for it. The prospect of these cable executives wanting to incorporate any technology controlled by Charlie Ergen, Echo's founder/CEO and the cable industry's arch-enemy, stretches my mind. However, stranger deals have been done, so who knows. In the meantime, there are a whole lot of other non-cable homes globally Sling can address first.

But much of that is down the road anyway. For now, Sling.com is going to compete head on with Hulu (which by my count supplies virtually the entire current movie catalog at Sling.com, in turn begging the question of how many different ways one relatively small ad revenue stream can get carved up?), Fancast, the portal sites, YouTube and so on. Jason readily admits that these sites will not compete on content exclusivity; ultimately they'll all have access to everything that's available.

So in this incredibly crowded space, is there room for a newcomer? On the surface, it's tempting to say "no." But history teaches us that "better mousetraps" can elbow their way into even the most crowded spaces. Remember how many search engines already existed when Google burst onto the scene? On a totally different level, I can relate to this challenge myself. A year ago I wondered whether there was room for a new broadband video-centric blog when so many others already existed; now here we are.

The reality is that newcomers succeed because they don't accept the status quo as final. Rather, they find smart ways of delivering new and better value to customers who didn't necessarily even know what they wanted, but when they got it, were delighted. That's Sling.com's challenge. Whether it can meet it remains to be seen. But in this crummy economy, their deep-pocketed backing certainly gives them a leg up on any VC-funded competitors when it comes to long-term staying power.

What do you think? Post a comment now!

Categories: Aggregators, Cable TV Operators, Devices, Satellite

Topics: Cisco, DISH Network, EchoStar, Fancast, Hulu, Motorola, SA, Sling, YouTube

-

Watching Reed Hastings at NewTeeVee Live

Yesterday I had my own positive broadband video experience, remotely watching portions of the

NewTeeVee Live conference held in SF from the comfort of my office. Om Malik and crew put together a packed agenda and I had wanted to go, but a personal conflict kept me in Boston.

NewTeeVee Live conference held in SF from the comfort of my office. Om Malik and crew put together a packed agenda and I had wanted to go, but a personal conflict kept me in Boston. I caught most of Netflix CEO Reed Hastings' keynote (until the UStream feed froze up, arghh...) and thought he offered some interesting tidbits about how he sees the broadband video market unfolding. VideoNuze readers know I've been avidly following Netflix's recent moves with Watch Instantly and I've come to think of the company as one of three key aggregators best-positioned to disrupt the cable model (the other two being YouTube and Apple).

Three noteworthy points that Hastings made:

Standards needed to interface broadband to the TV - Hastings catalogued the efforts Netflix is making to integrate with various devices like Roku, LG, TiVo, Xbox, etc, but concluded by saying that these one-off, ad hoc integrations are not scalable and are really slowing the market's evolution. Most of us would agree with this assessment. Still, he was quite pessimistic about a standards setting process's ability to move quickly enough - saying this could be a 10-30 year endeavor. Instead, if I understood him correctly, he thinks the TV approach should just be browser- based, and also that today's remotes should be scrapped in favor of pointer-driven (i.e. mouse-like) navigation.

Cable should evolve to focus on broadband delivery and de-emphasize multichannel packaging - Of course this is incredibly self-serving from Netflix's standpoint, but Hastings made the case that broadband margins for cable operators are nearly 100%, because they have no content costs, whereas on the cable side, they have high and ever-increasing programming costs. He cited Comcast's recent announcement of 50 Mbps service as evidence that cable operators should focus on winning the broadband war, and eventually letting go of the multichannel model. Nice try Reed, but I don't see that happening anytime soon. However, as I recently wrote in "Comcast: A Company Transformed," there's no question that broadband is becoming an ever greater part of its revenue and cash flow mix.(Reed emailed to clarify the above point. He didn't say cable should focus on broadband delivery over the current multichannel model; rather that cable - and satellite/telco - should focus more on web-like viewing experiences through improved navigation and VOD/DVR to be more on-demand, personalized and browser-friendly. And he added that with the shift to heavier broadband consumption, cable is a winner either way. Note - I thought I interpreted him correctly, but between UStream choking and my own scribble, it seems I was a bit off here. Thanks for correcting Reed.)Game consoles in leading position to bridge broadband to the TV - Hastings made a pretty strong case for the Wii - and to a lesser extent the PlayStation and Xbox - as the leading bridge devices. The Wii in particular could be a real broadband winner if it could support HD and Flash. As I've been thinking about broadband to the TV, I've concluded - barring anything from left field - that game devices, IP-enabled TVs and IP-enabled Blu-ray players are where the action will be concentrated for the next 3-4 years (this doesn't take account of forklift substitutes like a Sezmi or others sure to come).

NewTeeVee has a good wrap-up of Hastings' talk as well, here. The video replay isn't up yet, but when I see it, I'll post an update.

What do you think? Post a comment now!

Categories: Aggregators, Cable TV Operators, Devices

Topics: Apple, Comcast, LG, Netflix, PlayStation, Roku, TiVo, Wii, XBox, XBox, YouTube

-

Notes from Broadband Video Leadership Breakfast

Yesterday, I hosted and moderated the inaugural Broadband Video Leadership Breakfast, in association with the CTAM New England and New York chapters, here in Boston (a few pics are here). We taped the session and I'll post the link when the video is available. Here are a few of key takeaways.

My opening question to frame the discussion centered on broadband's eventual impact on the cable business model: does it ultimately upend the traditional affiliate fee-driven approach by enabling a raft of "over-the-top" competitors (e.g. Hulu, Netflix, Apple, YouTube, etc.) OR does it complement the model by creating new value and choice? As I said in my initial remarks, I believe that how this question is ultimately resolved will be the key determinant of success for many of the companies involved in today's broadband ecosystem and video industry.

I posed the question first to Peter Stern, who's in the middle of the action as Chief Strategy Officer of Time Warner Cable, the second largest cable company in the U.S. I thought his answer was intriguing: he said that it is cable networks themselves who will determine the sustainability of the model, depending on whether they choose to put their full-length programs online for free or not.

Later in the session, he put a finer point on his argument, saying that "a move to online distribution by cable networks would directly undermine the affiliate fees that are critical to creating great content" and that finding ways to offer these programs only to paying broadband Internet access subscribers was a far better model for today's cable networks and operators to pursue (for more see Todd Spangler's coverage at Multichannel News).

Peter's point echoes my recent "Cord-Cutters" post: to the extent that cable networks - which now attract over 50% of prime-time viewership, and derive a third or more of their total revenues from affiliate fees - withhold their most popular programs from online distribution, they provide a powerful firewall against cord-cutting. Speaking for myself for example, the prospect of missing AMC's "Mad Men" (not available online anywhere, at least not yet...) would be a powerful disincentive for me to yank out my Comcast boxes.

These thoughts were amplified by the other panelists, Deanna Brown, President of SN Digital, David Eun, VP of Content Partnerships for Google/YouTube, Roy Price, Director of Digital Video for Amazon and Fred Seibert, Creative Director and Co-founder of Next New Networks, who held fast to a highly consistent message that broadband should be thought of as expanding the pie, thereby creating a new medium for new kinds of video content. David, in particular cited the massive amount of user-uploaded and consumed video at YouTube (amazingly, about 13 hours of video uploaded every minute of every day) as strong evidence of the community and context that broadband fosters.

Still, our audience Q&A segment revealed some very basic cracks in the panelists' assertions that the transition to the broadband era can be orderly and managed (not to mention that afterwards, I was privately barraged by skeptical attendees). First and foremost these individuals argued the idea that the cable industry can maintain the value of its subscription service by using the control-oriented approach typified by the traditional windowing process flies in the face of valuable lessons learned by the music industry.

Of course most of us know that sorry story well by now: an assortment of entrenched, head-in-the-sand record labels forcing a margin rich, but speciously valued product (namely the full album or CD) on digitally empowered audiences, who decided to take matters into their own hands by stealing every song they could click their mouses on. Consequently, a white knight savior (Apple) offering a legitimate and consumer-friendly purchase alternative (iPod + iTunes), which would grew to be so popular that it has made the record labels beholden to it, while simultaneously hollowing out the last vestiges of the original album-oriented business model.

Does history repeat itself? Are Peter and the other brightest lights of the cable industry deluding themselves into thinking that a closed, high-margin, windowed platform like cable can ever possibly morph itself into a flexible, must-have service for today's YouTube/Facebook generation?

I've been a believer for a while that by virtue of their massive base of broadband-connected homes, high-ARPU customer relationships and programming ties, cable operators have enormous incumbent advantages to win in the broadband era. But incumbency alone does not guarantee success. Instead, what wins the day now is staying in tune with and adapting to drastically changed consumer expectations, and then executing well, day after day. One look at the now gasping-for-breadth behemoth that was once proud General Motors hammers this point home all too well.

As Fred succinctly wrapped things up, "The reason I love capitalism is that it forces all of us to keep doing things better and better." To be sure, broadband and digital delivery are unleashing the most powerful capitalistic forces the video industry has yet seen. What impact these forces ultimately have on today's market participants is a question that only time will answer.

What do you think? Post a comment now!

Categories: Aggregators, Broadband ISPs, Cable Networks, Cable TV Operators, Indie Video

Topics: Amazon, CTAM, Google, Next New Networks, Scripps, SN Digital, Time Warner Cable, YouTube

-

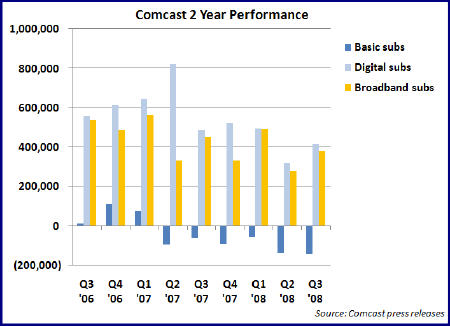

Comcast: A Company Transformed

Three numbers in last week's third quarter Comcast earnings release underscored something I've believed for a while: Comcast is a company transformed, now reliant on business drivers that barely existed just ten short years ago. Comcast's transformation from a traditional, plain vanilla cable TV operator to a digital TV and broadband Internet access powerhouse is profound proof of how consumer behaviors' are changing and value is going to be created in the future.

The three numbers that caught my attention were the net additions of 382,000 broadband Internet subscribers and 417,000 digital subscribers, with the simultaneous net loss of 147,000 basic subscribers. The latter number is the largest basic sub loss the company has sustained and, based on the company's own earnings releases, the sixth straight quarter of basic sub contraction. In the pre-digital, pre-broadband days, when a key measure of cable operators' health was ever-expanding basic subscribers, this trend would have caused a DEFCON 1 situation at the company. (see graph below for 2 year performance of these three services)

That it doesn't any longer owes to the company's ability to bolster video services revenue and cash flow through ever-higher penetration of digital services into its remaining sub base (at the end of Q3 it stood at 69% or 16.8 million subs). Years after Comcast and other cable operators introduced "digital tiers," stocked with ever-more specialized channels that consumers resisted adopting, the industry has hit upon a winning formula for driving digital boxes into Americans' homes: layering on advanced services like HD, VOD and DVR that are only accessible with digital set top boxes and then bundling them with voice and broadband Internet service into "triple play" packages. Comcast has in effect gone "up-market," targeting consumers willing and able to afford a $100-$200/month bundle in order to enjoy the modern digital lifestyle.

Still, in a sense the new advanced video services represent just the latest in a continuum of improved video services. Far more impressive to me is the broadband growth that both Comcast and other cable operators have experienced. Comcast's approximately 15 million YE '08 broadband subscribers will generate almost $8 billion in annual revenue for Comcast, up dramatically from its modest days as part of @Home 10 years ago. (It's also worth noting the company now also provides phone service to over 6 million homes today vs. zero 10 years ago)

The cable industry as a whole will end 2008 with approximately 37 million broadband subs, again up from single digit millions 10 years ago. And note that the 387,000 net new broadband subs Comcast added in Q3 '08 compares with just 277,000 net broadband subs that the two largest telcos, AT&T and Verizon added in quarter, combined. As someone who was involved in the initial trials of broadband service at Continental Cablevision less than 15 years ago, observing this growth is nothing short of astounding.

While broadband's financial contribution to Comcast is unmistakable, its real impact on the company is more

keenly felt in its newfound importance in its customers' lives. Broadband Internet access has become a true utility for many, as essential in many homes as heat, water and electricity. A senior cable equipment executive told me recently that research done by cable companies themselves has shown that in broadband households, broadband service would be considered the last service to get cut back in these tough economic times. In these homes cable TV itself - long thought to be recession-resistant - would get cut ahead of broadband.But Comcast and other cable operators must not rest on their laurels. Their next big challenge is to figure out how to take this massive base of broadband subs and start delivering profitable video services to it. If Comcast allows its broadband service to be turned into a dumb pipe, with "over the top," on demand video offerings from the likes of Hulu, YouTube, Neflix, Apple and others to ascend to dominance, that would be criminal. Not only would it devalue the broadband business, it would dampen interest in the company's advanced video services (VOD in particular) while making the company as a whole vulnerable in the coming era of alternative, high-quality wireless delivery.

Comcast is indeed a company transformed from what it was just 10 years ago. Technology, changing consumer behaviors and a little bit of "being in the right place at the right time" dumb luck have combined to allow Comcast to remake itself. Comcast itself must fully recognize these changes and aggressively build out Fancast and other initiatives to fully capitalize on its newfound opportunities.

What do you think? Post a comment now.

Categories: Aggregators, Broadband ISPs, Cable TV Operators, Telcos

Topics: Apple, AT&T, Comcast, Netflix, Verizon, Verizon, YouTube

-

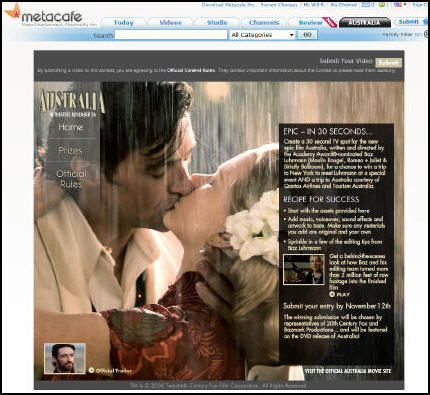

Fox, Metacafe Have a Winner with New "Australia" Contest

This morning Twentieth Century Fox and Metacafe are announcing "The Thirty Second Film Contest," which challenges contestants to put together a winning thirty second spot for the epic film "Australia," opening on November 26th. Though not yet fully live, I like the direction of this initiative a lot, and believe it provides an innovative example of how to blend traditional film marketing techniques with broadband-enabled audience participation.

Contestants visit the promotional site hosted at Metacafe, a large aggregator of short-form entertainment, to obtain film-related assets provided by Fox. These can be augmented with the contestant's own music, voiceovers, sound effects and artwork to create a highly original entry. Entries are submitted through Metacafe and will be judged by the folks at Fox and Bazmark (Australia director Baz Luhrman's company).

The contest is actually meant to be quite serious and semi-professional; Luhrmann has also created a whole library of videos about film-making, which a student of the art can use to help shape his/her entry, or just watch to learn. The grand prize is enticing: a trip for two to Australia, another to NY for a private screening/meeting with Luhrmann and inclusion of the winning entry on the film's eventual DVD.

The Australia contest builds on a similar one that Metacafe and Universal offered for "The Bourne Ultimatum" last year, which I reviewed enthusiastically here. The concept also follows on previous posts I've done about the value of what I call "purpose-driven user generated video" or "YouTube 2.0" opportunities for users to create videos that have actual business value. I continue to believe that user-submitted videos which go beyond goofball entertainment are a huge area of broadband industry opportunity.

The Australia contest is a winner on multiple levels as it; creates pre-release buzz for the film, allows fans and aspiring artists to get involved and showcase their work, taps into a large base of original (and free!) ideas to help promote the movie, and introduces a fresh, updated approach to film marketing that is sorely needed for differentiation.

This week I've been talking a lot about engagement and why it's so critical in the broadband era. While media and entertainment companies must always focus on driving ratings points or a big opening day box office, the ways to do so are changing. The key change I see is that films, TV programs and other entertainment must become part of a larger experience - complete with multifaceted engagement opportunities - rather than just a one-off moment of audience consumption. Broadband enables this shift in a big way. More marketers need to take advantage of the possibilities.

What do you think? Post a comment now!

Categories: Aggregators, Brand Marketing, FIlms, UGC

Topics: Bazmark, FOX, MetaCafe, Universal, YouTube

-

EveryZing's New MetaPlayer Aims to Shake Up Market

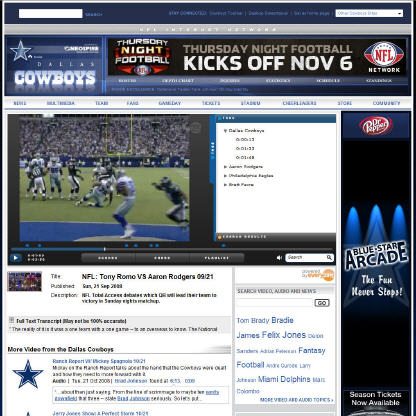

EveryZing, a company I wrote about last February, is announcing the launch of its MetaPlayer today and that DallasCowboys.com is the first customer to implement it. My initial take is that MetaPlayer should have strong appeal in the market, and could well shake things up for other broadband technology companies and for content providers. Last week I spoke to EveryZing's CEO Tom Wilde to learn more about the product.

MetaPlayer is interesting for at least three reasons: (1) it drives EveryZing's video search and SEO capabilities inside the videos themselves, (2) it provides deeper engagement opportunities than typically found in other video player environments and (3) it enables content providers to dramatically expand their video catalogs, while maintaining branding and editorial integrity.

To date EveryZing's customers have used its speech-to-text engine to create metadata for their sites' videos, which are then grouped into SEO-friendly "topical pages" that users are directed to when entering terms into the sites' search box. Speech-to-text and other automated metadata generating techniques from companies like Digitalsmiths are becoming increasingly popular as content providers continue to recognize the value of robust metadata.

MetaPlayer takes metadata usage a step further by creating virtual clips based on specified terms, which are exposed to the user. A user's search produces an index of these virtual clips, which can be navigated through time-stamped cue points, transcript review, and thumbnail scenes (see below for example). The virtual clip approach is comparable in some ways to what Gotuit has been doing and is pretty powerful stuff, as it lets the user jump to desired points, thus avoiding wasted viewing time (e.g. just showing the moments when "Tony Romo" is spoken)

Next, MetaPlayer enables deeper engagement with available video. Yesterday, in "Broadband Video Needs to Become More Engaging," I talked about how the importance of engagement to both consumers and content providers. MetaPlayer is a move in this direction as it allows intuitive clipping, sharing and commenting of a specific video clip within MetaPlayer. Example: you can easily send friends just the clips of Romo's touchdown passes along with your comments on each.

Last, and possibly most interesting from a syndication perspective, MetaPlayer allows content providers to dramatically expand their video offerings through the use of what's known as "chromeless" video players. I was first introduced to the chromeless approach by Metacafe's Eyal Hertzog last summer. It basically allows the content provider to maintain elements of the underlying video player, such as its ability to enforce a video's business policies (ad tags, syndication rules, etc.), while allowing new features to be overlayed (customized look-and-feel, consistent player controls, etc.).